Central banks: Our main calls

We're now expecting the Fed Funds Rate to hit 5% early next year, albeit in more modest steps. We also think there are limits to how much further both the European Central Bank and Bank of England can hike rates amid a looming recession

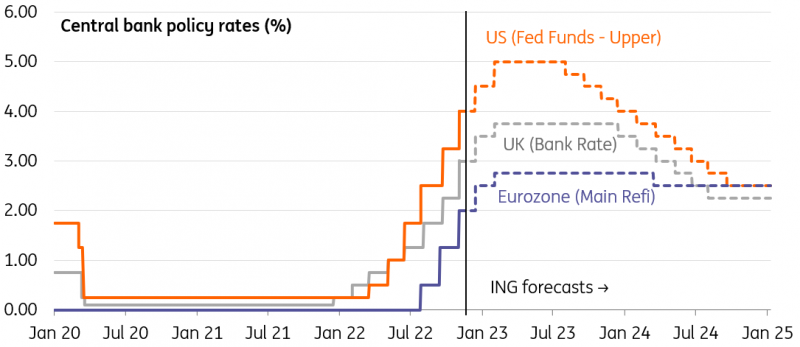

Central banks: Our forecasts

Federal Reserve

After four consecutive 75bp Federal Reserve interest rate increases officials have opened to door to a slower pace of hikes from December. The harder and faster a central bank moves into restrictive territory, the less control over the outcome and the greater chance of an adverse reaction. Given the state of the residential real estate market and the deteriorating corporate and consumer outlook, recession in the US now looks unavoidable. However, inflation is showing little sign of slowing. We need 0.1% or 0.2% month-on-month core inflation readings to get the annual rate down to 2% rather than the 0.5% or 0.6% MoM increases in ex-food and energy prices we are seeing. So, while the pace of hikes may slow, the expected terminal rate keeps moving higher. Nonetheless, with housing rents and used car prices now falling, and corporate pricing power being squeezed by the downturn, we think a 5% Fed Funds Rate will mark the peak in February and the door will open for rate cuts through the second half of 2023.

European Central Bank

The ECB’s October meeting had something for everyone. Another jumbo rate hike of 75bp and the opening for more for the hawks, but also more recession warnings and an opening to a dovish pivot in December for the doves. Consequently, the times of uncontested decisions at the ECB seem to be over. The December meeting will be much more controversial with a looming recession and a high chance that the ECB’s longer-term inflation forecasts will point to a sharp inflation retreat in 2024 and 2025. These aren't really the best arguments to hike into restrictive territory.

We expect the ECB to deliver rate hikes totalling 75bp at the December and February meetings. The balance sheet reduction has started with the announced changes to the ECB’s longer-term loans to banks and the option for earlier repayments. More will follow as a gradual phasing out of the reinvestments of asset purchases could become a substitute for additional rate hikes in 2023.

Bank of England

Markets have pared back interest rate expectations in light of a more stable fiscal backdrop but are still pricing Bank Rate to near 5% next year. Bank of England officials have begun to hint more explicitly that this would come with huge damage to the economy and is inconsistent with the amount of tightening needed to get inflation lower. Still, policymakers face an unpalatable decision. If they undershoot market rate expectations, the risk is that we see a renewed downside for the pound – not least because a full-blown pivot from the Federal Reserve seems at least a few months off. That helps explain why the BoE accelerated the pace of rate hikes in November.

But doing so repeatedly risks baking in mortgage rates and corporate borrowing costs which risk material stress in the economy. Around a third of mortgages are fixed for two years, while small and medium-sized enterprises (SMEs) are typically on floating interest rate products. We therefore expect the Bank to undershoot market expectations and remain unconvinced Bank Rate will go above 4% next year. We think the 75bp hike was a one-off.

People's Bank of China

The PBoC seems to have abandoned the traditional monetary policy tool of policy rate cuts and Reserve Requirement Ratio (RRR) cuts as a means to support the economy. Instead, the central bank has increased liquidity via policy banks in China. These policy banks lend directly to local governments for a specific policy target, for example, to finish unfinished home construction projects. This should be more time efficient as commercial banks would not be able to lend to property developers due to the still restrictive policies set for property developers, and they would be reluctant to lend to construction companies. This kind of direct lending to local government avoids them having to increase bond issuance, and therefore reduces interest costs of local governments in general. We expect the central bank to increase liquidity injections through policy banks until all unfinished residential projects are completed.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

4 November 2022

ING’s November Monthly: The long wait for the pivot This bundle contains 14 Articles