Credit Outlook 2024: Carry me home

- 7 November 2023

- Credit

The overriding sentiment for Credit in 2024 is that performance will be dominated by carry. And this year, we have a Q&A-style outlook and stepped away from the theme of 24 calls for 24. The reference to a musical theme continues, and hence the reference to the 'Carry me Home' lyrics. Authorised readers can find the report here under DM Credit

Which legendary song best describes the credit markets for 2024?

There are a multitude of reasons that would encourage us to use a song title that can perhaps best be described as depressing. Think of the likes of Losing my religion as the global slowdown starts to impact Credit metrics and inevitably spreads.

Indeed, there are so many threats circling Fixed Income markets and Credit in particular that one would be forgiven for Losing that religion. And, in the words of the famous song 'The Sound of Silence', it would be easy to say 'Hello Darkness, my Old Friend', particularly thinking about the plethora of challenges credit faces in the form of spreads being at the low end of the fair value range, low beta spread tightness, event risk, real estate question marks, geopolitical tensions but above all higher rates for longer and or the threat of lower growth. Credit metrics surely will be challenged, will they not?

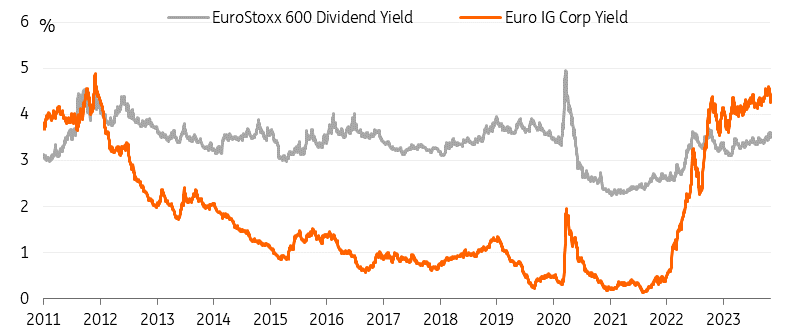

Corporate bond yields in excess of dividend yields

Thankfully, we are of a more positive disposition; we continue to believe that with yields where they are, the almost risk-free return on IG credit will be too scrumptious to ignore. The comparison to dividend yield shown in the chart above also supports strong flows into credit. So, despite all the challenges listed above, it is still the most likely scenario that spread widening will be limited year on year and in any case, underlying rates are set to fall from their current lofty heights. It seems that carry will be key in a defensive portfolio, much like in a rugby lineout. Hence, our choice for the 2024 song title is the US-originated song 'Swing Low Sweet Chariot, Coming for to CARRY Me Home'.

The song originates in US slavery times but has most recently been used as a rugby supporters’ song for the English team. We, of course, favour the Irish green machine, but a black monster in the form of New Zealand got in the way a bit like 'Hello darkness, my old friend'. For Credit and 2024, the lyrics would read a little like this:

Spreads Low Sweet Carry O

Total Yielding for to CARRY me home

Spreads are sometimes up and sometimes down

Coming for to CARRY me home,

But still credit feels heavenly bond,

Coming for to CARRY me home

I looked over Credit Markets, and what did I see

Comin' for to CARRY me home

A band of Technicals comin' after me

Comin' for to CARRY me home

Spreads Low Sweet Carry O

Total Yielding for to CARRY me home

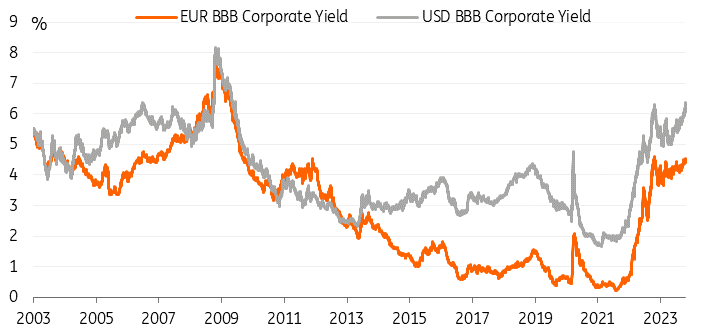

EUR & USD corporate BBB bond yields

How would you rank the largest drivers for credit markets in 2024?

- Rates, with yields backing up drastically in 2023 it’s safe to say that independent of direction, rates will have a huge clearing on credit spread direction for 2024. This, if anything, is therefore the biggest single challenge for next year. For 2024, our economists and rates strategists expect curve steepening, which is consistent with a move away from a hiking cycle and expect rates to fall a little but the theme of higher for longer certainly rings true. For credit, we see inflows as a positive driver due to the level of rates, reasonable pockets of value but it is a fine line as some of the potential spread widening does need to be absorbed by that expected slight fall in rates across the curve.

- Technicals, only a slight increase in supply is expected next year; when we look at redemptions, expected mutual fund and ETF inflows and the, at long last, rising coupon payments, we see a market that’s barely net positive.

