CEEMEA FX Outlook 2023: Geopolitical misfortune

- 16 November 2022

- FX

The geographic and geopolitical situation has made this a difficult period for the region. However, things should normalise in the coming year. We expect global pressures to ease and central banks to drop their FX intervention approach. Nevertheless, the situation remains fragile and we remain vigilant

Make the FX market normal again

Although it can be said globally that the last few months have been very complicated, the CEEMEA region and in particular the CEE4 have been clearly leading the way in this mess. The Covid years forced central banks in Central and Eastern Europe to start a global hiking cycle, and this year's events have compounded the burden on the region. In our view, the main shock is already over, but we are far from out of the woods and are only moving into the second stage – the aftermath.

In addition to the standard drivers of FX, such as rate differentials and EUR/USD, the price of natural gas has now become a central theme for the CEE4 region. The coming winter will test the unity of the European Union with a shallow recession and central bank efforts to end record hiking cycles bringing further pain to FX. Moreover, twin deficits, which will remain with us for a longer period, do not play in the region's favour. Central banks have been forced to do more than just hike rates to ensure price stability and the CEE4 region has split into two camps: full FX intervention regimes (Romania and the Czech Republic) and hybrid defence (Poland and Hungary). To make matters worse, politics has also come into play, and in particular, the dispute between Hungary and Poland with the EU has weighed heavily on the forint and the zloty. As you can see, the cards are heavily stacked against the CEE region, and we carry all these themes into the next year.

However, we believe that these issues will be addressed in 2023 and market conditions will begin to normalise. By far the biggest potential, in our view, is the Hungarian forint, which has suffered badly from the government's uncertain access to EU funds, full dependence on Russian energy, and the greatest sensitivity to a global sell-off. Therefore, with the calming of these issues, which we believe is only a matter of time, the hidden potential of the forint could be unlocked, outperforming its CEE peers. We see a similar story on a smaller scale in Poland. On the other hand, the Czech National Bank and National Bank of Romania have taken the path of keeping FX under control, leading to artificial overvaluation. In both cases, we expect a loosening of the central banks' approach in the first half of next year, which should lead to significant depreciation.

Among the high-yielders, Turkish policymakers have used an array of unorthodox policy measures to limit weakness in the Turkish lira. The Turkish election in June will be a pivotal period for financial markets, and investors will remain wary that unchecked inflation could put pressure on the lira. In South Africa, the rand looks to have found some good buyers near the 18.50 area in USD/ZAR. Those levels could be tested again early next year should the Federal Reserve push real interest rates higher again, but as pessimism in the Chinese economy starts to fade in the second half of 2023, (the rand is very much driven by commodity prices and China’s performance) USD/ZAR could be trading well below 17.00. Finally, USD/ILS normally proves a good bellwether for the broad dollar trend. And the Bank of Israel might be slightly more tolerant of shekel strength in 2023. We target 3.00 for USD/ILS.

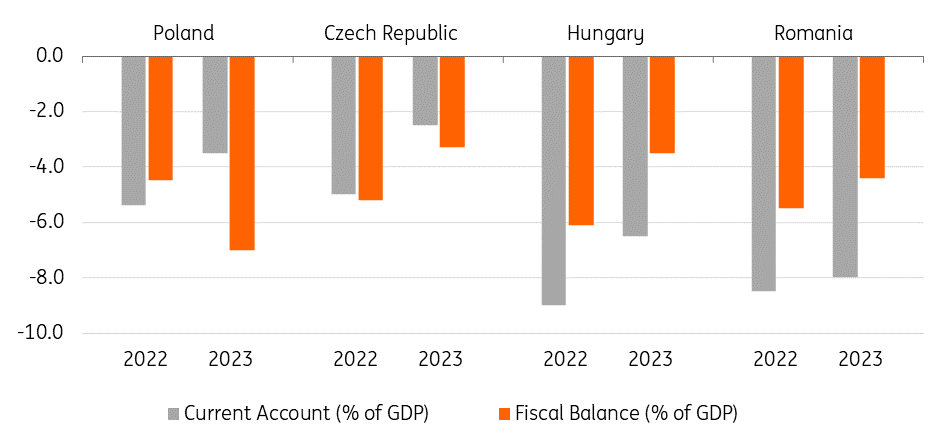

Twin deficits - the new standard in the region

EUR/PLN: Conditions to improve, zloty remains at risk

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| EUR/PLN | 4.70 | Neutral | 4.90 | 4.85 | 4.74 | 4.66 | 4.70 |

- Valuation: Our relative value EUR/PLN model (gauging the exchange rate against other market variables, such as swap spreads, option volatility, etc) continues to point to the zloty still being some 3% undervalued against the euro. We attribute this to a mix of risks, both external, particularly the war in Ukraine and its economic fallout, and internal, specifically, tensions with the EU, elevated CPI risk and expansionary fiscal policy undermining the local currency bond market – Polish government bonds (POLGBs). Many analysts suggest another major Russian offensive may be due in the spring. If Russia simultaneously attempts to put economic pressure on the EU, this could again sour sentiment towards the CEE region. The prospect of the conflict coming to an end is a major unknown, but investors should at least become increasingly resilient to news about the war.

