China’s growth remains steady despite the tariff dance

- 12 June 2025

- China

China’s April data slowed but outperformed expectations, while easing by the People's Bank of China and the 90-day truce along with an initial trade deal supports our forecast upgrade – despite lingering uncertainties

China’s data softened but remained resilient amid April’s tariff turmoil

The sharp escalation of tariffs in April led to a wave of forecast downgrades in China, as markets weighed the impact on growth. Reports of halted shipping containers and empty ports grabbed headlines. However, China’s data releases over the past month, our first real look at the aggregate impact of tariffs, showed a less dramatic slowdown than feared.

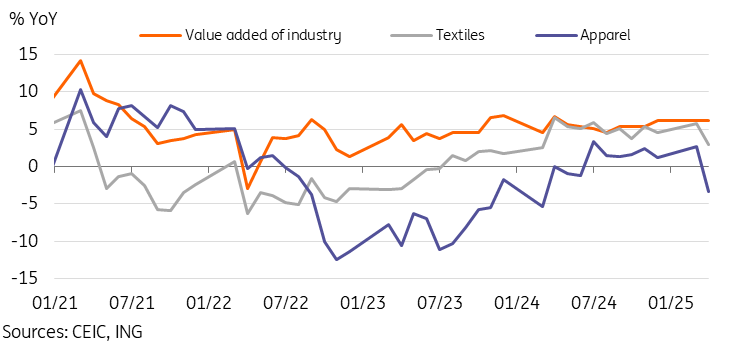

Exports and industrial production were the most closely watched indicators, and both moderated in April. We observed a more pronounced slowdown in low-value-added sectors, such as textiles and apparel, where readily available substitute products led to a sharper decline in China’s growth. This slowdown continued for exports in May, with exports to the US slumping by 34.5% YoY. However, the overall levels saw only a mild downturn as exports to other markets picked up part of the slack. We expect that the trade negotiation period could lead to another round of trade frontloading amid concern that tariffs could rise again.

Somewhat ironically, despite higher and faster-than-anticipated tariffs coming into effect, both export and industrial production grew faster in year-on-year terms through the first five and four months of 2025, respectively, compared to the 2024 growth levels. With that said, PMI data does present a case for caution, with May's data remaining in contraction for a second consecutive month, and though we saw a rebound of export orders, the gauge remained in contraction territory.

While the direct impact may have been smaller than feared, tariffs continue to contribute to overall uncertainty and weak sentiment, and we have therefore seen a slowdown in both fixed asset investment and retail sales.

Low value-added sectors hit harder by tariffs while overall growth remained solid

The PBoC seized the opportunity to ease policy as the yuan recovered

Markets have been looking for China's central bank to ease for some time, after various high-level meetings signalled easing to come at a “suitable time.” With the CNY stabilising after the 90-day trade war ceasefire, this window had finally arrived, allowing the PBoC to cut benchmark interest rates by 10bp and the required reserve ratio by 50bp, freeing approximately RMB 1tr of liquidity.

We still think there’s room for additional policy easing if needed later in the year, given deflationary pressures and the risk of moderating growth.

We are looking for another 20bp of rate cuts and 50bp of RRR cuts this year, though we suspect that the next move might not come until after the US Federal Reserve resumes rate cuts.

Initial trade deal boosts the outlook though Grand Bargain may remain elusive

After several stops and starts, China and the US reached an initial agreement to reduce trade tensions in London. Details remain sparse at the time of writing, but appear to include some loosening of restrictions around the edges, with the deal mainly featuring loosening of export controls on products such as rare earths from China and hi-tech exports from the US, as well as restrictions on Chinese students studying in the US. At the moment, it looks like tariffs will remain where they were at the start of the 90-day trade war ceasefire, meaning that this initial deal is a positive initial step.

While it certainly is encouraging that steps are being taken in the direction of negotiation rather than escalation, we can see that the 90-day trade war ceasefire is already showing that coming to any lasting “Grand Bargain” will be very challenging in such a short period. We expect that results may be limited to smaller or partial agreements where tariffs remain in place; as we said at the start of all the trade tensions, there certainly should be room for cooperation on issues such as fentanyl. If the current tariff levels remain in place, exports to the US should improve from the sharp declines seen in April and May, but should ultimately settle at a lower level, as easily substitutable products will likely lose out to other competitors.

It remains uncertain whether this 90-day deadline for reaching a trade deal still applies or if this agreement will be sufficient to keep tariffs at the current level. Reports are that no further talks are scheduled for now, but channels of communication remain open.

In the near term, we expect this current window of relatively lower tariffs to allow US importers to replenish inventories. Depending on whether or not the 90-day deadline still applies, we could see another round of import frontloading closer to August. Overall, developments in the past month have given a boost to China's second and third quarter outlooks. Along with the smaller-than-feared impact from April tariffs, we reverted our 2025 GDP forecast to the original 4.7% YoY level last month.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: A blockbuster plot worth following

- This bundle contains 14 Articles