Why commercial real estate concerns haven’t subsided for banks just yet

- 30 October 2023

- Financial Institutions Real estate

The softness in the commercial real estate market is not a concern of the past yet. Nordic banks remain most exposed to the CRE sector, but when it comes to climate change transition risks, these assets do not appear to be among the most vulnerable in Europe

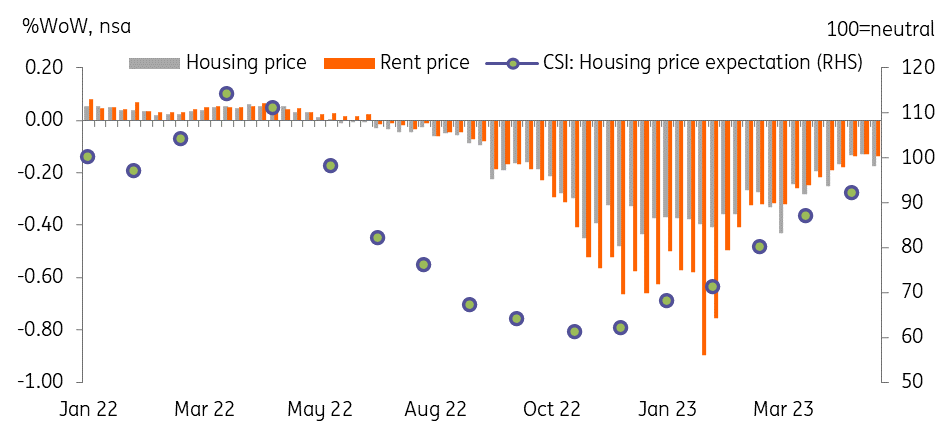

Since central banks aggressively started hiking rates to fight rising inflation levels, commercial real estate (CRE) has been a key area of concern. Rising interest rate levels and a declining need for office space (due to the effects of working from home) have caused vacancy rates to rise and property values to decline. While the worst price declines are levelling off, concerns remain over tougher financing conditions and that high CRE debt maturities will continue to exert pressure on the heavily debt-reliant CRE sector.

The increased presence of real estate investment trusts (REITs) in commercial real estate adds an extra layer of concern, especially if these companies need to sell properties to meet their forthcoming redemption payments. Real estate investment volumes are declining and climate transition risks are looming, but it is reassuring that rental income growth remains stable. Banks are also much better capitalised now than during the financial crisis. That said, supervisors remain alert regarding the stresses that may arise from the commercial real estate sector – particularly if interest rate levels stay high for a long period in what is a still very uncertain geopolitical, inflationary, and economic environment.

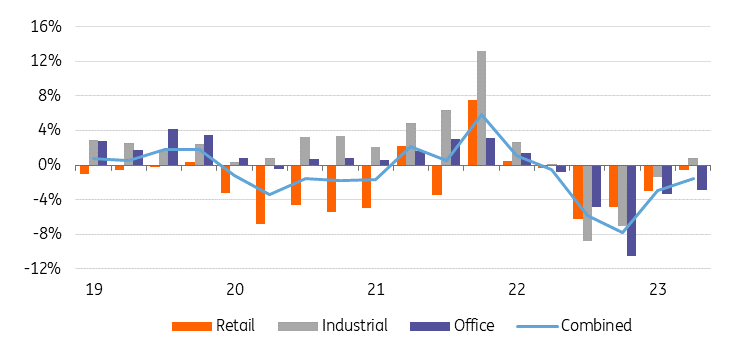

Worst price declines appear to be over in commercial real estate

EU-15 prime capital value index, QoQ change

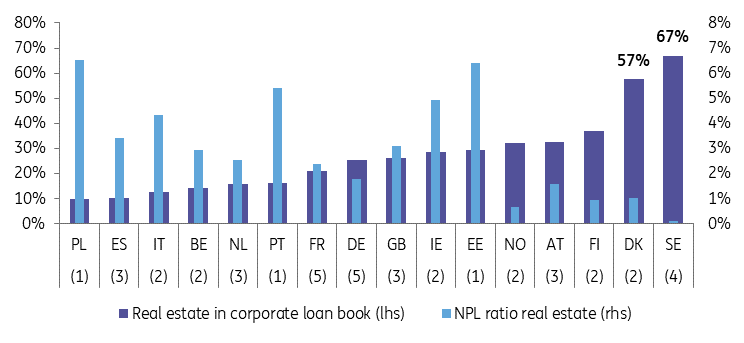

Nordic banks remain most exposed to commercial real estate firms

While many banks reduced their commercial real estate exposures over the past decade and became stricter on their lending conditions, loans to the CRE sector still represent around 30% of corporate lending books for European banks. However, exposures differ substantially from country to country. In Nordic countries such as Sweden and Denmark, loans to CRE companies comprise 57% and 67% respectively of bank loans to non-financial companies. In Spain and Italy, only 10% and 13% of banks’ corporate lending books are loans to CRE companies.