- External position: Fundamental backing behind the zloty should improve next year, but risks behind the local policy mix will rise. We expect the current account deficit to tighten from €35bn to €26bn, owing to e.g. a more favourable terms of trade. Poland is also likely to draw some €20bn from the 'old' EU budget. Moreover, the government finally decided to lean towards hard currency funding. All of this is likely to be converted via the market under the current Ministry of Finance's FX strategy – balancing the current account deficit. Also, FDI inflows should remain solid, already standing at a net €16bn in the first half of 2022. Year-end 2022 may prove more difficult, as refilling natural gas reserves may again prove costly.

- Politics: Domestic politics is a major unknown in 2023. The proximity of the October elections is a key risk for the fiscal consolidation the government recently unveiled to curtail weak POLGBs. The government is also attempting to reset relations with the EU – possibly encouraged by Hungary’s pro-EU turn. While reaching an actual compromise will take time (and may prove impossible ahead of the general elections), it is at least a move in the right direction and likely to improve the market perception of Poland. Moreover, opinion polls show increasing support for the EU-orientated opposition. A victory for them could prove supportive to the zloty, as investors would bet on swift access to the 'new' EU budget.

EUR/HUF: Waiting for a forint breakout

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| EUR/HUF | 405.00 | Bearish | 400.00 | 390.00 | 380.00 | 385.00 | 390.00 |

- Inflation: The forint's (HUF) underperformance is largely related to price pressures. Despite the anti-inflationary measures provided by the Hungarian government via price caps in basic food, fuel, and utilities, core inflation is the highest in the EU. However, we believe that the peak is close. Real wage growth dropped into negative territory from September, consumer confidence is close to a record low and a higher share of companies are complaining about a lack of demand rather than a lack of labour. These factors should tame the pricing power of companies. Thus, we see headline and core inflation peaking around the end of 2022 or early 2023. As soon as inflation starts to ease, inflation expectations will come down, so a forward-looking positive real interest rate will spur interest in the HUF.

- Monetary policy: The central bank stepped into Phase 3 of its tightening cycle in mid-October with an emergency move. New temporary targeted measures were introduced to maintain financial stability alongside the main goal of price stability. The effective rate is now defined by the one-day deposit quick tender, sitting at 18%. With further fine-tuning in the system, we see monetary transmission improving, with short-end rates rising further. In parallel, tightening via the squeezing of liquidity will continue. The exit strategy from the 'whatever it takes' stance will be triggered by materially improved risk sentiment (see next bullet). We think this could translate into a gradual convergence of the effective rate to the base rate, starting as soon as late December.

- Internal risks: As this policy turnaround will be triggered by a materially improved risk environment, we see a potential relief rally in the forint, despite some normalisation in interest rates. The two key elements of internal risks are the Rule-of-Law procedure and the current account imbalance. Regarding the former, we expect Hungary to settle the dispute with the EU, opening the door for EU transfers as soon as mid-December. This will eliminate a key barrier to HUF strengthening. We expect the country’s external balance to improve in the coming months as the recession and coming winter will dampen the country’s import needs, easing the systemic pressure on the forint. In our view, this could result in a 5% strengthening of the forint over the next six months.

EUR/CZK: Koruna under CNB control

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| EUR/CZK | 24.30 | Neutral | 24.50 | 24.50 | 25.00 | 25.00 | 24.50 |

- Monetary policy: The Czech National Bank left interest rates unchanged at 7.0% for the third consecutive meeting and we think the Bank has now ended its hiking cycle – the first central bank in the region to do so. The economy already posted a decline in the third quarter of 2022 and we believe it is heading into a shallow recession. Wage growth remains high but inflation below the CNB's forecast suggests a hawkish surprise is unlikely, in our view. The current account has plunged into a record deficit and, in relative terms, we forecast it will reach the largest deficit since 2003. Moreover, fiscal policy shows only marginal signs of consolidation, and so the Czech Republic joins the twin deficit club within the CEEMEA region.

- FX Interventions: The main topic for the Czech koruna in the coming months is the fate of the CNB's FX intervention regime. According to the central bank's figures, it has so far spent 16% of FX reserves from mid-May to the end of September. In our view, the CNB's activity in the markets has been zero in recent weeks, as confirmed by the Bank's board member Oldrich Dedek in a recent interview. Therefore, we see the CNB in a comfortable position and expect FX intervention to continue at least until the end of the first quarter next year with a line in the sand at 24.60-24.70 EUR/CZK.

- What next? For now, the koruna is clearly capped on the upside due to the presence of the CNB in the market, while we also see the pressure on the CZK from the global environment as gradually easing. Moreover, within CEE, markets see more interesting themes in Poland and Hungary and several CZK short squeezes have discouraged bets against the end of CNB FX intervention. Therefore, we expect EUR/CZK to trade slightly below the CNB's unofficial line and the koruna will return to the market's attention in the second quarter of 2023 when we think the topic of the CNB's exit strategy will return.

EUR/RON: Focus on the 'managed' in managed float

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| EUR/RON | 4.91 | Mildly Bullish | 4.94 | 4.95 | 5.10 | 5.10 | 5.10 |

- Hiking cycle: Having reached a key rate of 6.75% in November, the National Bank of Romania is either at or very close to the end of the hiking cycle. We narrowly favour no more hikes in 2023, though we admit that chances are high for another 25bp increase in January. The NBR’s commitment to firm liquidity management will likely – on average – keep carry rates above the policy rate. However, we see a good chance for the liquidity situation to improve substantially into year-end on the back of accelerated spending by the Treasury. Mopping up this liquidity is likely to take a good couple of months.

- Twin deficits: While on the budget deficit side, policymakers seem committed to reaching the 3.00% of GDP target in 2024 (with a 4.4% target for 2023), developments on the current account side are not encouraging. Due to unfavourable price developments in external markets (including the energy sector) but also on the back of robust GDP growth in the first half of 2022, the trade balance deficit will close well within double digits in 2022, possibly flirting with levels last touched in 2008 when it surpassed 16.0% of GDP. This represents a significant structural weakness that will keep pressure on the leu and require constant FX intervention from the central bank. Strong EU funds absorption will be key to balancing this imbalanced picture.

- Politics: The relatively eventless political scene in 2022 has been rather remarkable after years of political turmoil. As per the current coalition agreement, the PNL prime minister will resign in May 2023 and a PSD prime minister should be voted in by the same coalition. While there are no real signs of trouble currently, the impending 2024 electoral year still makes it somewhat hard to picture a completely serene change of power in May-June 2023.

EUR/RSD: IMF acts as an anchor of stability

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| EUR/RSD | 117.30 | Neutral | 117.30 | 117.30 | 117.35 | 117.40 | 117.40 |

- IMF: On 2 November, the IMF announced that a EUR2.4 billion 24-month Stand-By Arrangement (SBA) will replace the current Policy Coordination Instrument (PCI), subject to IMF Board approval in December 2022. The agreement will help to address “emerging external and fiscal financing needs”. On the external front, the IMF estimates the current account deficit to reach 9.0% of GDP in both 2022 and 2023 due to “sharply higher energy import costs along with shortfalls in domestic electricity production, as well as weakening external demand”. On the fiscal side, the initial 3.0% of GDP budget deficit target will be exceeded, most likely ending up around 4.0% of GDP. Summing up, the country needs financing, and the current choppy markets have made the IMF SBA look more appealing despite the strings attached.

- Monetary policy: Beyond the proposed reforms on the fiscal side, the SBA will undoubtedly shape monetary policy as well. The 2 November press release specifically mentions that “the macroeconomic policy mix should be tight to contain high inflation and support exchange rate stability” and “the ongoing monetary tightening is crucial to ensure that inflation does not become entrenched”. Essentially, we read this as a signal that the IMF is relatively comfortable with the current FX stability policy but that interest rates should continue to be increased. We revise our terminal key rate forecast from 4.50% to 5.75%, which should be reached in the first quarter of 2023.

- (Geo)Politics: While on the internal front, the April 2022 elections have settled things for some time, the regional developments – be it the war in Ukraine or the Kosovo car plates dispute – are making it more and more difficult for the country to sustain the ambivalent stance it has so far maintained. Absent more clarity, Serbia’s progress as a candidate country for EU accession might see little improvement in the short to medium term, which could dent its efforts to achieve the long-awaited investment grade status.

