Credit overshoots

- 9 February 2022

- Credit

Credit markets have been overshooting on the back of the European Central Bank meeting. The market now needs to come to terms with the new normal - a quicker end to the Asset Purchase Programme/Corporate Sector Purchase Programme. In theory, spreads now look cheap but further widening is likely, and thus we remain more conservative for now

Spread widening is overdone

Spreads widened 6-9bp towards the end of last week on the back of the European Central Bank (ECB) meeting, alongside mutual fund outflows and exchange-traded fund (ETF) outflows and selling, with particular underperformance in higher beta (14-16bp) and the longer end of the curve, pushing curves steeper again.

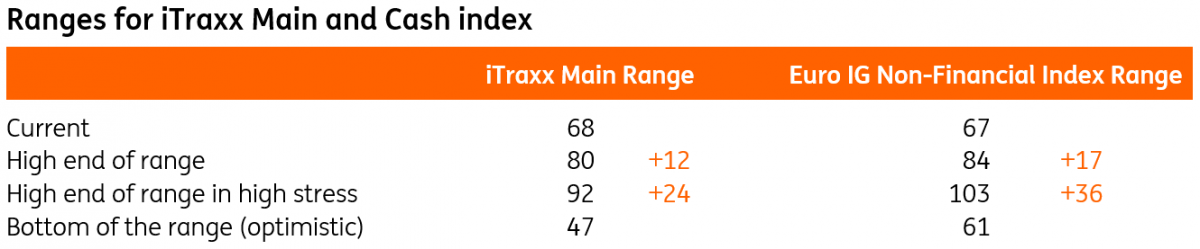

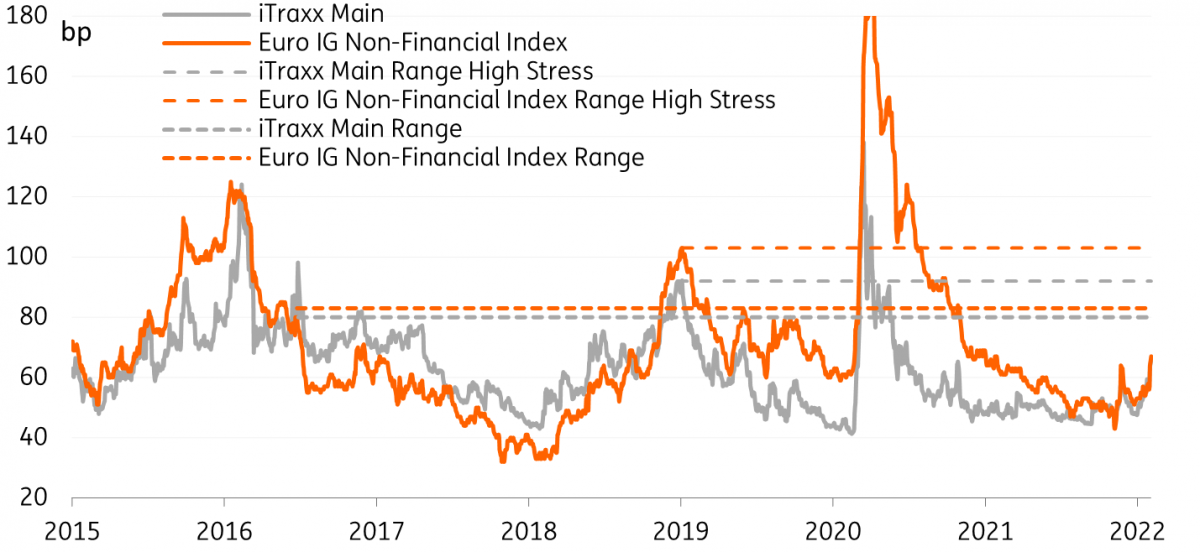

This spread widening on the back of the ECB messaging has sent the European credit market into flux. We feel spreads are now heading into oversold territory and could potentially approach the wide spreads seen in mid-2016 and mid-2019. When compared to both mid-2016 and mid-2019, we determine a new high end of the range to be 80bp for the iTraxx main and 83bp for the ICE BofA Euro non-financial index, although in a more stressed environment, spreads could reach levels last seen in early 2019.

