China signals more aggressive monetary stimulus

- 11 May 2020

China's credit growth slowed in April but the central bank, the People's Bank of China, has signalled more aggressive monetary stimulus. We expect there will be more focused credit injections to SMEs, which should help employment

Starting with slower credit growth in April

Combining all the data, we get the impression that corporates continued to issue bonds as an alternative to bank loans.

But the money raised seems to have been deposited in banks, which pushed up the M2 growth rate significantly, to 11.1%. Yuan deposit growth only rose 9.9%, and most of this increase came from corporate savings, which makes us curious about whether some funds raised in the bond market, in anticipation of projects beginning, have been parked in longer-term savings products, e.g. structured deposits, for interest income.

For individuals, we see a fall in household deposits and an increase in short term loans to individuals. This could reflect rising unemployment resulting from Covid-19.

Here is the data summary:

- Aggregate finance grew only CNY3.09 trillion in April after growing CNY5.15 trillion a month ago. Loan growth was a mere CNY1.7 trillion after CNY2.85 trillion in March.

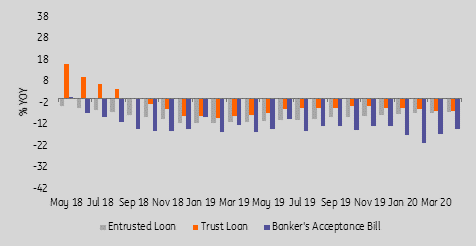

- Among other categories in aggregate finance, the net issuance of corporate bonds fell the least, at CNY902 billion in April similar to CNY982 billion in March.

- In contrast, government bond issuance, including local government special bond issuance, increased at a slower pace of CNY336 billion in April from an increase of CNY634 billion in March.

- Most shadow banking items increased at a slower pace in April even as the PBoC continued to ease.

- But the M2 growth rate surged to 11.1% year-on-year in April from 10.1% a month ago, compared to yuan deposit growth of 9.9% YoY in April.

China's shadow banking keeps shrinking even as the PBoC eases

...we see a fall in household deposits and an increase in short term loans to individuals. This could reflect rising unemployment resulting from Covid-19.

PBoC change to aggressive monetary easing

In its first-quarter report, the central bank deleted the prudency wording describing its monetary stance. This is a big change and means the PBoC is going to inject a lot of liquidity into the financial system.

The easing policy should focus on SMEs as they will be hit hardest by the Covid-19 crisis, and a possible coming trade war. They employ a lot of workers, mostly lower income groups.

We believe the easing will be in the form of targeted RRR cuts or broad-based RRR cuts for all banks.

- In previous RRR cuts, the central bank excluded big banks, which limited the injection of liquidity. From now on, this may change as more liquidity will be released if the RRR applies to all banks. This could help the economy recover from Covid-19.

- There should be an additional mechanism to encourage banks to lend to SMEs, which usually have weak credit profiles. Without this mechanism, mere RRR cuts will not help SMEs.

- A government-guaranteed SME programme could also be a solution as this will shift the credit burden from banks to the government, which is not desirable for lending to healthy corporates but is necessary to help SMEs and to stabilise employment so that households don't use up their savings or indeed need to borrow for a living.

After injecting liquidity from RRR cuts, there will also be interest rate cuts from the 7D reverse repo to the 1Y Medium Lending Facility and 1Y Loan Prime Rate. Money market rates should fall accordingly.

Forecast of monetary policies

We expect the RRR for big banks to be cut from 12.5% to 9.5% by the end of 2020. This is the most aggressive easing policy as it will inject a lot of liquidity into the system.

The 7D reverse repo rate should be cut from 2.2% to 1.5% and the LPR should be cut from 3.85% to 3.35%.

USD/CNY forecast

Though we expect a lot of liquidity injections from the PBoC, which could push down interest rates, we do not expect such moves to put depreciation pressure on the yuan. Instead, we are closely monitoring news on the trade and technology war, which are more likely to move the yuan in the coming months.

We forecast USD/CNY at 7.15 by the end of 2Q20 and 6.90 by the end of 2020. But we may revise the year end forecast if there is more negative news about US tariffs on China.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Covid-19: What you need to know

- This bundle contains 10 Articles