Despite the substantial exposures of Nordic banks to the CRE segment, the performance of these CRE loans remains solid so far. Swedish banks report the lowest NPL ratios for their corporate real estate exposures, closely followed by Nordic peers from Norway, Finland and Denmark. Austrian and German banks also report modest NPL ratios on their loans to CRE companies. The highest CRE NPLs are recorded by Polish, Estonian, Portuguese and Irish banks.

Nordic banks have high exposure to the CRE sector but with low NPLs

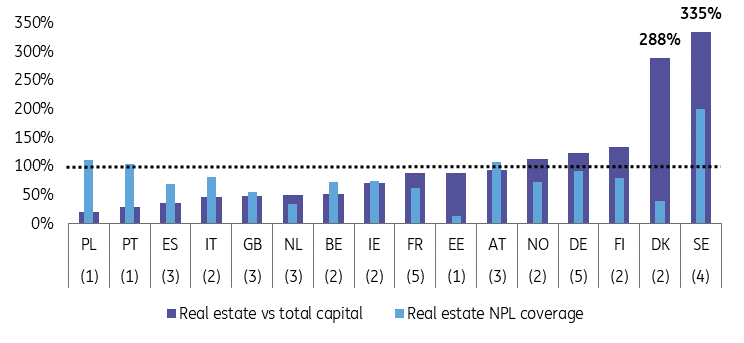

Even though CRE loan performance remains reassuring for Nordic banks, it is no surprise that supervisors still pay close attention to commercial real estate market developments. For Danish and Swedish banks, exposures to commercial real estate companies are around threefold the size of their capital stack. Severe troubles in the CRE sector – resulting in notable write-offs and provisioning on loans to CRE companies – could form quite a risk, even to these well-capitalised banks versus risk-weighted assets.

Most Swedish banks have already set aside quite sizeable provisions to cover non-performing CRE exposures. They distinguish themselves in that regard from Danish peers who have taken fewer impairment provisions against their outstanding CRE loans. That said, in Denmark, the Systemic Risk Council recently recommended to introduce a 7% sector-specific systemic risk buffer for bank exposures to real estate companies from 30 June 2024. Such a buffer would serve to improve bank capitalisation levels to better withstand impairment charges and losses on loans to commercial real estate firms.

CRE activities are about 3x the capital stack of Danish and Swedish banks, but Swedish banks have better NPL coverage

Property price developments matter for CRE collateralised loans

Properties that are pledged as collateral for loans to commercial real estate companies form an important security against a rise in non-performing loans. This does not only hold for loans to CRE companies, but also applies to the other parts of the corporate lending books secured by commercial real estate.