Ranges for iTraxx Main and Cash index

Sooner end to APP

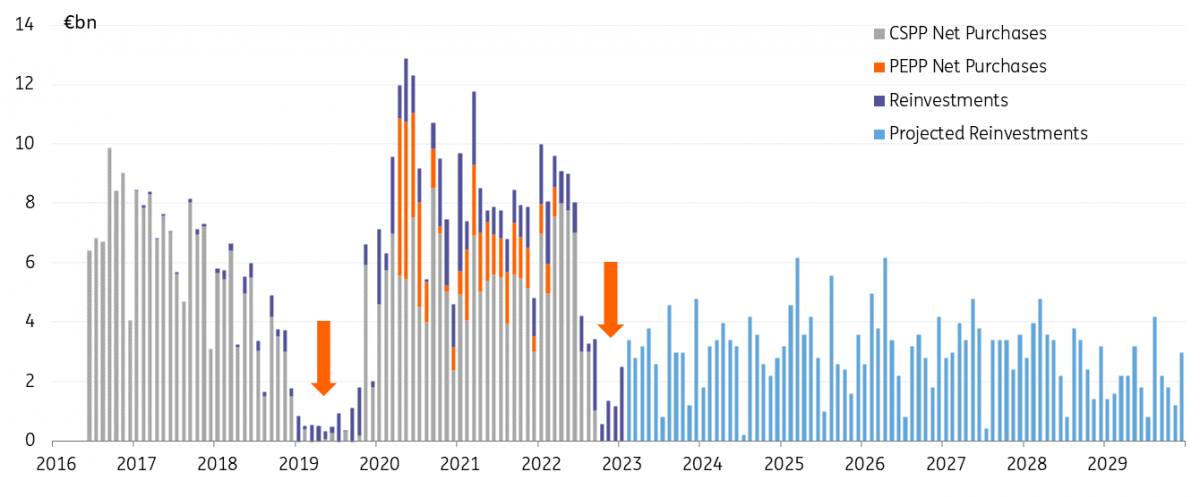

The hawkish tone from the ECB opens up the likelihood of an earlier rate hike. Therefore, our economists now expect the APP to come to an end in October. But this programme will still be at an increased level for the second and third quarters, as the ECB transitions away from the PEPP. This could still lead to a temporary increase in corporate purchases per month, compared to the combination of the Corporate Sector Purchase Programme (CSPP) and PEPP, while assuming the ratio of CSPP to overall APP will drop slightly from 27.5% to 25% during the second and third quarters.

Below we break down the monthly gross purchases under CSPP (and PEPP until March). Our previous forecast had the expectation of APP ending in 1Q23, while our new forecast shows APP ending in October with just reinvestments from then onward. Finally, we take a look at a risk scenario of an even quicker taper and end to APP than what’s now expected, whereby APP ends in June.

Indeed there is a significant drop in monthly gross purchases if CSPP stops in October, but reinvestments will continue for some years to come. And a further word of warning lies ahead as the timing of a tapering of CSPP is quite poor for credit markets, as reinvestments in 4Q22 are small at an average below €1bn. And under an even earlier taper, reinvestments in 3Q will also do little to support credit market technicals and spreads. The benefit of reinvestments is not really felt until next year when, as the light blue bars show in the graph below, reinvestments rise to between €2.5bn and €4.5bn a month.

ECB corporate purchases will remain high until October, and reinvestments are significant for years to come

Overshoot in spread widening will continue

All in all though, we feel most of the adjustment in credit spreads has been made for the taper that commences in October. However, it is expected that the spread widening will continue, opening up more value creation in credit, particularly when the primary market starts to produce its usual volumes after the earnings season. Our new forecast for gross purchases of €66.5bn for 2022 is indeed a decrease, but is not low. The forecast €51bn of net purchases will still, in combination with coupon payments, offset the €67bn of forecast net supply. This means negative net supply in the European corporate credit market.

