Changing trade flows for coking coal

- 8 June 2022

- Commodities, Food & Agri

Coking coal has had a volatile year so far. Russia’s invasion of Ukraine has led to supply concerns as buyers shun Russian coal. This comes at a time when Australian coking coal exports have suffered due to bad weather. However, prices should edge lower as supply prospects improve

Record prices due to supply tightness

Australian coking coal prices have traded to record levels this year. Prices broke above US$600/t at one stage in March, a period when there was plenty of uncertainty over Russian coal supply due to the war. Rainfall and floods in Australia also tightened up the supply side. The market has given back a lot of these gains as trade flows slowly adjust, and amid worries over Chinese demand and the expectation that Australian flows will recover as we head into the dry season. However, the market is still up more than 20% year-to-date.

Russian coal flows

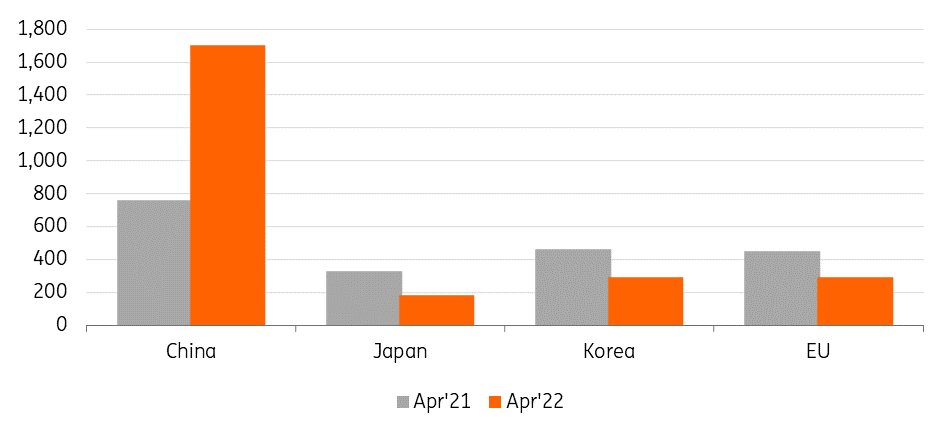

Russia is a fairly large exporter of coking coal, making up around 9% of global export volumes, leaving it in a tied third position with Canada among the largest exporters. Therefore the bans we have seen imposed by some countries, along with self-sanctioning, have had an impact on the market. This impact is already evident in Russian coal flows. EU imports of Russian coking coal in March (latest available data from Eurostat) have fallen by around 35% year-on-year, and given the EU ban on Russian coal, these volumes will only continue to trend lower. Japan and South Korea have also reduced volumes, with imports falling 45% and 38% YoY, respectively, in April. However, these reductions have been more than offset by China, which increased Russian coking coal imports in April by 124% YoY. We also suspect that India will look to pick up a larger share of discounted Russian coking coal, which would free up alternative supplies (Australian) for those buyers who are avoiding Russian coal. We have seen India taking similar action when it comes to oil imports.

Coking coal imports from Russia-k tonnes (Apr 22 vs. Apr 21)

Australian exports struggling at a time of need

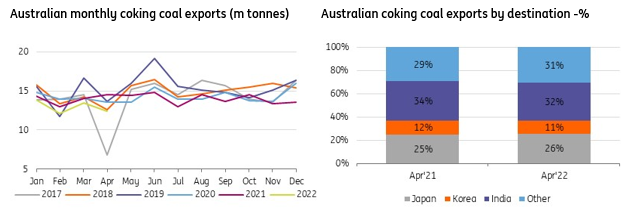

While the Russian sanctions have raised supply concerns, Australia has struggled to help the market out with stronger export flows. Instead, exports have been under pressure for much of the year due to heavy rainfall in both Queensland and New South Wales. And this follows weaker exports over 2021, with a little over 167mt shipped last year- the weakest volumes since 2012. The latest data from the Australian Bureau of Statistics shows that exports over the first four months of the year totalled 51.8mt, down 7% YoY. This is the slowest pace of exports since 2017 when we saw cyclone Debbie. However, given that Australia is moving further into the dry season, we should see a recovery in coking coal exports. Demand for Australian coal should also be robust given that many buyers will be looking for alternatives to Russian supply.

