CNB has spent EUR7bn since May in defending the koruna

- 30 June 2022

- Czech Republic

According to our calculations, the CNB's FX interventions to support the koruna increased in June compared to May. We expect more will be required. We estimate that without interventions, EUR/CZK would be trading at around 25.20. A new governor takes over the CNB leadership from tomorrow, but we do not expect any changes in the approach to intervention

How much have CNB spent so far in FX intervention?

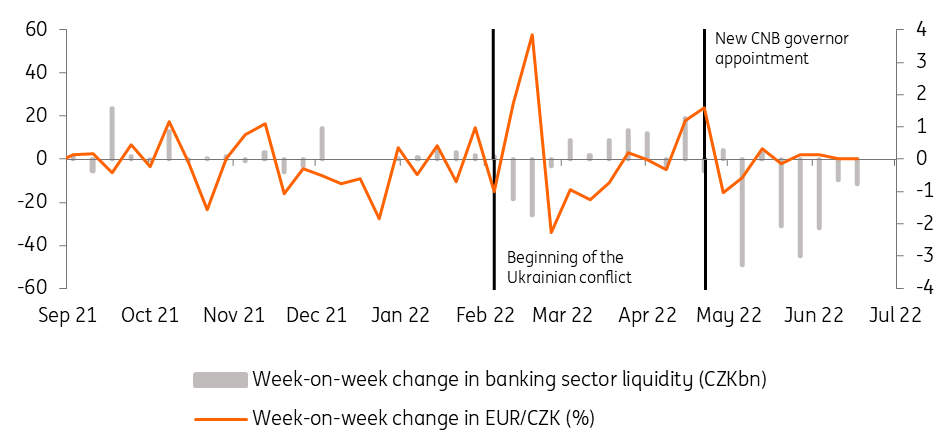

Another month of the koruna under the Czech National Bank's (CNB's) close management is coming to an end and it is once again time to look at how active the central bank has been in supporting the koruna. Official FX reserve data for May should be released later next week and we will have to wait another month for the June numbers. Until then, we will have to make do with an estimate based on banking sector liquidity data.

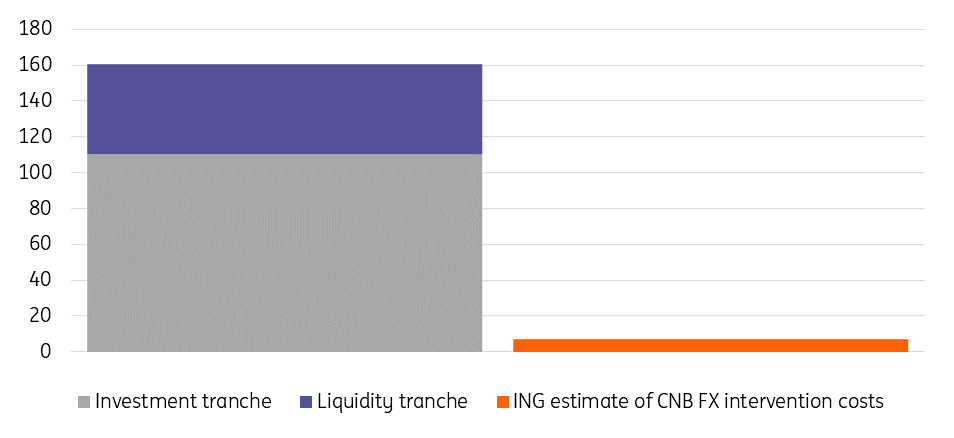

As mentioned earlier, based on our calculations, we estimate that the CNB's FX interventions in May were worth under EUR3bn. In June, it sold another roughly EUR4bn, giving a total of almost EUR7bn in FX reserves sales. This is equivalent to a collapse of 4.5% of all FX reserves or 2.8% of GDP. By comparison, official CNB data show that the central bank's FX operations in January-April ranged from EUR122-199m, which includes the FX reserve income sales programme and FX interventions following the start of the Ukraine conflict. Unfortunately, the liquidity data contains a lot of noise, which is the case, especially in late February/March when the collapse of a Russian bank branch hit this data series.

CNB managed to stabilise the koruna

Where would EUR/CZK be trading without CNB intervention?

The million-dollar question indeed. To find the answer we adjusted our short-term market equilibrium model based on interest rate differentials (2y CZK IRS vs EUR), market sentiment (DAX) and FX risk aversion (DXY). We normally use a rolling regression, but for this purpose we used the period from the start of the Ukraine conflict to the appointment of the new CNB governor, when we believe the CZK was in a new environment but still without significant CNB presence in the market (R2 = 0.84).

Using this relationship, we now estimate that EUR/CZK would be trading around 25.20 - the koruna roughly 1.8% weaker than current levels. On the other hand, we believe that this fair value of EUR/CZK may be a little lower in the last two weeks (e.g. 24.90/25.00) given that the relationship between the koruna and the interest rate differential has been restored, while our calculations also imply lower CNB intervention volumes – perhaps making current koruna pricing a little more market-driven.

The new governor takes over the CNB tomorrow

A new governor and board members will take over the CNB's leadership from 1 July. For now, we do not know much about the new board's views on interest rate developments and FX intervention. So, the most frequent question from clients these days is when we will hear more from the new board members? Usually, new members have a media quarantine of about one to two months at the beginning, but this time it could be shorter. Two of the three new members will be starting their second term on the board, so they know how things work. Therefore, we could see the first statements and interviews before the first monetary policy meeting in early August.

However, our conclusion from the statements so far is that the approach to FX intervention will not change and on the contrary could be more open. Let us not forget that the current board has been against the use of massive FX reserves for years and their view only changed in March this year. So, we expect FX intervention to continue in July under the same rules. The August CNB meeting should reveal the views of the new board. However, regardless of its assessment, we believe that the continuation of FX intervention is inevitable if the CNB is serious about inflation targeting. The interest rate differential, the main driver of the koruna, has basically reached its peak and, on the contrary, the CNB's dovish rhetoric and ECB rate hikes will drive it lower. The koruna thus has little reason to strengthen and, on the contrary, in our view, weakening pressure will intensify.

Size of CNB FX reserves in April and costs of interventions for May and June (EURbn)

Conclusion

The market has not yet properly tested the central bank's determination, but the data suggests that the CNB is being dragged into an increasingly heavy intervention battle to stop the koruna from depreciating and from easing monetary conditions too early in the cycle. The situation will get more complicated in the second half of the year and although the CNB has some of the largest FX reserves relative to GDP in the world, the nominal volume is not that large and very quickly the size of necessary intervention may become prohibitive.

However, this looks more of an issue for the fourth quarter. Until then, we expect nothing to change about the current situation and testing the central bank's resolve will not give investors enough reward for the expensive cost in shorting the koruna. But certainly, FX tools will remain the main focus for the second half of the year given the continued inflationary pressures in the Czech Republic and the CNB's reluctance to raise rates at all or sufficiently.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more