China’s economy to endure another Covid New Year

- 4 February 2022

- China

China is reporting more confirmed Covid cases per day as its population prepares to celebrate the Chinese New Year. Localised social distancing measures are tight in Beijing, which will hurt catering businesses, but some consumption items will benefit. Infrastructure investment should pick up after the holiday

Another Chinese New Year with social distancing measures

Covid is still present in China, although the number of reported cases remains small, and China is still maintaining its zero-Covid policy. As a result, even with small numbers of reported Covid cases, localised areas in Beijing City have tightened social distancing measures and people flows. Some of those who intended to leave Beijing to travel to their hometowns are now stuck in the city. As well as Beijing, another Covid hotspot is Hangzhou, and travel agencies have cancelled cross-provincial travel in and out of the area.

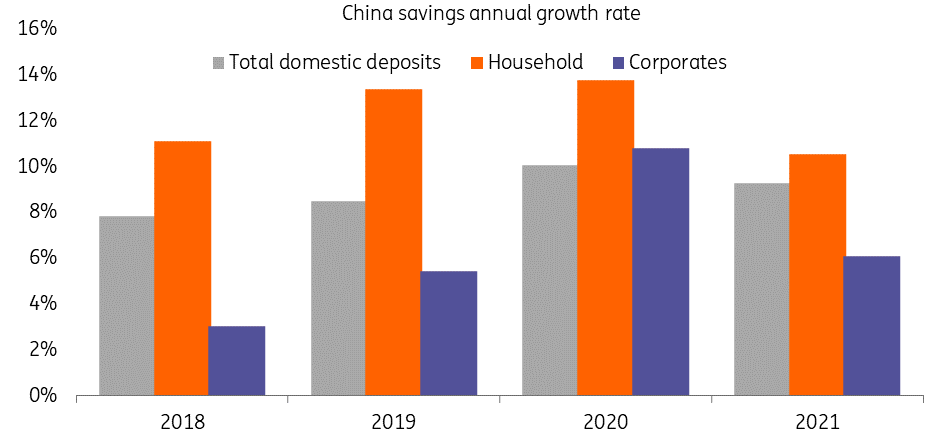

All these as well as future people flow restrictions will hurt catering and travel businesses. But for overall consumption, we still believe there will be some growth compared with the previous Chinese New Year as job stability has improved over the past few months. Household savings rose at a slower pace in 2021 compared to 2020 as the more recent social distancing measures have been more localised, and overall people flows have improved. This has helped the economy return to some sort of normality.

For this Chinese New Year, we expect that sales of clothes and beverages will benefit the most as we believe the government will continue to limit the degree of social distancing measures. But Beijing will experience a more stringent set of policy measures because the authorities want the Winter Olympics, which open on 4 February, to run smoothly.

Overall savings have been falling

Infrastructure investments vs real estate developments

We understand that the government is eager to minimise the economic and market impact of defaulting real estate developers. This will be done by organising mergers and acquisitions at a deep discount. Buyers will likely be developers and asset management companies with state backgrounds. We also expect that the other real estate developers will build more slowly than they have in the past to avoid piling up extra debt.

With these factors in mind, some building materials could be affected as demand from real estate developers will slow. But infrastructure investment should pick up some of the slack after the Chinese New Year as the central government is urging local governments to front-load projects in the first half of the year. This policy should be addressed in the "Two Sessions" to be held on 4 and 5 March 2022.

Forecasts

We aren't yet revising our GDP forecasts. These currently stand at 4%Year-on-Year growth in the first quarter of this year, and 5.4% for the whole of 2022. This is partly because the People's Bank of China (PBoC) has confirmed that it will deliver a more accommodative monetary policy in 2022. We expect to see more rate cuts in the 7D reverse repo, 1Y Medium Lending Facility, 1Y and 5Y Loan Prime Rates. As an indicator, we forecast the 7D reverse repo rate to fall from 2.2% at the beginning of the year to 1.7% by the end of the year. This forecast, however, relies on Covid cases remaining limited and confined to small area outbreaks, so the risks are skewed to the downside.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles