CNB preview: Past and future inflation perceptions set the pace of easing

The residual inflationary hotspots have been broadly extinguished, but future price pressures seem to be building, warranting a more cautious approach with a 25bp cut to 5%. Support for the fragile recovery is tempting, yet price stability is at the heart of the Czech National Bank’s mandate

Monetary policy conditions are restrictive with investment in the spotlight

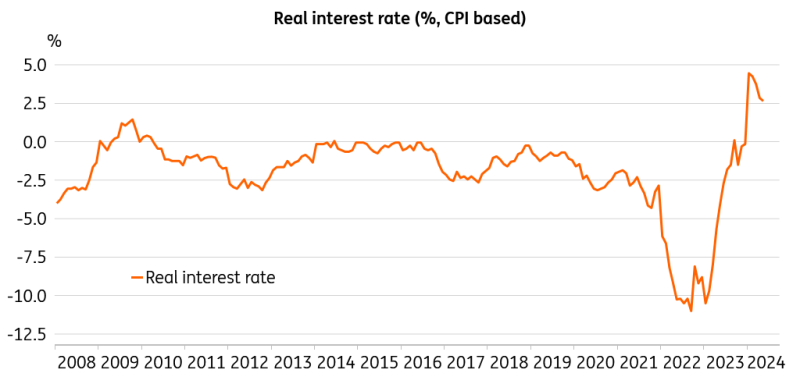

There is no doubt that the monetary policy stance is currently restrictive for the Czech economy, especially by historical standards. The real interest rate, calculated as the difference between the nominal rate and annual consumer inflation, has been mostly negative since the financial crisis. Buoyant consumer price growth has even brought real rates below the negative 10% threshold in recent years, cutting deep into the real purchasing power of household savings. The current real rate level of +2.9% has lifted savings to levels not seen in a long time. At the same time, it sets a high bar for competition that viable investments can cross. Elevated interest rates are likely impeding consumer spending and disincentivising investment. Governor Ales Michl made it clear that both 25bp and 50bp are perfectly possible, and Vice Governor Eva Zamrazilova confirmed this as her take for the upcoming decision on 27 June.

Real interest rates are elevated and restrictive

But are somewhat higher interest rates necessarily a bad idea per se? The inflationary Tsunami, which has hammered all participants of day-to-day economic life in recent years and still represents a burden to lower-income households, suggests that positive real interest rates are perhaps not such a terrible idea overall. A positive real rate sets a welcome competition bar for viable and efficient business ideas and investments. It also keeps the economy from overheating, which could occur rather swiftly and unexpectedly. That said, advanced economies have recently moved toward setting a higher standard in terms of interest cost, while China, for example, has moved in the opposite direction.

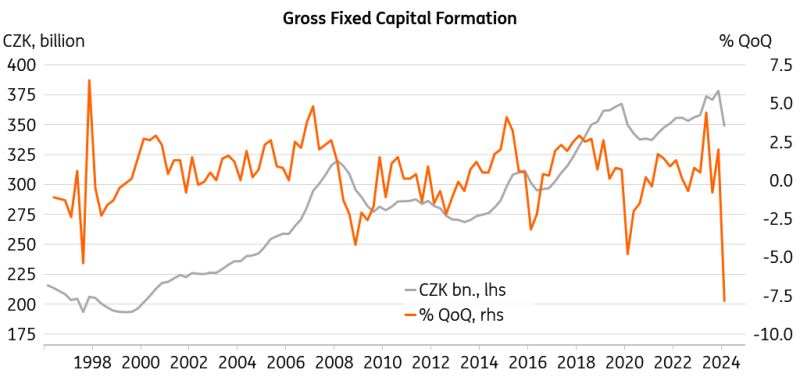

Weak investment and stagnating industrial production are set to enter the decision function of the CNB's bank board as a high priority at the upcoming meeting. Czech companies are currently sitting on rather non-negligible financial resources. So, is the high interest rate to blame for the firms hoarding cash and collecting a fat real interest? It seems there are also other reasons of a structural nature and continued uncertainty about the economic rebound in Europe rather than financing constraints.

