China stimulus optimism supports iron ore prices

Iron ore has been the best-performing industrial metal this year, with prices rising more than 17% year-to-date to November. We believe prices will be supported looking into 2024 amid optimism around China’s recovery and further support for the country’s property sector

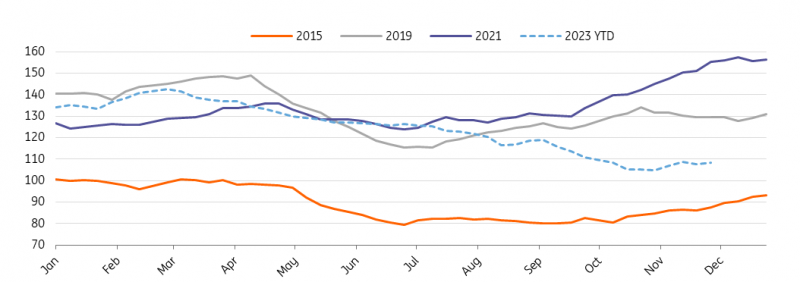

Iron ore holds above $100/t in 2023

Iron ore prices have managed to stay above the key $100/t mark for most of the year. Prices are now trading at their year-to-date highs, fuelled by strong demand and multi-year low inventory levels in China.

Over the last couple of months, the Chinese government has moved forward with a series of stimulus measures to turn around its ailing economy, which have supported iron ore prices. However, there are still concerns when it comes to China’s economy, particularly surrounding anything related to the property sector, which accounts for about 40% of demand for iron ore. The country’s property new home starts – the biggest steel demand driver – fell sharply in 2023, now down more than 23% year-to-date. This should continue to suppress steel demand in 2024.

In its latest efforts to revive the struggling steel-intensive property sector, China plans to provide at least 1 trillion yuan of low-cost financing to the country’s urban village renovation and affordable housing programs. The latest plan comes after Beijing announced fiscal stimulus, including raising the budget deficit with the issuance of an additional 1 trillion yuan of sovereign bonds. This has added to the positive sentiment in the iron ore market. With China ramping up investment in infrastructure and manufacturing, it should boost demand for steel in these sectors in 2024, supporting iron ore prices looking forward.

However, the uneven pace of China’s economic recovery has capped the upside for iron ore prices. The country’s manufacturing PMI has remained in contraction for most of the year, underscoring the fragility of its economic recovery.

With the recovery path for China still bumpy, we believe iron ore will remain sensitive to Chinese policies. Prices are therefore likely to remain volatile, at least in the short term.

China iron ore imports remain elevated

China saw growth in global seaborne iron ore imports in 2023, with the country’s full-year imports on course to rise for the first time since 2020. While China's iron ore imports dropped 1.8% month over month to 99.4 million metric tonnes in October, marking a second successive monthly decline, imports for the first 10 months were 59 million tonnes higher year over year at 977 million tonnes.

At the same time, iron ore inventories at Chinese ports have reached an eight-year low as mills have been cautious about restocking amid property woes. China’s iron ore port inventory is a key indicator that reflects the supply and demand balance, as well as the safety net and imbalance between the iron ore supply and the steel mill demand. We believe low inventories should support iron ore’s price at elevated levels, with restocking before February’s Lunar New Year likely to boost prices in the first quarter.

China’s healthy appetite draws down stocks

(Million tonnes)

Strong steel exports support production

China’s steel production has been robust this year, supported by strong growth in the country's steel products exports. So far this year, they've reached over 75 million tonnes, up from over 67 million in the same period last year, according to the latest China Customs data.

Stable domestic demand amid government support for the infrastructure and manufacturing sectors has also kept steel production in the country at elevated levels, and the World Steel Association has forecasted the country's steel consumption to grow 2% in 2023.

In the January-September period of 2023, China’s crude steel production reached 795 million tonnes, up 1.7% from the same period last year, according to data from Worldsteel. In 2022, China’s output reached 1.018 billion tonnes. Still, we believe that the uncertainty around mandatory steel curbs will weigh on the outlook for steel production. After China’s steel output climbed to a record of more than 1 billion tonnes in 2020, the government responded by ordering production cuts in each of the next two years to cut back on emissions and match supply with demand.

The intensity and the timeline of production cuts this year are still unknown, but any steel output cut would add to bearish risks for the iron ore market. Given Beijing's concerns over economic growth, however, we expect production cuts to be less stringent this year – and that should cap the downside for iron ore prices.

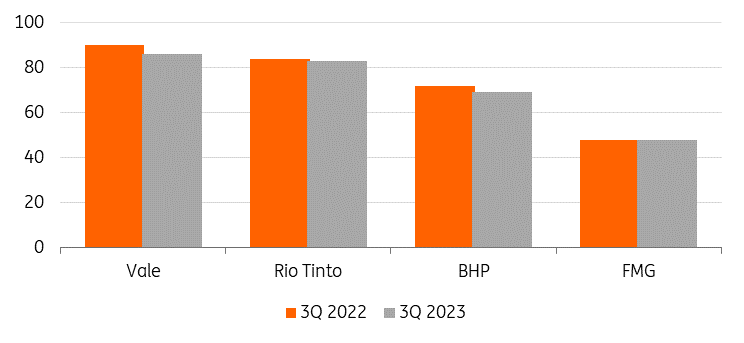

Supply from majors lags

Meanwhile, slow iron ore supply growth has dampened the impact of China’s slowdown. The market is very balanced in the supply and demand sides. Total iron ore production from the top four miners (Vale SA, Rio Tinto, BHP and Fortescue Metals Group) reached 287 million metric tons in the third quarter of 2023. This was 2% lower than a year earlier, as operational issues and maintenance impacted production across the board.

There are some concerns over iron ore supply in the near term. Brazilian exports will be constrained due to the suspension of operations at Tubarão. A slowdown in Australia’s shipments – after train drivers at BHP’s Pilbara iron ore hub in Western Australia announced a restrained strike from 24 November over pay and benefits – also poses a threat.

We believe that with the supply side largely stable, it will be demand in China continuing to drive iron ore prices going forward.

Iron ore supply from majors (million metric tonnes)

China policy key to iron ore prices

Iron ore prices are set to remain volatile as the market continues to respond to any policy change from Beijing. We expect them to average $120/t in 2024, assuming the government will introduce additional measures to support the economy, with iron ore remaining dependent on economic stimulus from China.

With demand largely stable, a further boost for China’s property sector will be crucial in supporting demand going forward. The downside risk for 2024 is if the stimulus effect is weaker than expected.

Beijing’s possible interventions to curb iron ore prices remain a downside risk for the market. Since the start of the year, the National Development and Reform Commission (NDRC) and other authorities have been enhancing the collaborative supervision and regulation of the iron ore market and have cracked down on price gouging, excessive speculation, and illegal activities. Previously, government interventions to calm the markets have included subduing trading and ordering steel capacity cuts. If we see similar measures used again, this could add further downside pressure to our view.

Looking further ahead, downside risks include China looking to replace older steel capacity with electric arc furnace capacity in order to help the country meet its decarbonisation goals. Growth in electric arc furnace (EAF) capacity at the expense of basic oxygen furnace (BOF) capacity will be a concern for the medium to long-term outlook for Chinese iron ore demand, reflecting increasing secondary production. Currently, 9.5% of China’s steel capacities are electric steel mills. The country plans to increase the share of steel from EAFs to 15% by 2025 amid a drive to reduce carbon emissions, increasing its appetite for ferrous scrap. China aims to achieve carbon neutrality by 2060.

ING forecast

Download

Download article

4 December 2023

Commodities Outlook 2024: Cautious optimism This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more