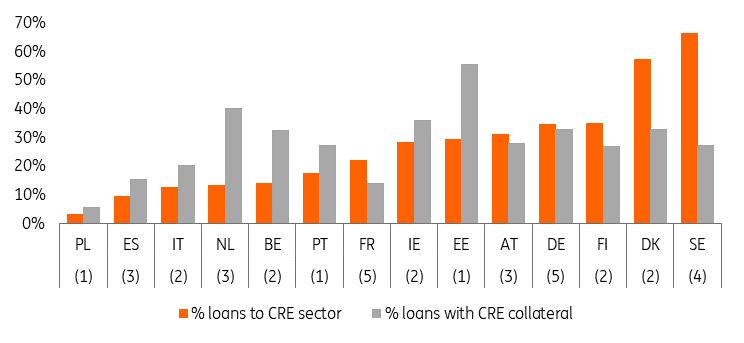

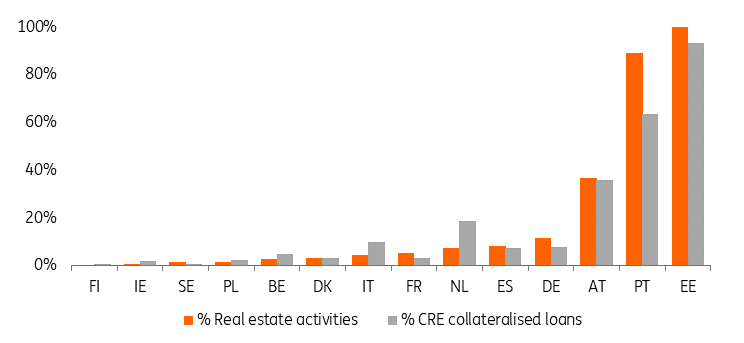

CRE collateralised loans have a relatively prominent position in the corporate loan books of Benelux banks, even though these banks have lesser direct exposure to CRE firms. Banking sectors with higher exposures to commercial real estate companies are indeed also among the banks with relatively higher shares of CRE collateralised loans, a sign that the loans to commercial real estate companies are often collateralised.

Exposures to the CRE sector versus CRE collateralized corporate loans

% of non-financial corporate exposures

The commercial real estate collateral should protect banks against loan losses in the event of company defaults. However, the loan recovery prospects become worse if the value of the commercial real estate collateral declines significantly. The effect on banks of worsening conditions in the CRE market therefore stretches beyond their direct exposures to commercial real estate firms alone.

Corporate loan performance has remained relatively stable in the past two years. However, the trend is turning worse with our credit strategists expecting European speculative-grade default rates to rise to 5.5% in 2024 (see here). With corporate default rates on the rise, the collateral value of commercial real estate becomes an increasingly important backstop, even for banks with less direct exposure to CRE companies.

Real estate valuations may overestimate true value

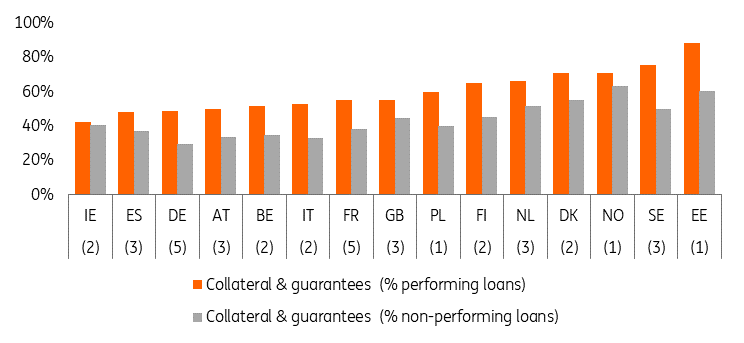

The security offered by real estate collateral, or by financial guarantees for that matter, is generally reflected in a lower percentage of corporate loans being earmarked as increased credit risks (stage 2) or credit impaired (stage 3). If the value of the security becomes less, this could coincide with a deterioration in loan performance and rising impairments. This will impact banks that rely relatively heavily on real estate collateral.

Fewer stage 2 & 3 loans if there is more security from collateral

% of non-financial corporate exposures

Commercial real estate loans usually have a decent cushion against property price declines due to their on average low loan-to-value (LTV) ratios. These LTV levels have improved further during the past decade of low interest rates and property price rises. In its May 2023 Financial Stability Review, the European Central Bank (ECB) showed that more than 60% of the CRE loans in the eurozone had LTV levels below 60% at the end of 2022, while little more than 10% of the CRE loans had LTV levels of more than 100%.

Nevertheless, collateral valuation risks have emerged as one of the top supervisory priorities for the ECB. In an August 2022 supervision letter, the central bank identified collateral valuation as a blind spot for various banks. On-site inspections revealed flaws in the updating of appraisal reports as per the CRR and in ad-hoc revaluations upon changed market conditions. The ECB is also concerned that valuation approaches and inadequate parameters give rise to a significant asset overstatement.

These concerns could at some point lead to more aggressive valuation adjustments by banks on their commercial real estate collateral. This may cause provisions to rise, for instance, if certain LTV covenants were to be breached. We do note however, that alongside LTVs, debt servicing indicators such as interest rate coverage ratios (ICR) have become increasingly important for the assessment of default risks related to CRE corporates. (See also our note here, which focuses on bond covenants in the CRE sector).

Valuation requirements under the CRR

Article 208 of the EU capital requirements regulation (CRR) requires commercial property values to be monitored on a frequent basis, and at least once a year. If there are signs of a material decline in property values relative to general market prices, property values must be reviewed by a qualified valuer. For loans exceeding €3m or 5% of own funds, an appraisal review should take place at least every three years. Moreover, CRR Article 229 requires properties to be valued at or less than the market value or the mortgage lending value. The value of collateral should be reduced as appropriate to reflect the results of the monitoring.