Fixed investment dropped to 2018 levels

Czech companies are simply neglecting to develop the core of their business activity, which is not very strategic with respect to future developments. Competition does not slow down, especially in a globalised market. The fight for market share is raging all the time. If Czech companies want to disappear into the abyss of history, they can well continue in the current modus operandi of non-investment. However, they must not be surprised that the world has moved on, while they are merely standing by. The main reasons for the anaemic investment in the Czech Republic are found in places other than elevated interest rates. For example, the significant level of European regulation, uncertainty about future energy prices, and administrative hurdles such as never-ending construction permit procedures and a slow judiciary have all weighed on business investment.

So, what is the appropriate pace to ease monetary policy conditions?

Inflation remaining within the upper segment of the CNB's tolerance band, the mediocre investment performance, and the still-fragile economic recovery are encouraging a faster pace of policy rate cuts, say by 50bp at the upcoming board meeting. Price trends in both goods and services have already weakened significantly. Meanwhile, weaker growth in goods prices by up to 1% annually combined with faster growth in services prices by up to 4% creates an unexpected picture for an economy remaining on a trajectory of price convergence towards more advanced economies. Indeed, the hotspots of the past inflationary inferno can be considered broadly extinguished.

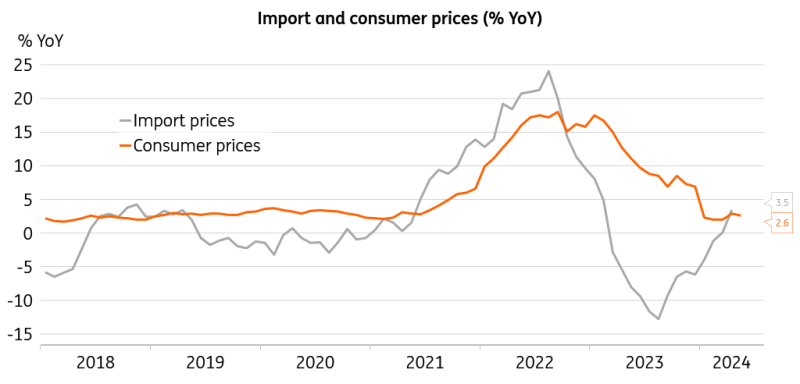

Import prices return to growth and will impact consumer prices

In contrast, strong nominal wage growth is rolling through the economy amid a still-tight labour market. We observe a solid recovery in consumer spending, which will continue to benefit from the fresh and buoyant real wage growth. Household consumption and nominal wage growth came in above the CNB's and financial market expectations, with both of these underpinning future upward pressures on consumer prices. Wages in industry rose 10% from a year earlier in April, while wage hikes in construction were just a tick behind. That said, import prices have once again entered the growth area, which will to some extent mirror shelf prices with some delay.

A more gradual reduction in the monetary policy rate seems more forward-looking

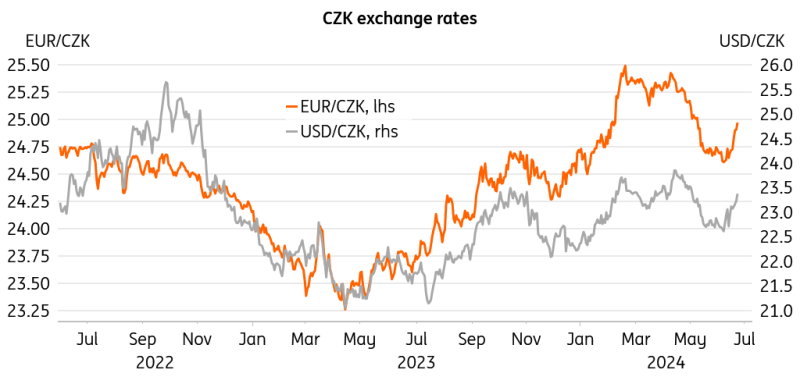

The fact that major monetary institutions in advanced economies are not in a hurry to cut rates may also contribute to a more cautious reduction in the key interest rate. While the European Central Bank has recently cut interest rates, the Federal Reserve is still in wait-and-see mode. The ECB is watching the Fed, and the CNB is watching the ECB. After all, the interest rate differential and exchange rate are in play, one of the ultimate prices for any economy. After its appreciation during the past two months, the koruna has been weakening in recent days, which is only adding fuel to the smouldering import prices. The governor has often pledged the necessary caution vis-a-vis the possible build-up of inflationary pressures, as he is certainly not keen on seeing inflation crawling above the upper margin of the tolerance band. Delivering the proclaimed caution would likely benefit his credibility.

