China RRR cut reduces risks from reform and trade war

- 25 June 2018

- China

A targeted cut in the reserve requirement ratio of 0.5 percentage point will add CNY700 billion of liquidity to facilitate debt-to-equity swaps and increase loans to SMEs. It's a policy that kills two birds with one stone, by relieving credit pressure from financial deleveraging reform and cushioning the potential impact of a trade war

Creative RRR cut to reduce two biggest risks in the economy

China has cut its reserve requirement reserve ratio (RRR) by 50 basis points, releasing CNY700billion cash. But this cash will be restricted to two purposes. State-owned and large banks will use CNY500billion for "debt-to-equity swaps" while other banks, including foreign lenders, will use the remaining CNY200billion to lend to SMEs.

We think this dual purpose RRR cut will reduce the two biggest risks facing the economy by:

- relieving corporate default pressure from financial deleveraging reform;

- providing a cushion for SMEs that could be affected by trade wars.

RRR cut for debt-to-equity swaps - another 'kill two birds with one stone'

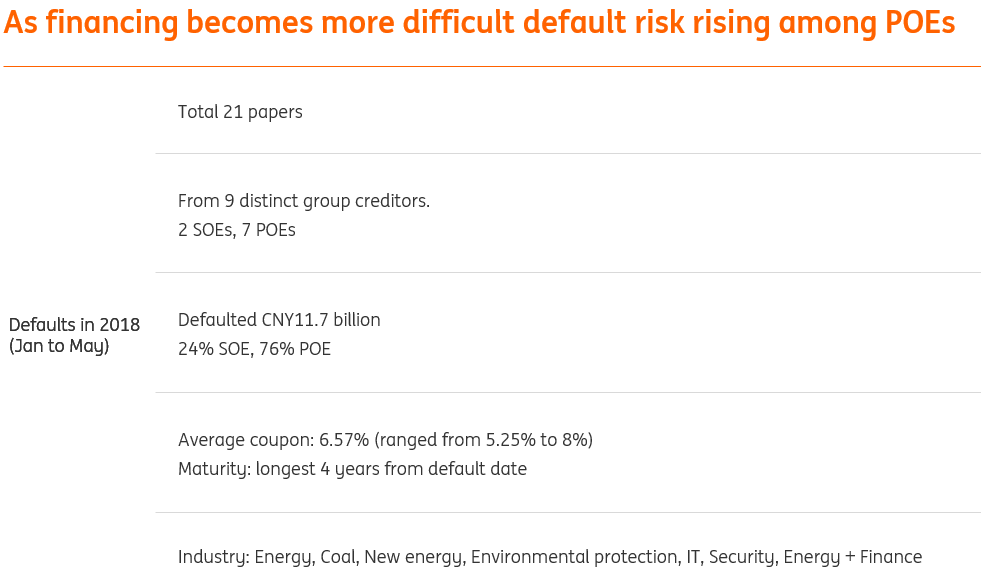

The RRR cut for debt-to-equity swaps should reduce the leverage ratios of corporates that participate, and therefore the number of default cases. These are rising in China due to financial deleveraging reform that started at the end of April when several policies were announced.

This RRR cut is likely to calm the market's concerns about deteriorating credit quality of companies affected by financial deleveraging reform. Still, we do not expect an immediate fall in credit costs in the debt market. The market is likely to adopt a 'wait-and-see' approach because the debt-to-equity swaps need time to have an impact on the credit market.

Debt-to-equity swaps in China - a primer

"Debt-to-equity swaps" in China have been developing quietly.

The current structure is that the main bank of an overleveraged company would create a subsidiary to hold the equity by reducing debt for the company (debt-to-equity swap). The subsidiary is usually in the form of a trust company or an asset management company.

The main bank would then include other investors to become equity holders of the subsidiary so that the main bank wouldn't be the only investor of the equity. Other investors could be, but are not limited to, the social security fund and state-owned asset management companies.

The swap ratio should be determined by the market, in theory. But since the number of cases of debt-to-equity swap is small, the "market price" of the swap rate is usually done by negotiations between the overleveraged company and the equity investors.

Banks need to provide extra capital for these equity holdings though they benefit from the reduction of non-performing loans or potential losses from the debt-to-equity swap.

There is a policy to restrict zombie companies (that is companies that are so highly leveraged and are targets of overcapacity cuts) to enter into a debt-to-equity swap. The purpose is to transfer risk from zombie companies to banks.

RRR cut for SMEs will allow more loans to survive the trade war

Another element of the RRR cut targets SMEs. The purpose is the same as the April RRR cut. As the trade war escalates, we expect that there will be increasing support from the government in terms of fiscal spending like tax cuts, and monetary support of targeted RRR cuts.

Together with the April RRR cut, cash released for SME loans should increase by CNY600 billion in six months' time.

But this may not be enough to cushion an escalating trade and investment war between China and the US, as well as a global trade war that disrupts the global supply chain, in which China's SMEs would be affected. Thus we expect more RRR cuts to come in 2018.

For the same reason, we do not expect the RRR cut to have a substantial impact on the USDCNY exchange rate.

We expect the next RRR cut in October but no interest rate hike

Similar to the RRR cut in April and July (this one is effective on 5 July), we expect the next RRR cut to be in October.

We believe that the timing won't coincide with the quarter-end because the central bank would like to send a signal to the market that the RRR cut is a long-term monetary policy tool, and should not be used to ease liquidity tensions at quarter-end.

We expect the next RRR cut would be 0.5 percentage point, similar to July's cut, but not 1.0 percentage point as in April.

The 1.0 percentage point cut of RRR in April applied to some banks only, and the overall cash released was CNY400billion, which benefited SMEs. The impact is smaller than July's 0.5 percentage point cut in RRR, which is applied to all banks.

As financial deleveraging reform continues, we expect the next RRR cut to be similar to the structure of July's RRR, applying to all banks but targeting different purposes to reduce the biggest risks in the economy, specifically risks arising from financial deleveraging reform and the escalating trade war.

We no longer expect the PBoC to follow the Federal Reserve's rate hikes for the rest of 2018. Interest rates in China have been high due to rising credit risks. The central bank may not want another push higher by following the Fed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 26 June 2018

- This bundle contains 7 Articles