With the implementation of the Basel III reforms, the CRR will be amended to reduce the impact of cyclical effects on property valuation and keep the own funds requirements on mortgages more stable. Upward revisions to commercial real estate values will for instance be restricted versus the original value of the properties to the average value over the last eight years. Upward price modifications can however be made to above this average value if they are the outcome of energy efficiency improvements to the building.

(See for a further discussion of the CRR review the article linked here).

Commercial real estate collateral values also tend to be adjusted lower once corporate counterparties default. This too may deteriorate the recovery prospects on the loans if the bank were to move forward on selling the collateral to recover (part of) the loan.

Security from collateral and guarantees is lower for NPLs

% of performing and non-performing non-financial corporate exposures

The impact of climate change on commercial real estate assets

Climate change can act as a further source of pressure on the commercial real estate market. Physical climate risks such as sea level rise (chronic) or wildfires, storms, floods, drought, and subsidence (acute) can cause severe damage to properties. Besides, energy-inefficient buildings can lose value due to their higher energy consumption costs, or by not transitioning in time to meet the energy performance targets set by regulators (transition risks). Renovating or replacing inefficient buildings also brings extra costs at a time when company earnings are already under pressure from higher energy prices, wage rises and funding cost increases.

Since the end of 2022, European banks have reported on a subset of climate risk metrics via their Pillar 3 disclosures. These disclosures encompass physical and transition risk indicators for commercial real estate activities and CRE collateralised loans. The first disclosures still heavily rely on estimates, making it difficult to draw valuable conclusions. Besides, the physical climate risk assessments of banks are based on a broad variety of assumptions and approaches, sometimes resulting in substantial reporting differences.

Finnish and Estonian bank disclosures (almost neighbouring countries) form two reporting extremes on physical climate risks. Finnish banks classify only a few real estate assets as exposed to physical climate risks, while a very high portion of Estonian commercial real estate assets is assumed vulnerable to chronic and acute physical climate risks. Adjusting for the high physical risk outliers, real estate assets of German, Spanish and Dutch banks appear to be a tad more sensitive to physical climate risks.

The physical climate risk assessment differs widely among banks, with Finnish and Estonian banks at the extremes

Physical climate risk as % of real estate exposures

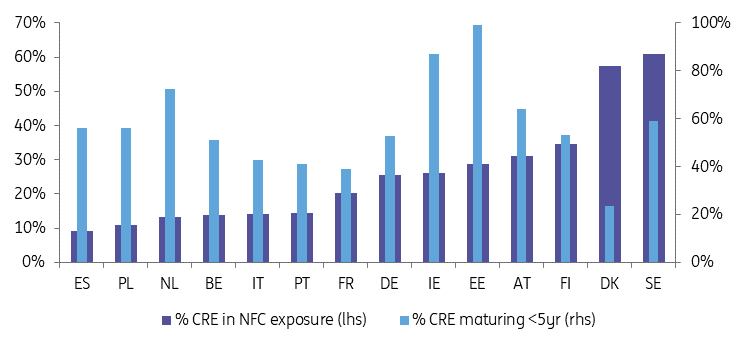

The disclosures on transition risks confirm that a significant part of the CRE sector exposures of European banks will expire within five years’ time. While this may exert unwanted pressure on these loans from a refinancing perspective, it is positive from a transition risk point of view. If the maturities of the CRE exposures are shorter, banks have an earlier opportunity to renegotiate the loan terms for stricter environmental requirements. This is supportive of the decarbonisation targets of banks. The commercial real estate exposures of Danish banks look somewhat more sensitive to transition risks, as the maturity of these loans mostly stretches beyond five years.

CRE sector important to transition risk exposures of the Nordic banks, but most CRE exposures mature within 5yr

Transition risk as measured by the maturity of CRE activities

The energy performance disclosures by banks on their CRE collateralised loans offer further clues on the transition risks for the commercial real estate assets of banks. These disclosures use both energy performance certificate (EPC) labels and energy performance scores.