The strengthening of koruna has reversed in recent days

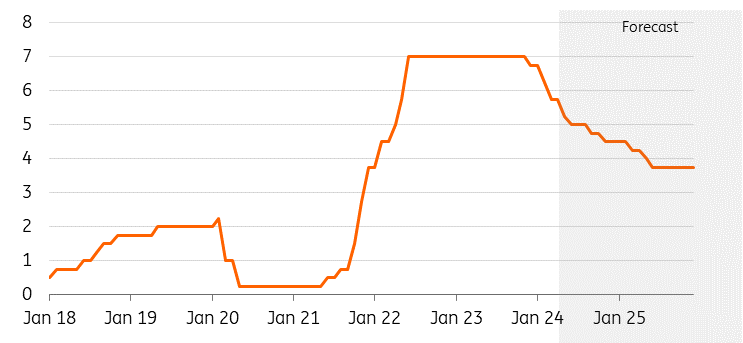

In sum, we have the broadly extinguished inflationary hotbeds of the past on the one hand and nascent future price pressures on the other. Consumer demand has entered a recovery phase, while investment remains underwhelming and industrial production languishes at 2018 levels. The CNB undoubtedly is a forward-looking institution, and safeguarding price stability is its sole mandate. With this in mind and the cyclical recovery set to carry on, although at a gradual pace, we think that some caution in reducing rates is the better option. Such an approach would also preserve some live ammunition to deal with potential difficulties ahead. A considerably narrowed field for reaction in case the world economy stumbles represents one of the drawbacks if interest rates are set low. We expect the policy rate to gradually decline to 4.50% at the end of this year and further to 3.75% at the end of next year as our base case scenario.

Monetary policy easing to take on a more gradual pace

Our market views

The financial markets have shifted by leaning towards a 50bp rate cut after signals from the CNB, which in turn has put pressure on the koruna. We believe EUR/CZK is only a fast money trade this year given the dynamics of the CNB cutting cycle and the markets' preference to bet on a faster pace of rate cuts. In our view, the market has thus moved from heavy short positioning in April, when EUR/CZK was around 25.300, to light long positioning in June, when EUR/CZK posted local lows at 24.550, well above the CNB forecast. However, the CNB board's openness to a 50bp rate cut at the June meeting visibly surprised markets and the shift in market pricing took EUR/CZK almost to 25.000, nearly erasing the entire gap in the CNB forecast. We expect EUR/CZK to be around 25.00 on the day of the meeting, which is likely to be the main argument for 25bp. On the other hand, it is hard to read the CNB's reaction function these days and perhaps the current levels could prove comfortable for the central bank. Even though pricing is quite aggressive, we see the EUR/CZK reaction function rather symmetrical in the event of a 25bp or 50bp decision for the 25.200-24.800 range. However, in both cases, we think we should see the weakest local CZK levels regardless of the decision and thus weaker levels may be attractive to long investors given that we only expect a stronger CZK from this point onwards due to the slowing pace of CNB rate cuts and strengthening economic fundamentals.

In the rates space, markets have moved more towards a 50bp decision, however falling PRIBOR has made it difficult to read the exact pricing in recent days. Nevertheless, roughly 100bp of rate cutting is priced in by year-end, which is only 25bp more than our baseline and still a very likely scenario. So we don't see much opportunity in the rates market for the decision itself here given the close call for Thursday. On the other hand, if the CNB delivers 50bp, the market would likely overreact and price in more easing, which we see as difficult to deliver in current conditions. We thus see paying dips rather than receiving spikes at the moment in the CZK market, with the CZK curve probably the best priced in the CEE region at the moment.

In the CZGBs space, the fundamental story remains positive. Monthly issuance remains lower while the budget is under control and we do not expect much change here. The summer months may bring slightly lower supply but that is all. Friday should see a funding strategy update from the Ministry of Finance, which should confirm our positive view. Thus, we see value in CZGBs with yields above 4%, but visibly the potential has thinned, which is compounded by the heavy long positioning of the market. On the other hand, we retain a tightening bias in ASW, which still has some potential in our view.

Frantisek Taborsky

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article