Bank of England dashboard: Why a May hike is a 50:50 call

- 8 February 2018

- United Kingdom

What we expect from the Bank of England and markets on 'Super Thursday'

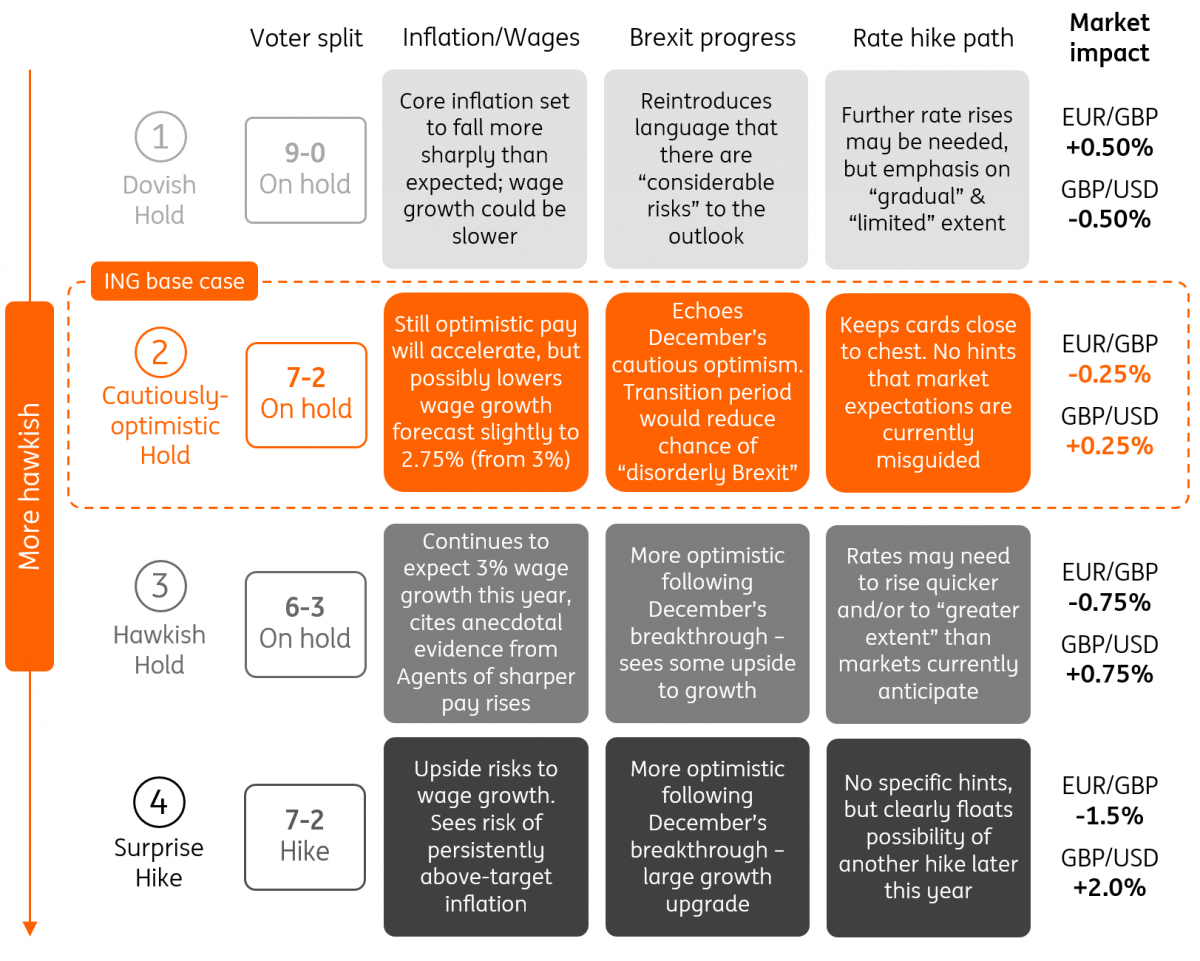

Scenario analysis: How markets could react on Thursday

No hike this week, but a May rate rise is a 50:50 call

Back in November, the Bank of England (BoE) hiked rates and hinted that more could be to come. Since then, policymakers have done little to talk up the possibility of a February hike. True, there has been some better news on wage growth, but Brexit remains a big uncertainty. There has been little progress so far towards an agreement on a transition period, nor has there been much further clarity on the UK's desired trade model.

But come May's meeting, steps should theoretically have been made on both of these issues. Assuming wage growth remains on track, that could be enough to satisfy policymakers that another rate hike is required. The Bank will also be acutely aware that the hiking window could close fairly rapidly over the summer as Brexit noise heats up ahead of the October deadline for a deal.

Markets are currently pricing roughly a 50% chance of a May rate hike, and that sounds about right to us at this stage. We suspect the Bank will be fairly comfortable with this too, and this week we expect it to keep its options fairly open, albeit continuing to strike a fairly optimistic tone. But if the BoE opts to upgrade its growth forecasts, remains bullish on wage growth and explicitly sounds more optimistic on Brexit, then that would send a fairly strong signal that another rate hike is likely in coming months.

Here's our Bank of England dashboard with five things policymakers will be watching at the February meeting...

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more