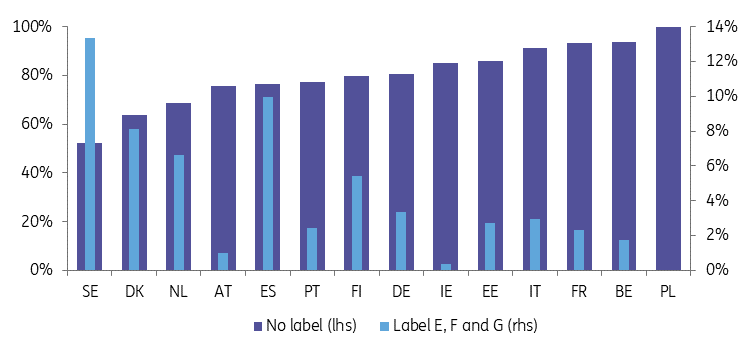

The statistics confirm the poor data availability of EPC labels in most countries. Swedish banks have a relatively decent 48% EPC label coverage for their CRE collateralised loans, but there is no EPC label coverage at all in Poland and only a 6% EPC label usage by Belgian banks. Banks with the ability to use EPC labels also tend to disclose a higher percentage of loans in the less energy-efficient EPC label E, F and G buckets which are the most exposed to transition risks. This likely reflects the broader EPC label coverage of commercial real estate in these countries, including for older dated and less energy-efficient properties.

Another well-known issue with the use of EPC labels is the lack of comparability of the definitions used. This makes it difficult to draw conclusions based on these statistics. Against this backdrop, it is a bit of a setback that the rescaling of EPC labels as per the initial revamp proposals to the Energy Performance of Buildings Directive (EPBD) seems to be off the table. The original proposals not only facilitated a better accessibility of labels but also a harmonisation of EPC label scales.

Banks from markets with better EPC label availability appear worse positioned on transition risk

Swedish and Spanish banks have the highest shares of E, F and G labelled properties

The energy performance scores may give a better idea of the transition risk exposures of commercial real estate collateral. While these scores are still largely based on estimates, they do cover the full commercial real estate collateralised loan portfolio and are better comparable in terms of actual energy demand. These energy performance scores identify CRE properties in Portugal and Ireland to be most exposed to transition risks. German, Spanish and Nordic banks score best, with a higher share of their CRE collateralised loans included in the better <100 kWh/m2 energy performance bucket.

Energy performance scores of CRE collateral see least transition risks arise for German banks

Energy performance in kWh/m2 of collateral

Based on this, we can draw the cautious conclusion that banking sectors with large commercial real estate exposures are probably not those most sensitive to climate transition risks.

The spillover consequences of CRE concerns to funding costs

Higher exposure to companies in the CRE sector does come at a funding cost disadvantage. Credit spreads are currently wider for banks with more CRE loans on their balance sheet than for banks with less CRE exposure, which is even more so the case for bonds issued by banks further down the liability structure.

The two graphics below illustrate the 5yr equivalent asset swap spread levels for the preferred senior unsecured and bail-in senior unsecured bonds of a sample of European banks. The charts distinguish banks with less than 20% exposure to CRE firms, from banks with 20-50% CRE exposure and banks with more than 50% CRE exposure. The spread levels are plotted against the average ratings of the bond instruments.

The funding cost impact of higher CRE exposures is modest in preferred senior

5yr equivalent preferred senior unsecured asset swap spreads, in basis points

There is more funding cost disadvantage to higher CRE exposures in bail-in senior

5yr equivalent bail-in senior unsecured asset swap spreads, in basis points

The charts confirm the wider asset swap spread levels for banks with more than 50% CRE exposure in both the preferred and bail-in senior unsecured bond markets. Banks within the 20-50% CRE bucket also have in most cases higher credit risk premiums on their bail-in senior liabilities than banks with less than 20% CRE exposure.

This shows that commercial real estate-related risks are already partially reflected in bond market funding levels. That said, we do believe that spreads will widen more if the credit metrics of the banks come under stronger pressure from CRE-related problems. If CRE concerns were to ease convincingly, banks with more CRE exposures should benefit from a decline in the CRE risk premium.

Conclusion

While the worst price declines in commercial real estate are levelling off, supervisors and market participants stay vigilant regarding the developments in the CRE market. Nordic banks are among the most exposed to turmoil in the CRE sector, but the performance of their CRE loan books remains solid so far. These banks also do not appear to be among those most exposed to CRE-related climate risks. The bond market already prices in a certain CRE risk premium, offering some cushion if commercial real estate were to become a more serious concern for bank fundamentals. That said, this risk premium is unlikely to be enough to prevent credit spreads from widening further if stresses in the CRE sector build up.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Banks Outlook 2024: A world of higher for longer

- This bundle contains 7 Articles