China: The supply chain is still broken

- 6 March 2020

- China

The spread of the coronavirus in China seems to be slowing down, but the global supply chain remains broken. As a result, we've revised our growth forecast to 4.4% YoY in 1Q20 and 5.2% for this year

What we know so far

The market expects Chinese activity data from January to February to be fairly disappointing.

China has postponed trade data release for January, so the upcoming data release will be year-to-date February figures, but that won't help much. For most of January and February, exports and imports are likely to be almost negligible.

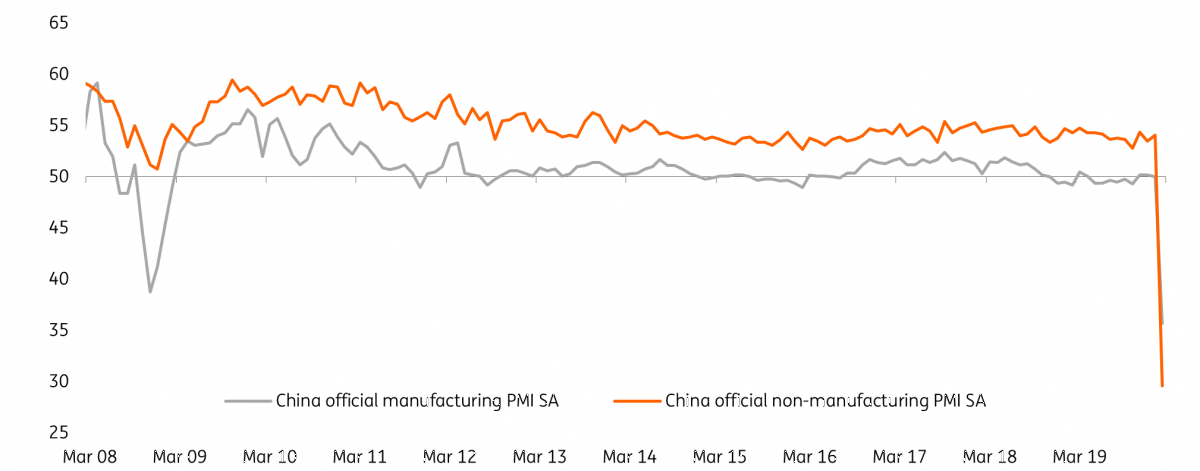

There wasn't much activity in the manufacturing and retail sector, which was reflected by the PMI. Manufacturing PMI dived to 35.8 and non-manufacturing PMI dived even deeper to 29.6 - both were the poorest reading since the data has been compiled.

We expect industrial production and retail sales to move to the negative territory but fixed-asset investment could experience some growth as two new hospitals have been built to combat coronavirus.

China’s worst PMI in history

Factories trying to get back to normalcy

Some reports suggest, 85.6% of larger factories resumed operation as of 25 February, but others suggest this figure might be overestimated.

As local governments received resumption quotas from the central government, they are eager to show factories in their cities are operating as usual again.

Therefore officials are closely monitoring the reopening of factories. Although well-intentioned, as officials could in theory help workers travel to factory locations from their hometowns, but, in reality, there is little they can do. The main issue is traffic, which has been very congested as many workers move from rural to factory hubs.

As a result, some factories, which are trying to circumvent officials’ visit, have switched on machinery, despite the lack of workers to inflate electricity usage, which often is a production indicator.

Not much will change in March

A few things we need to note on the development of the coronavirus for March:

- Imported coronavirus cases increase, but the number is still below 100 as of 4 March 2020.

- Some patients after being discharged from the hospital have tested positive again.

This means the peak of confirmed cases might not be behind us. As more countries report new cases daily, factories in these locations could also temporarily halt production, and this can always lead to the entire supply chain being disrupted.

With expected hurdles in factory production in March, and most consumers too wary to go shopping malls and dine out, and little business investment demand, the prospect of economic growth is still unclear.

We don't think March data will do any wonders.

More fiscal stimulus to the rescue

When activity levels are low, the Chinese government usually delivers a fiscal stimulus to support the economy. There is already a policy in place that waives social security contribution for staff, worth around CNY 1 trillion. More fiscal stimulus is likely to follow if cities confirm they have been able to reduce confirmed Covid-19 cases.

Last month, the Chinese government announced more stimulus measures. Therefore, we revise our projection of fiscal stimulus from around CNY 3.5 trillion to CNY 4 trillion, which is equivalent to 4% of nominal GDP in 2020, and this could be increased if more is required to boost economic growth.

Monetary easing beyond rate cut

We maintain our forecast that the People's Bank of China is going to cut 10 bps on 7D reverse repo, 1-year medium lending facility and 1-year loan prime rate. The loan prime rate cut should be on 20 March.

There will also be a focused RRR cut of 0.5 percentage points for banks to channel liquidity to companies affected by Covid-19.

More than these, the central bank is allowing companies suffering from cash flow problems to request deferred loan repayments. The positive side is that affected companies can concentrate on the resumption of work and not worry about repayment. The negative side is that only banks that have capital buffers can participate in this scheme.

The global supply chain remains broken

As most economic activities have been muted in January and February, we're not expecting a V-shape rebound in March, even though more fiscal stimulus and monetary easing is on the way.

Therefore, we scale down our forecast for China’s GDP in 1Q20 from 5.0%YoY to 4.4%YoY and 5.2% from 5.4% for the full-year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 9 March 2020

- This bundle contains 7 Articles