- Metrics, credit quality for issuers actually will not suffer that much next year despite a downturn in economic activity, more below.

- Regulation / ESG, Inflows into ESG funds seem to have hit the pause button whilst regulators sort out the taxonomy and other regulatory aspects. We expect this to only be a temporary effect, though.

- Central banks, despite the fact that they hold the power to adjust rates, events in 2023 have given us confidence that the new level of rates will be positive for credit flows and we don’t think quantitative easing, forced selling of credit, ESG or otherwise is on the cards. There's more on this below.

Where do you see spreads going in 2024?

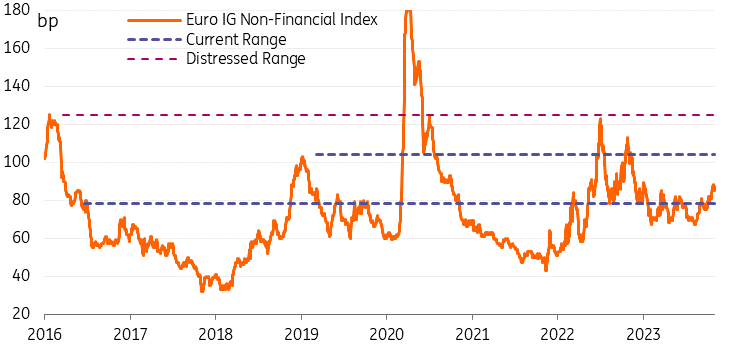

As we indicated right at the beginning of this document its is all about the carry in 2024. We do not believe that credit spreads have the potential to tighten significantly from their current relatively tight levels. The ranges we look at for the ICE index for non-financials (EN00) still trades at the low-end of what we would see as the fair value range of 80- 100bp. A move into squeezed territory with inflationary, economic and higher debt financing costs is not to be expected.

- Carry, insulation of higher yields with yield sensitive buyers, the technical picture all contribute to our belief that despite the fact that credit should widen due to the move into a stagnating economic environment, it will not be a significant move that will be outdone by rates that will have the possibility to move tighter compensating from a total return perspective any small widening.

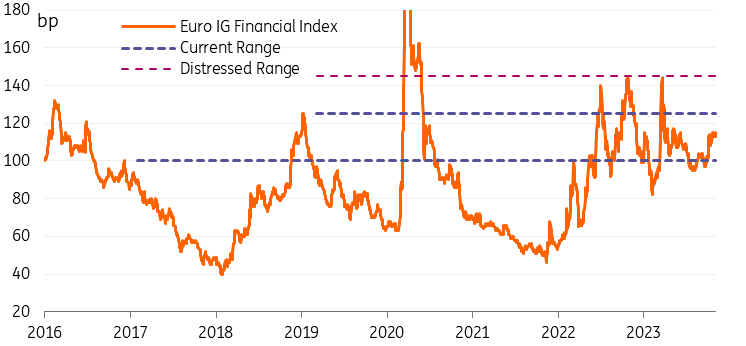

- We see a little more value available in Financials for 2024, trading in the middle of that range and with certain pockets of excellent value such as preferred senior debt (around the 5-7yr area). The tightening potential, as indicated by the chart on the EUR IG Financials range, also clearly shows far more room to perform with spreads currently at over 2.5 times the tightest levels seen in 2022. Corporates don’t even manage to trade at a 2-times multiple compared to those 2022 lows.

All in all, we're mildly bearish on credit spreads but to such a small degree that with the EN00 index currently at 83bp, we expect that to be 90bp at the end of the year.

Look for the DM Credit section

You may be able to access our full report on the ING Research website.

There, we dive in-depth into many topics within Strategy, Financials, Corporates, High Yield and Emerging markets. In our Q&A style report, we answer questions and give investment recommendations on the following:

Jeroen on spread direction, curves, positining, and CARRY

- Net Supply one of the technical positives, redemptions and coupon payments rise.

- Mutual fund flows turn positive too, differences in maturity preference drive positioning.

- Credit Metrics under a little pressure but cash position strength limits damage.

- Active selling based on ESG or lower re-investment risk very limited.

- Spreads to end the year a little wider than where we stand now but carry compensates.

- Real Estate and Higher for Longer main risks to relatively upbeat outlook.

- Credit curves stand to steepen, as rates curves normalise

- Hybrid extension risk still prevalent but manageable, and supply will be limited

Tim on Relative Value, Sectors, Reverse Yankee, Supply and Defaults

- Positioning in the credit markets

- EUR versus USD credit

- Financials versus corporates

- Inflation sensitivity, interest rate sensitivity, supply pressure, energy intensity will all be drivers of certain sectors in 2024.

- Real estate, Industrials, Capital goods, Consumers and Leisure are all inflationary and interest rate sensitive and will be under more pressure.

- Real Estate, Retail, Chemicals, Basic Resources, Metals & Mining and to a lesser extent Autos are the only sectors of concern in terms of leverage metrics.

