CEE: Risk of sticky inflation forces central bankers to hike

- 5 November 2021

- FX Hungary Poland

Disruptions in global value chains weighed on Central and Eastern Europe in the third quarter and the Delta variant blurs the outlook for the fourth. Yet the 2022 activity outlook remains sound. Record high inflation can no longer be written off as temporary though, with labour markets tighter than those in developed markets

Economic activity losing momentum but prospects for 2022 remain quite bright

After a strong rebound in the second quarter following the lifting of pandemic restrictions, GDP growth in CEE3 (Hungary, Poland, and Romania) moderated in the third quarter. Sequential growth (quarter-on-quarter) may suffer in the fourth quarter to an extent. The main downside risks are:

- Supply-side bottlenecks in global markets (Hungary is the most sensitive);

- Labour market frictions due to shortages of qualified workers;

- Increases in global commodity prices, including energy, and maritime freight costs;

- The Delta variant outbreak (Romania is most sensitive due to low vaccination rates).

Prospects for growth in 2022 remain bright, but with risks tilted slightly to the downside. Although all the factors mentioned above will stay in CEE3 countries into 2022, economies will remain in the post-pandemic economic upswing, still heavily supported by public funds and a solid labour market performance.

Hungary and Poland are, however, struggling with unlocking access to advance payments from the new EU Recovery Fund due to legal disputes with the European Commission. In early December, the European Court of Justice will announce a ruling on compliance of the conditionality mechanism with the EU Treaties. Thus, the Hungarian government is pre-financing projects. Romania’s National Recovery Plan has been given the green light and the country will receive some €3.8b later this year.

Labour markets in CEE3 were tight and minimum wages were expanding even before the pandemic. Thus labour cost pressures should come to the fore in 2022 with a pro-inflationary impact. CEE3 governments are pouring oil onto the inflationary fire, not only with accommodative fiscal policy (e.g. PIT rate cuts in Poland, payroll tax cuts and tax refunds for families in Hungary), but also sizeable hikes in minimum wages (e.g. by 10% in Romania and Hungary, and 7.5% in Poland).

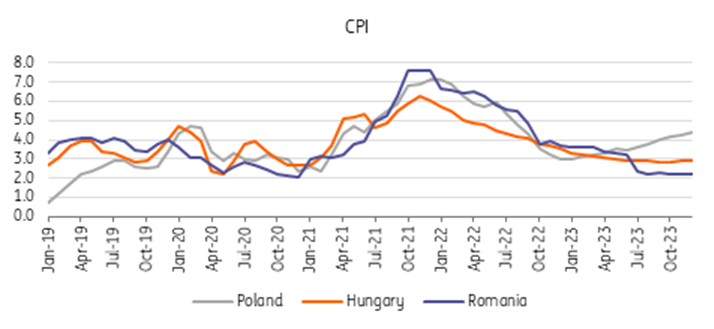

Inflation close to the peak in CEE3. In 2022, wages and demand come to the fore

Increased inflationary pressures and more interest rate hikes coming

There is no doubt that supply-side factors have been a primary driver of accelerating inflation from the spring. But, in addition to energy and food, price increases have become generalised and visible in elevated core inflation numbers. This signals that inflation is becoming widespread and in 2022, the contribution of demand-side pressures and wages should take a leading role in holding core inflation at elevated levels. For example, Polish CPI accelerated to 6.8% year-on-year in October with prices rising in 70% of the categories in the CPI basket.

The most hawkish central bank in CEE3, the National Bank of Hungary, started with a cycle of interest rate hikes in June 2021. It raised the base rate by 120bp in five steps - from 0.6% in June to 1.80% in October. Its forward guidance remains hawkish, clearly pointing towards further rate hikes, which will continue in early 2022 with an additional 100bp. We see the terminal rate of 2.75% being reached by spring 2022 (just before the general election in April 2022).

One of the most dovish central banks in Central Europe, the National Bank of Poland, is catching up after making a surprise 40bp hike in October. The market surprise resulted from misleading forward guidance repeatedly provided in its communication. In early November, the NBP delivered another hike – by 75bp and again above consensus. This is due to the rising inflation risk, e.g. CPI above 7% YoY and more visible risk of second-round effects. Also, the new NBP projections showed average CPI in 2023 above the 3.5% upper bound of the 2.5% inflation target. The tightening cycle should bring the main policy rate to 2.5% in 2022/23 - with upside risk.

Romania, which has been very dovish until recently, launched a tightening cycle in October with a 25bp move. We expect a 50bp hike at the next meeting and 25bp at each of the following meetings, until we reach 3.00%. But that depends on the NBP as well, as the interest rate differential needs to stay positive for Romania.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

ING Monthly: Curve surfing

- This bundle contains 11 Articles