Credit Outlook 2022: Demand for ESG is insatiable

- 12 November 2021

- Credit Sustainability

Demand for Environmental, Social and Governance (ESG) bonds continues to grow rapidly. Therefore, we expect ESG to outperform in secondary markets in 2022

Surging demand

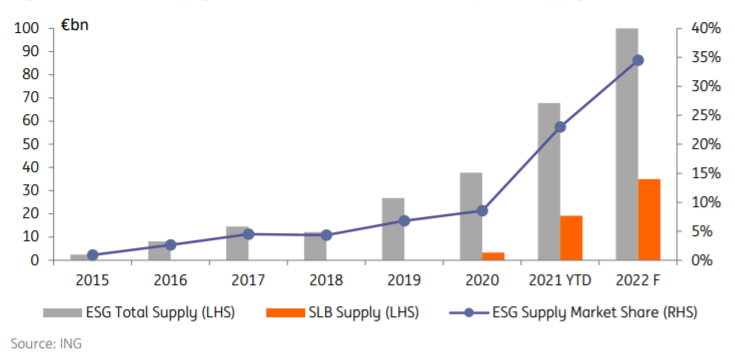

Corporate ESG supply is set to increase to €100bn in 2022, of which €35bn is from sustainability-linked bonds. This will account for 35% of total corporate supply in 2022. Demand for ESG continues to grow rapidly. Therefore, we expect ESG to outperform in secondary markets in 2022, despite having little greenium now. The outperformance of ESG in primary markets is expected to continue, with relatively higher oversubscriptions and more greenium being priced in.

As it stands, there is very little spread differential between ESG and vanilla bonds. This is due to the compression of spreads over the past months, resulting in little differential between most sectors, ratings and durations. However, we do expect greenium will increase in 2022, with ESG spreads outperforming.

Issuers and investors alike are embracing ESG as core financing or investment philosophies. Covid has acted as a catalyst for that higher ESG demand, and longer term, we believe ESG will outperform as demand is insatiable and supply is lagging behind. Fund flows, supply and regulation are all driving the trend.

ESG vs overall index shows very little greenium

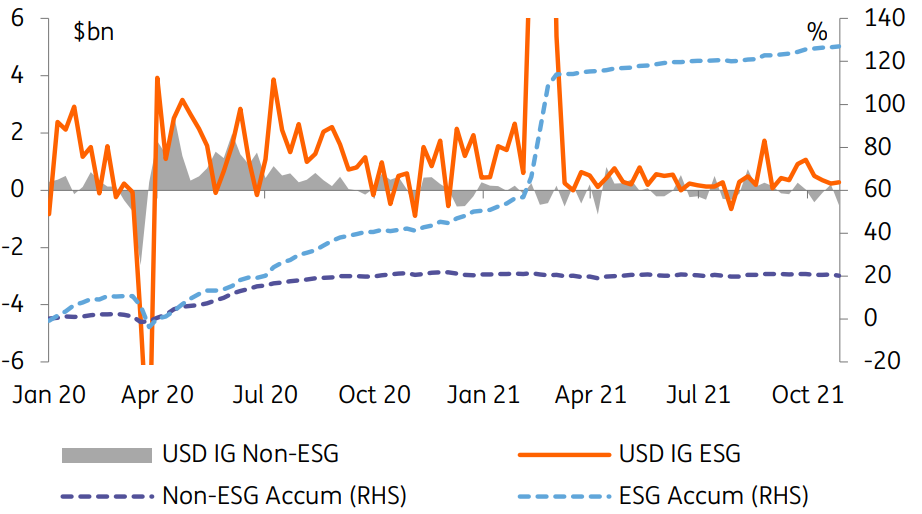

As we see in the figures below, the majority of the inflows seen in Euro IG funds have been into ESG funds. In fact, non-ESG funds have generally seen outflows. It is also visible that most outflows seen from non-ESG funds have been swapped over to ESG funds in the same asset class. This was largely seen after the outflows during the beginning of the Covid crisis.

Inflows into ESG funds have accumulated to a substantial 57.3% of assets under management since the start of 2020. Meanwhile, specifically non-ESG funds have seen outflows of 1.8% of AuM. Similarly, in USD, ESG funds have seen inflows of 126.9% of AuM. Non-ESG funds, however, were still high at 20.3% of AuM.

EUR ESG mutual fund inflows

USD ESG mutual fund inflows

Despite the lack of greenium being priced into secondary markets, ESG has seen outperformance in primary markets. As illustrated in the two charts below, ESG bonds have constantly been oversubscribed relative to vanilla bonds and have seen more greenium being priced in relative to vanilla. Sustainable linked bonds singularly are just slightly below ESG in both. This will continue into 2022, and we may see further outperformance in the case of more turbulent market conditions.

Higher oversubscription for ESG and SLBs

NIP in ESG and SLBs

In 2022, we expect the green, social, sustainability and sustainable-linked bonds market to continue to grow as the pressure from societies, governments, activists and the new EU requirements for ESG reporting accelerate. We forecast Euro ESG corporate supply to hit €100bn in 2022, with €35bn coming from SLBs. We believe that the Energy sector will continue to drive the surge with a c.€45bn of ESG issuance as projects and capital expenditure dedicated to the energy transition rise.

Euro ESG supply to account for 35% of total corporate supply in 2022

This article was first published as part of our Credit Outlook 2022. You may be able to access that on our investment research website here, but MiFID and other restrictions may apply.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more