- Our Sector Scoring - which sectors we are overweight and underweight for 2024

- We forecast €310bn in EUR corporate supply in 2024.

- We forecast US$650bn in USD corporate supply in 2024.

- We forecast €40bn in Reverse Yankee supply in 2024.

- Defaults expected to rise towards 5.5% in Europe and reach 6% in the US.

Maureen on Banks and Covered Bonds

- Easing pressure on yields and wide spreads are supportive of bank bonds in 2024.

- CRE exposures continue to warrant caution if interest rates were to stay high.

- Nordic banks remain most exposed to CRE, but at low NPL levels.

- Our preferred positioning on the liability structrue.

- Realtive value between Covered, preferred, bail-in, T2 (callabel v non-callable) and AT1.

- TLTRO repayments will once again contribute to high covered bond supply in 2024.

- Covered bond spreads will remain on average stable around 30bp.

- A dive into positioning in covered bonds.

- ESG supply by banks will stay high at €75bn.

Suvi on Banks

- Bank bond issuance will remain high in 2024.

- Higher issuance in unsecured debt, and in particular in preferred senior debt, is likely to offset the slump in covered bond issuance in 2024.

- Banks are likely to jump on the possibility to print capital to prepare for the looming redemptions both in 2024 and in 2025.

- Smaller, lower rated banks may struggle to refinance their AT1, pushing extension risk higher, but we expect most banks to seek to call their capital at first call date.

- We expect competition for bank deposits to intensify in 2024.

- The tightening ECB monetary policy stance poses a risk for bank liquidity in 2024.

- The runoff of the TLTRO-III programme will pressure liquidity positions, Italian and German banks are most impacted due to the combination of their large LTRO drawings and more limited LCR buffers than other comps.

- The potential changes to the level of Minimum Required Reserves could come with additional unintended consequences with in particular Italian banks at risk.

- Our Picks & Pans for Banks.

Marine on Banks and Regulation

- Banks with a larger share of real estate in their portfolio are expected to disclose a higher GAR in 2024.

- No systematic effect of Taxonomy-eligible disclosures is seen on bail-in bonds performance yet.

- The impact is likely to be more important on vanilla issues as green bonds are already showing a greenium.

Nadège on Energy, Utilities and ESG supply

- Energy prices to remain elevated in 2024.

- Oil & gas majors’ capex grows, cash flow generation flat.

- We are marketweight the € IG utilities sector with supply to reach €55bn.

- Corporates ESG € bonds to marginally grow to €90bn.

- ESG bonds book subscription to stay high.

- Our Picks and Pans for the Utility sector

Jan on Telecom, Media and Technology

- We deem the core European telecom space as being stable.

- Some names, however, look relatively unattractive.

- We do not see a catalyst for spread performance of US issuers under our coverage.

- We think names in the technology space are solid while attractive entry points arrive from time to time.

- The names provided above show the Benelux is an attractive space to park cash.

- Our Picks and Pans for the TMT sector.

Jesse on Real Estate

- I would highlight for the real estate sector in 2024: refinancing and maturity management, pressure on credit metrics and operational performance.

- From a geographical perspective, I think the Nordics, Germany and the US will be most in focus. In the Nordics and Germany, rapid rises in funding costs and steep valuation declines could put more pressure on ratings.

- In the US, the market is experiencing a lot of volatility, particularly in the office segment. Rising impairment costs for banks highlight the worsening financing environment here.

- On the other hand, I believe that many companies will continue to take decisive action to manage pressure on credit metrics and that investor sentiment could turn more positive in 2024.

- We see supply increasing to €12bn in 2024, albeit still much lower than pre-2022 levels. Net supply is still expected to be negative at €-8bn.

- Picks and Pans for the Real Estate sector.

Oleksiy on Autos & European High Yield

- We are Market Weight on the Auto sector in 2024 as we anticipate a slowdown in the pace of sales and production growth relative to the current year.

- We assume that global car sales will have a modest but positive momentum in 2024.

- We believe that some of the crossover Auto sector names have a propensity to be upgraded to investment grade territory during the year.

- Our Picks and Pans for the Autos parts manufacturers.

- Our base-case scenario assumes another year of mid-single digit positive return for the European high yield in 2024.

- We expect gross corporate EUR-denominated high yield issuance of €50bn in 2024.

- Our preferred positioining in the High Yield market

Egor on CEEMEA corporates

- Corporate spreads of CEEMEA issuers will be slightly tighter spreads in IG credits and up to +50-150bp wider corporate spreads among HY credits.

- New issue supply will be subdued by elevated base rates and geopolitical risks in the first half 2024, while I see more chances for healthy supply in the 2H24.

- Tight refinancing conditions, geopolitics, corporate governance and ESG risks will determine negative rating changes and growth of default rates across the region.

- Our Picks and Pans for both the IG EM space and HY EM space.

Authorised readers can find the report under DM Credit on our Research website here.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more