Trade data is yet to reflect any significant changes in Australian trade flows. In April, 32% of Australian coking coal went to India, compared to 34% in April 2021. It may still be too soon to see India shifting to discounted Russian coal, or at least for it to be reflected in trade data. Also, given the wind-down period in Russian coal flows to the EU, it will likely take some time for this share to grow. There have been reports of increased interest from EU buyers for Australian coking coal.

Australian coking coal exports lagging

Chinese imports still struggling to get back to pre-2020 levels

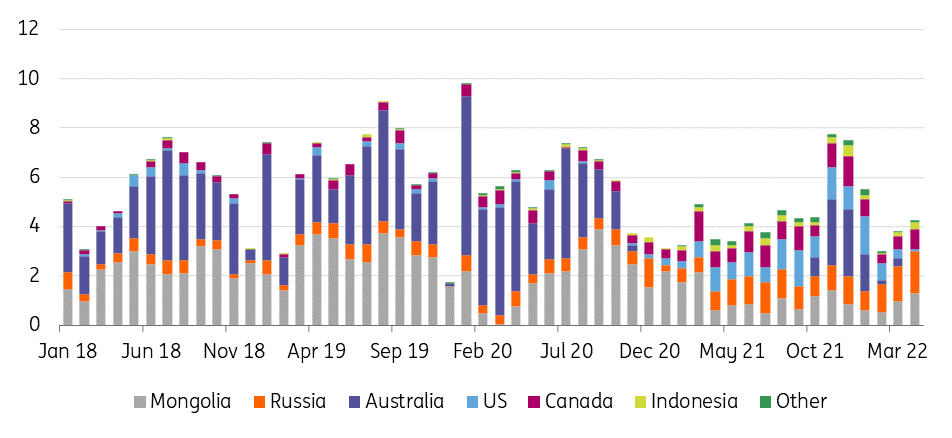

Since the unofficial ban on Australian coal, China's coking coal imports have struggled to reach pre-ban levels. This is despite China importing larger volumes from Russia in recent months. Given the prospect of several countries increasingly shunning Russian coal, we could very well see Russian volumes to China continue to grow. But up until now, clearly no other origin has been able to make up the shortfall from Australia. Reduced flows from Mongolia due to Covid-19 restrictions have also had an impact on overall imports. The only period that we saw Chinese coking coal imports go back towards pre-ban levels was when the government agreed to clear a lot of the stranded Australian coal cargoes at Chinese ports towards the end of last year and early this year.

China coking coal imports by origin (m tonnes)

Despite lower Chinese imports, the spread between Chinese domestic futures and Australian coking coal has narrowed from the US$200 plus levels seen in 2021. In fact, we have seen periods this year when Chinese domestic coking coal futures have traded at a discount to Australian coking coal.

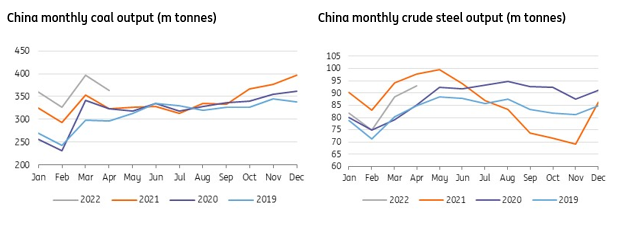

There are a number of reasons behind the weakening in the spread. In China, domestic coal output has ramped up given concerns over domestic energy supply. In addition, demand has been under pressure. Policy to cap steel output should weigh on demand. China aims to reduce steel output further this year after seeing a decline in output in 2021 for the first time since 2015. In addition, Covid-related restrictions this year have hit demand although the Covid impact should start to subside as restrictions are gradually eased. If China continues with its zero-Covid policy, however, this will remain a downside risk for demand.

These more bearish developments in the Chinese market have come at a time when Australian exports have been under pressure whilst there has been a fair amount of support due to bans and self-sanctioning of Russian coal.

China coal output surges, whilst steel output lags last year

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more