China curbs exports of battery-making graphite as global tech war escalates

China has imposed export controls on graphite, a key material used in electric vehicle batteries, in the latest move to control the supply of critical raw materials

Citing national security concerns, Beijing said on Friday it will require special export permits for certain types of graphite starting 1 December. It clarified that it was not targeting any particular country.

Under the new restrictions, China will require exporters to apply for permits to ship two types of graphite, including high purity, high-hardness and high intensity synthetic graphite material, and natural flake graphite and its products. Meanwhile, it dropped temporary controls on five less sensitive graphite items used in basic industries such as steel, metallurgy, and chemicals.

China dominates global supply chains of graphite, the raw material essential for EV batteries. Graphite demand is expected to rise by 20-25 times in the 2020-40 period, according to the International Energy Agency (IEA).

The EU listed natural graphite as a critical raw material in 2020. The US also considers it to be a critical and strategic mineral.

Beijing’s move comes days after Washington tightened controls on exports of semiconductors to China, including stopping sales of more advanced artificial intelligence chips made by Nvidia.

The EV supply chain has become a source of escalating feud between Beijing and the West. Last month, the European Union said it was weighing levying tariffs on Chinese-made EVs, arguing they unfairly benefit from subsidies.

China dominates global supply chain of critical minerals needed to make EV batteries, from material processing to the construction of cell and battery components. This is a result of Beijing’s early push towards electrification, particularly through subsidising EVs.

The curbs are similar to those placed in August on gallium and germanium, key metals used to make semiconductors and electronics.

Exports of the two metals had surged before the controls went into effect but have fallen in recent months. Meanwhile, prices outside China have increased.

China dominates graphite supply chains

China is the world’s top producer and exporter of the mineral. It also refines over 90% of the world’s graphite into the anode material used in EV batteries. Top buyers of graphite from China include the US, South Korea, Japan, Poland and India, Chinese Customs data shows.

Graphite can be found naturally or produced synthetically. Natural graphite is the mined graphite, which is then processed into an end-use product that can be used in the battery industry. Natural graphite is primarily mined in China and Mozambique. Synthetic graphite is produced by utilising a carbon precursor product, typically petroleum coke, needle coke or coal tar pitch, and made into graphite through a process called graphitisation.

A natural graphite anode generally benefits from smaller costs and lower energy consumption than a synthetic anode. But synthetic graphite is popular thanks to its higher purity and most lithium-ion batteries rely on it these days.

Other countries that mine graphite include Brazil, Mozambique, Russia, Madagascar, Ukraine, Norway, North Korea, Canada, and India.

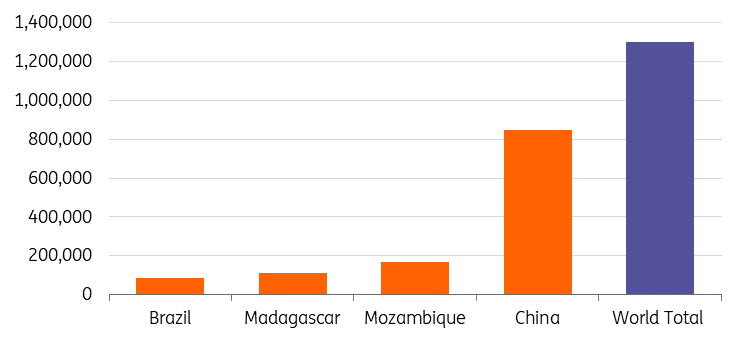

In 2022, China took the top spot by mining 850,000 tonnes of the mineral, accounting for 65% of the global total. Brazil came a very distant second with 87,000 tonnes while other countries mined significantly less, according to the US Geological Survey (USGS).

Africa has been a recent focus for graphite exploration, with projects under development in Madagascar, Mozambique, Namibia, and Tanzania.

Ukraine and Russia were among the top 10 producers of graphite before the conflict, according to USGS. In February last year, Ukraine halted graphite production. Operations resumed in August, however future production is uncertain as the conflict continues. As well, many countries have suspended trade relations with Russia, which has removed supplies of Russian graphite from much of the global market.