USD/KZT: A defensive play on local fundamentals

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| USD/KZT | 460.00 | Mildly Bullish | 480.00 | 480.00 | 470.00 | 470.00 | 470.00 |

- Scope for higher exports: The Kazakh tenge (KZT) depreciated 6% in the first 10 months of 2022, which is defensive given the geopolitics in the region and the 10-15% US dollar appreciation against major currencies. This is attributable to Kazakhstan’s stronger trade. Exports grew 48% year-on-year in the first nine months of 2022, and the current account is back to a $7.9bn surplus vs. a $5.6bn deficit in the first nine months of 2021. Oil production of 1.5m barrels per day is below the OPEC+ quota of 1.6m bpd, and the official target of 1.9-2.0m bpd, meaning there is scope for an increase in exports in 2023, assuming stable oil prices. Meanwhile, oilfield maintenance and an 85% dependence on Russian pipeline infrastructure are downside risk factors.

- The government is looking to reduce involvement in the FX market: The government is planning fiscal consolidation to reduce the breakeven oil price from a high $110-140 in 2021-2022 to a more comfortable $55-76/bbl to 2023-25. As a result, more FX oil revenues could be saved, reducing the gross spending of the sovereign fund to $7bn in 2023 from $9-11bn in 2021-22. However, the planned 3% GDP increase in non-oil revenues appears ambitious, and the actual conversion of FX oil revenues into KZT for state spending could be higher than officially planned in the event of non-oil revenue under-collection and higher than expected spending.

- Private capital flows remain uncertain: While the state capital flows, including the sovereign fund and foreign debt, are normally a mirror image of the current account, the private sector’s capital flows are subject to uncertainty. In the first nine months of 2022, private outflows (including unidentified operations) narrowed to $0.3bn vs. $3.8bn in 2021, in line with our expectations, due to the post-Covid recovery in corporate borrowing and the government’s capital repatriation measures. Continued capital inflows will require further progress in structural reforms, improvement in the global/regional risk appetite, and signs of a reversal in the nominal key rate trend, which is so far heading higher.

USD/UAH: Central bank allows further depreciation

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| USD/UAH | 36.80 | Neutral | 40.00 | 40.00 | 38.50 | 37.70 | 37.00 |

- Central bank: 2023 prospects for the hryvnia remain concerning. Analysts warn that the recent Russian mobilisation may prolong the conflict by at least several months. Moreover, the Ukrainian military progress may slow this winter after recent successes. This leaves the economy struggling with a massive trade deficit (US$5.4bn during the first eight months of 2023), largely reliant on international aid to shore up its FX reserves, currently at $25.2bn owing to a massive injection. However, while the scale of FX intervention has decreased markedly since its peak in July ($4bn), it remains considerable ($2bn in October). The very likely intensification of fighting in early 2023 may again push up the scale of FX intervention required to stabilise the currency. That is why we expect the central bank to allow for further depreciation of the hryvnia, possibly in the first half of 2023.

- Long-term view: The prospects for the Ukrainian currency largely hinge on the timing of an end to the conflict and the ensuing inflow of reconstruction aid. Various estimates indicate that the restoration may cost up to $750bn (or nearly four times the 2021 Ukrainian GDP). A fraction of this should suffice to drive USD/UAH lower, considering the costs of Ukraine’s FX intervention so far.

- New normal: Returning to pre-war USD/UAH levels is impossible, though. Given the massive damage to Ukraine’s infrastructure and means of production, the economy will for years remain dependent on investment-related imports. Even if those could theoretically be covered by inflows of foreign aid, the country will likely aim at maintaining a weaker hryvnia in order to support exports.

USD/TRY: No relief in sight for TRY

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| USD/TRY | 18.60 | Bullish | 19.50 | 21.20 | 22.40 | 23.30 | 24.00 |

- Central bank focus to keep financial conditions supportive: The Central Bank of Turkey (CBT) has delivered 350bp in cuts since August, pushing rates to 10.50%, while also signalling that the rate-cutting cycle will end in November at 9%. The reasoning behind the extension of the rate-cutting cycle at an accelerated pace remains the same. The CBT has cited the need for supportive financial conditions so as to preserve the growth momentum in industrial production and the positive trend in employment. Further signs of a slowdown in economic activity and the recovery in FX reserves since late July are likely factors for the cutting cycle. However, given tighter regulations on the asset side which selectively limit loan growth, cuts are not easing financial conditions quickly.

