Cherish the moment as ECB Christmas comes early

- 11 December 2017

The ECB has said and done everything it wanted to do this year, so expect a lot of self-congratulation this week. But don’t be overwhelmed by the Christmas harmony, 2018 is likely to bring new in-house tensions

This week’s ECB meeting, as well as the subsequent press conference, should be short. The ECB has said and done everything it wanted to do this year: gradually introducing a dovish tapering. Therefore, Thursday's meeting, in our view will probably bring lots of looking back and self-congratulation. But don’t be overwhelmed by the Christmas harmony, 2018 is likely to bring new ECB in-house tensions.

The most interesting bit of the ECB meeting on Thursday will probably be the presentation of the latest ECB staff projections

For the ECB, the year 2017 will come to a close already this week. Thursday’s meeting will end another exciting year for the ECB. This was a year in which the Eurozone economy finally gained strong momentum, proving the ECB and its ultra-loose monetary policy right. But it has also been a year in which the ECB temporarily lost its magic touch on financial markets – it got it back eventually by successfully preparing the grounds for a dovish tapering, with a reduction of QE without distorting financial markets.

Thursday's meeting, in our view, will bring lots of self-congratulation by ECB president Mario Draghi, emphasising the strong growth story. At the same time, we expect Draghi to reconfirm the main messages from the October meeting - that policy rates will remain at current levels “well past” the horizon of the net asset purchases, that QE could continue beyond September 2018 if a “sustained adjustment in the path of inflation consistent with its inflation aim” is not achieved, and that the ECB could still do more QE if the macro outlook “becomes less favourable” or financial conditions “become inconsistent with further progress towards a sustained adjustment in the path of inflation”.

The most interesting bit of the ECB meeting will probably be the presentation of the latest ECB staff projections. With some upward revision for Eurozone growth for this year and next, the ECB should join the growing choir of Eurozone optimists. Even more important for the future path of monetary policy, however, will be the ECB’s inflation forecasts for 2019 and 2020.

The long-term inflation projections will be important in a possibly upcoming policy debate in 2018. With higher oil prices, chances that headline inflation could push through the 2% level next year have increased. This has provided ammunition for ECB hawks to push for a definite end to QE earlier rather than later than September 2018. It could also be the trigger to restart the currently hushed debate on sequencing and forward guidance.

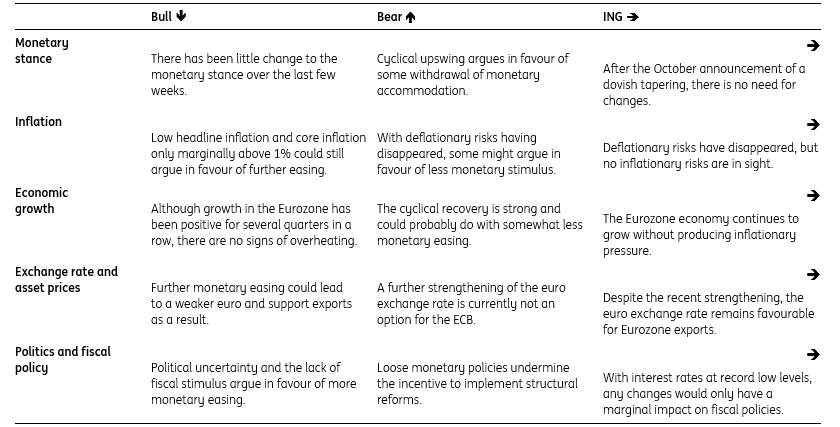

One of the ECB’s big successes in 2017 has been that it managed to tame many diverging views and statements within the Governing Council towards what we see as the right path towards tapering. It should cherish the moment because it is far from certain that this discipline will continue in the next year.

ECB Bull Bear

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more