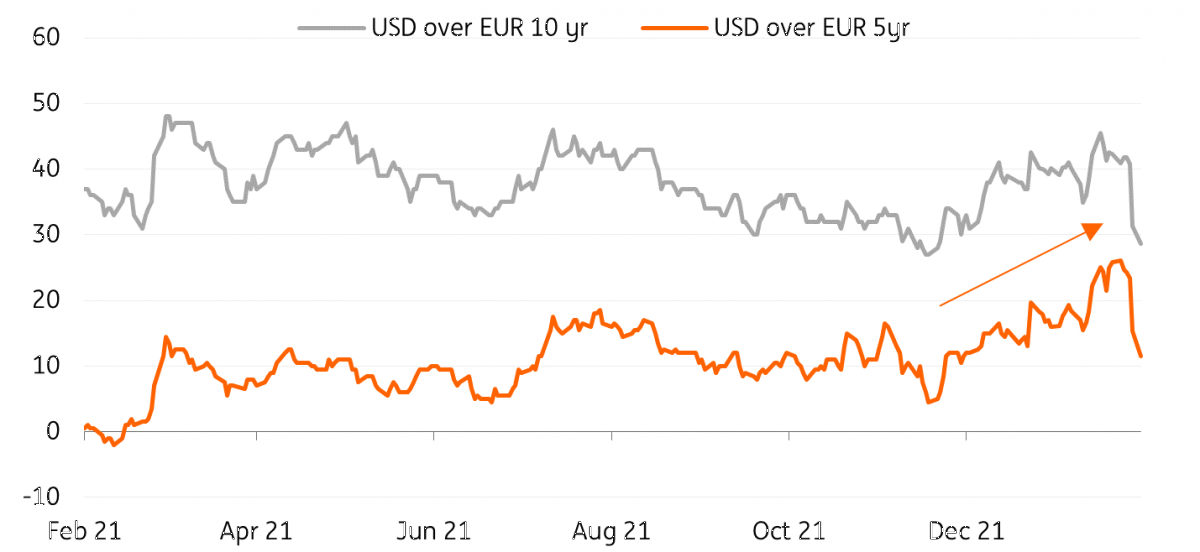

It is interesting to compare the European market to the US dollar (USD) credit market. This is best illustrated by the spread differential between euro (EUR) and USD. USD spreads have been underperforming against EUR spreads since November 2021. Whilst the USD market has not had the same quick sell-off, the direction and magnitude of widening of that market pricing in rate hikes has been similar to what the EUR market has done in a week.

Theoretically, therefore, spreads now represent more value. However, increased volatility means we can expect further widening until the market finds its feet and comes to terms with the new normal of a quicker taper and a sooner end to the CSPP.

Spread differential between USD & EUR

Optimistic for credit

We remain optimistic about EUR credit in finding a new trading range between 84bp and 61bp (using the Bank of America ICE Euro non-financial index). Hence, we outline four reasons why we remain optimistic about EUR credit despite the risks;

- CSPP is still in place until October, albeit at a slower pace. Thereafter, reinvestments will provide some support.

- The differential between USD and EUR spreads will likely see some reversal and widen on the back of continued slow underperformance of USD credit.

- Once credit spreads hit the higher half of the range and begin to settle, we see significant tightening potential. Spreads will be cheap and the market will begin to find its footing around the new normal without the ECB.

- Fundamentals are still strong. Indeed inflation is still a major risk, particularly for some sectors, but balance sheets should be capable of absorbing the shock considering the significant level of cash on balance sheets. Therefore we don’t expect this to lead to any significant downgrades or pressure on fundamentals.

Risks for credit

However, we do see two main risks for credit;

- Excess overselling of ETFs, such that a negative spiral occurs when the cash bond market cannot keep pace with the more liquid ETF market.

- An even quicker tapering and APP ending sooner than now expected and what is being priced in (see our faster taper forecast above).

Positioning

For the time being, we remain selective and more conservative in positioning.

- We see more uncertainty in the long end of the curve. However, we see some value in selective longer issues with high New Issue Premiums (NIPs), which compensate for a curve that we feel will steepen further.

- We see more opportunities in the belly of the curve, specifically the 5-7Y area, which offers an additional cushion. There is more steepening seen between 2-7Y than there is between 2-10Y.

- Additionally, there is a significant roll down between 4Y and 5Y maturities. In spread terms, the 2-4Y area is still looking somewhat expensive when compared to 5Y. We like adding the 1Y extension for the pick-up in both swaps and spreads.

- We expect the short-end to catch an extra bid, now that this area of the curve is yielding positively. Even the 2Y swap rate has come out of negative territory. Spreads on the short-end have been cosmetically wide over the past couple of years, as spreads struggle to tighten when rates are negative.

- We now prefer financials over corporates. The technical picture in corporate credit has weakened, albeit still strong in terms of lower net supply. But more importantly, financials are less inflationary sensitive. This combined with financials now looking cheap compared to corporates drives our expectation for financial outperformance.

- We favour more defensive sectors, avoiding names/sectors that are more inflationary sensitive, more exposed to supply chain shortages and higher energy consumers.

- We maintain our call for preferring Environmental, Social, and Governance (ESG) debt over vanilla and expect slightly less volatility, due to insatiable demand seen both in secondary markets (via inflows into mutual funds) and primary markets (illustrated by larger oversubscriptions and lower NIPs).

- We flip our call and now favour ineligible debt, as CSPP will begin to slow down. Eligible debt is now no longer defensive, and throughout the adjustment phase could see more volatility. We feel there is more value in ineligible debt.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more