- Supportive fiscal stance and continuation of selective credit policy: The timing of the recently announced Credit Guarantee Fund package (reportedly at least TRY50bn) and any possible easing in macro-prudential regulations could reverse the recent momentum loss in lending ahead of elections, with the objective of further supporting domestic demand. Policymakers are also leaning towards a more expansionary stance on the fiscal side as the budget deficit, estimated in the Medium Term Program at 3.4% of GDP in 2022, has been rapidly increasing from c.1.4% in September. The budget deficit forecast for 2023 is 43% higher than this year's forecast. And we should not rule out a breach of this target as the elections approach – scheduled for June 2023.

- Inflation and external imbalances remain as major concerns: While the policy mix has tilted to a more supportive stance lately, sustained disinflation is not likely unless real rates are normalised. The recent steps are not sufficient to facilitate an external rebalancing which will be determined by the evolution of energy and gold imports. In this environment, TRY is likely to remain under pressure not only because of macro fundamentals but also because of the current unsupportive global backdrop. A recovery in FX reserves will be more challenging in this environment.

USD/ZAR: Surprise fiscal outperformance

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| USD/ZAR | 17.20 | Mildly Bearish | 18.00 | 17.50 | 17.25 | 17.00 | 16.50 |

- Some good fiscal news: For many years, the fiscal position has been the rand’s Achilles' heel, including the high-profile downgrade to junk status of its sovereign bonds in 2017 and their removal from key bond indices in the 2017-20 period. However, the October budgetary statement in parliament projected South Africa running a fiscal surplus next year and the country’s gross debt-to-GDP stabilising at lower and earlier-than-predicted levels. This has helped the sovereign five-year CDS retrace from the 360bp levels seen in late September. This suggests that if external conditions improve, the rand would be rewarded.

- Terms of trade will be key: As a high beta, EM commodity exporter, the rand is also very much driven by both commodity prices and China’s performance. Commodity prices and weak imports had helped South Africa’s current account position switch to a strong surplus in 2021 and early 2022. Into 2023, however, the South African Reserve Bank (SARB) forecasts the terms of trade declining 17% and the current account moving back into deficit. South Africa will also be playing its part in the energy transition as it switches from coal and the hope is that the nation’s electricity provider, Eskom, can find some stability if the sovereign assumes a big chunk of its debt.

- The profile: It seems as though international investors have started to find value in the rand when USD/ZAR trades at 18.50. We think it could trade there again into early next year if the Fed tightens US real rates still further. Yet the global stagflation story is well flagged and into 2023 we think investors could switch to a more reflationary mindset if it looks like the Fed is preparing to cut rates later in the year. Equally, it is hard to see investors remaining as pessimistic on China for the entirety of 2023. We therefore see USD/ZAR trading back to 17.00 and possibly even 16.00 as 2023 progresses.

USD/ILS: Shekel well positioned when equities turn

| Spot | Year ahead bias | 4Q22 | 1Q23 | 2Q23 | 3Q23 | 4Q23 | |

|---|---|---|---|---|---|---|---|

| USD/ILS | 3.40 | Bearish | 3.50 | 3.40 | 3.25 | 3.10 | 3.00 |

- Equities a key driver: 2022 has proved a strange year for the shekel in that when the Bank of Israel (BoI) finally turned hawkish, and with good reason, the shekel sold off along with the rest of the EMFX complex. Recall that for many years the BoI had been battling shekel strength with a large FX intervention campaign. Apart from widespread dollar strength, it also does seem that the shekel is very much driven by equities. Here, declines in overseas (mainly US) equities markets drive margin calls to Israeli buy-side investors and generate shekel weakness. We tentatively expect this dynamic to reverse in the second quarter of 2023.

- Strong economy: The Israeli economy is expected to grow around 6% this year and 3% next year – even when the US and Europe are likely to be in a recession. Perhaps Israel should be warier of second-round inflation effects than most since the economy is operating above capacity and at full employment. However, the BoI hints that its tightening cycle might end around the 3% area and that inflation should come back into the BoI’s 1-3% target range by the end of 2023. The risks would seem to be skewed towards the BoI needing to tighten further.

- Why we like the shekel: Israel runs a 3%+ of GDP current account surplus, has strong domestic growth and a central bank not afraid to get involved in FX markets – meaning that shekel weakness will not be particularly welcome. In our experience, USD/ILS is always at the forefront of the dollar trend and if the dollar does turn in the first half of 2023 as we expect, USD/ILS should come a lot lower. Less concern over deflation by the BoI should mean that it will be more tolerant of USD/ILS breaking below 3.00 towards the end of 2023 – which could be the surprise.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

FX Outlook 2023: The dollar’s high wire act

- This bundle contains 6 Articles