Coronavirus ‘fear factor’ is the biggest risk to the economy

- 7 February 2020

The coronavirus has already hit domestic demand in China, as well as supply chains further afield. But if the outbreak becomes more widespread overseas, the major risk is 'fear', and this could begin to take its toll on consumer spending growth among developed economies

What’s the latest?

The rapid spread of the coronavirus (nCov) throughout China is quickly becoming a major source of uncertainty for the economy. Markets – most notably commodities – have taken a hit as concerns over demand become more widespread.

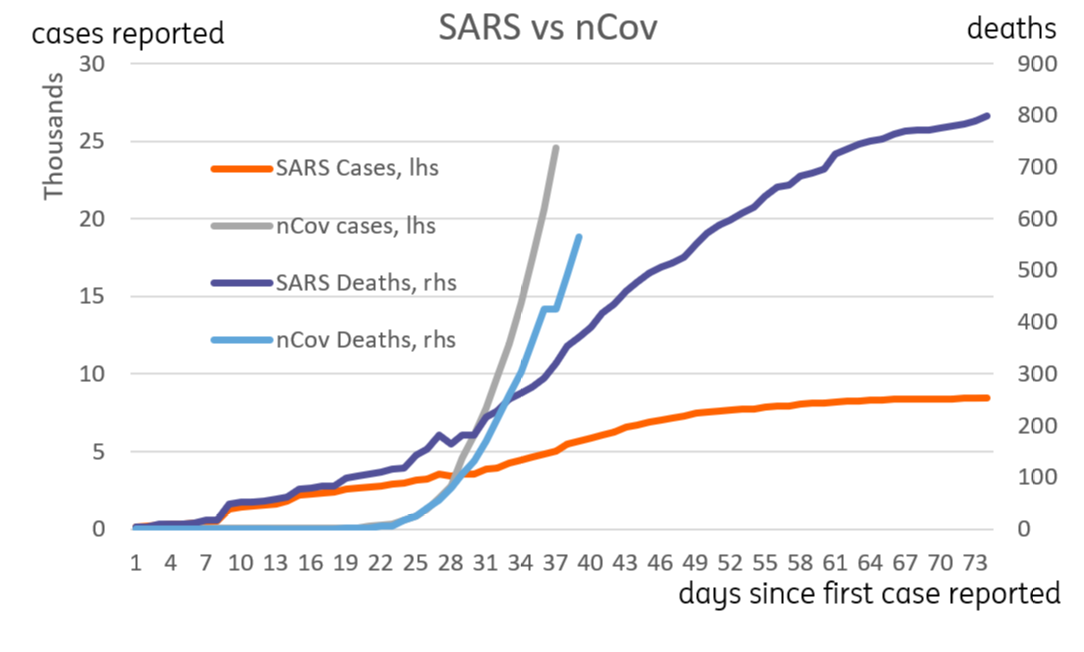

Comparisons are naturally being made to SARS back in 2003, and the early data suggests that nCov is proving less fatal (the mortality rate is around 2% so far), but importantly it is much more infectious. The number of nCov cases is already far in excess of SARS at the same point in time after the first case was reported.

If there’s one glimmer of hope, it’s that the rate of change in cases each day has not gone exponential, though these trends can change rapidly.

While this may tentatively hint that the virus has been contained, the reality is we still don’t know just how far the virus has spread outside of China. The number of cases confirmed overseas is still limited - especially outside of Asia - but the total is now over 200 and rising. Many of these, however, were visiting Chinese tourists. Cases of community transmission remain low.

Given the virus has a 14-day incubation period, the full spread may only become apparent over coming days. And despite market optimism on potential vaccines, it could be several months before these can come into use.

Growth in coronavirus cases compared to SARs

What’s been the impact so far for the global economy?

As Iris Pang notes in this month’s economic update, Chinese retail and associated services have felt the immediate brunt of the virus. From shops to restaurants, a lack of footfall is hitting sales, while a sharp fall in inbound tourism will also take its toll.

But as time goes on, supply chain disruption will become a bigger concern globally. China is much more integrated into the global economy than it was back in 2003 when the SARS virus hit. A sustained drop in Chinese production of electrical components could quickly cause knock-on effects elsewhere. Production outages have already forced carmaker Hyundai to close South Korean factories owing to a lack of Chinese components.

Carsten Brzeski reckons this could be yet another headache for German industry, where the latest data suggests the sector is still experiencing sharp order book deterioration.

World trade growth will inevitably suffer, particularly if marine shipments are cancelled and air freight becomes more restrictive. Our trade team notes that capacity constraints within global logistics mean the current fall in trade volumes might not be made up quickly later in the year.

What would a global pandemic mean for global growth?

If the number of cases begins to surge outside of China, one of the principle channels of transmission to the economy will be through “fear”. Fear of catching the virus results in a change in household behaviour that is arguably disproportionate to the chances of either catching the disease, or of dying from it.

That change in behaviour typically manifests through a very substantial decline in consumption of consumer services. Spending on recreation (cinema, theatre), transport (public), eating out and accommodation, could be particularly vulnerable.

Our latest forecasts assume that the epidemic is not contained within China, and there is some ‘community transmission’ in major economies. Taking the US as a guide, we reckon roughly 18-20% of consumer spending is directly exposed to the ‘fear’ factor. A 5% fall in those categories could quickly see around 1% knocked off consumer spending. This is a worry given that consumer spending has been a key growth driver throughout the developed world over recent years, often in the absence of investment and net export growth.

The spread would inevitably hit other sectors, too. Some airlines are already furloughing staff in the region as they cancel flights. And some imports of commodity goods and fuels have been rejected with a force majeure as demand slumps and storage facilities reach capacity.

Our latest forecasts assume that the epidemic is not contained within China

As always with shocks like this, it’s fair to say there is limited scope for policy responses in some countries. Interest rates are low or negative in many advanced economies, while fiscal policy is bound by political constraints (e.g. US), regulatory ones (e.g. EU) or structural (e.g. Japan).

This situation is especially unfortunate since the improvement in US-China trade relations was expected to reduce uncertainty and provide a platform for stronger global growth for 2020. White House officials have acknowledged that the impact on the Chinese economy means that the predicted US “export boom” will be less than hoped, but are keen to emphasise the situation should not be used as an excuse by China to backtrack on commitments made as part of the deal.

What would a widespread pandemic mean for markets?

A generalised shift to risk aversion will likely see equity markets sell off, though how far they fall may be highly dependent on how stretched their valuations had previously been, so US markets may be more exposed here than some in Europe or Asia. In general, we would expect EM currencies to underperform those of the DM universe which also may hinder the ability of local central banks to respond to weak domestic demand with more accommodative policies. Reliance on commodity exports is another factor that could affect the resilience of an economy, and its asset and FX performance.

Government bond yields will also likely fall further in the short term, which on the one hand will likely see more accommodative financial conditions, but if accompanied by a sell-off in riskier high yield credits could more than undo that result, spreading further pain through the business channels – which are already very weak in many parts.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Gauging the cost of the coronavirus

- This bundle contains 7 Articles