World mine production 2022 (tonnes)

Graphite is essential for EV batteries

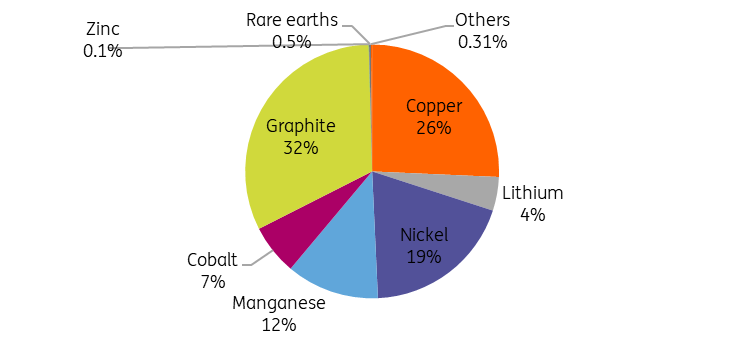

Graphite is the largest component by volume in an EV battery. It makes up 95-99% of the anode (negative electrode) material in lithium-ion batteries, in varying natural and synthetic combinations. In lithium-ion batteries, graphite cannot be substituted as it helps improve electrical conductivity and acts as a host for lithium ions. Cathode, the other half of the battery, constitutes lithium, nickel and cobalt.

Minerals used in electric cars

Prices to rise but supply chains will diversify

Graphite prices are likely to rise, but China’s latest move will also intensify the need to find alternative sources of this key battery material and push production out of China.

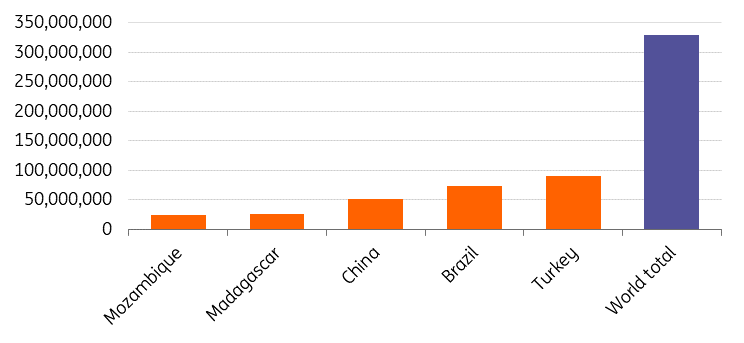

Although China produces more than half of the global supply, but looking at global reserves, China is not the only option. Turkey takes the top spot (27%), followed by Brazil (22%), with the two countries owning half of the world’s natural graphite resources. China comes third at 16%, according to data from the USGS.

World graphite reserves 2022 (tonnes)

Some EV manufacturers have already moved to diversifying supply chains away from China. Earlier this year, Tesla signed a supply deal with Australia’s Magnis Energy Technologies, which produces graphite concentrate in Tanzania.

Meanwhile, graphite consumption is expected to continue to increase, owing largely to growth from the EV market. A total of 14% of all new cars sold were electric in 2022, up from around 9% in 2021 and less than 5% in 2020. Global sales exceeded 10 million last year alone – and this level of growth isn't expected to slow any time soon, with almost one in five new cars sold worldwide this year set to be electric.

The battery end-use market for graphite has grown by 250% globally since 2018, according to USGS. Besides EVs, graphite is commonly used in the semiconductor, aerospace, chemical and steel industries.

Energy transition at risk on rising resource nationalism

The energy transition has become a pillar of policy for many governments while global trade and political tensions have prompted a reconsideration of global supply lines.

The global incidence of export restrictions on critical raw materials has increased more than five-fold in the last decade. In recent years, about 10% of the global value of exports of critical raw materials faced at least one export restriction measure, according to a report by the Organisation for Economic Cooperation and Development (OECD).

China’s graphite export restrictions are just a part of the global trend with several other countries having taken greater control of their resources. Chile nationalised its lithium industry earlier this year, while Indonesia banned exports of nickel ore in 2020.

We believe the rise in resource nationalism could slow down the pace and increase the cost of the energy transition, impacting the scale of investments, supply and prices. Meanwhile, policy and politics will continue to play an increasingly large role in the future of EV supply chains.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more