How governments are tempting corporates with CCS: Carbon Capture and Storage

- 17 February 2022

- Energy Sustainability

Carbon capture and storage is a key technology for the transition towards net-zero emissions by 2050. Governments around the world are shaping CCS support mechanisms to trigger far greater corporate investment. But we're still far from a world where CCS alone can steer the world to its stated climate goals. And it's not without controversy

CCS projects are picking up globally

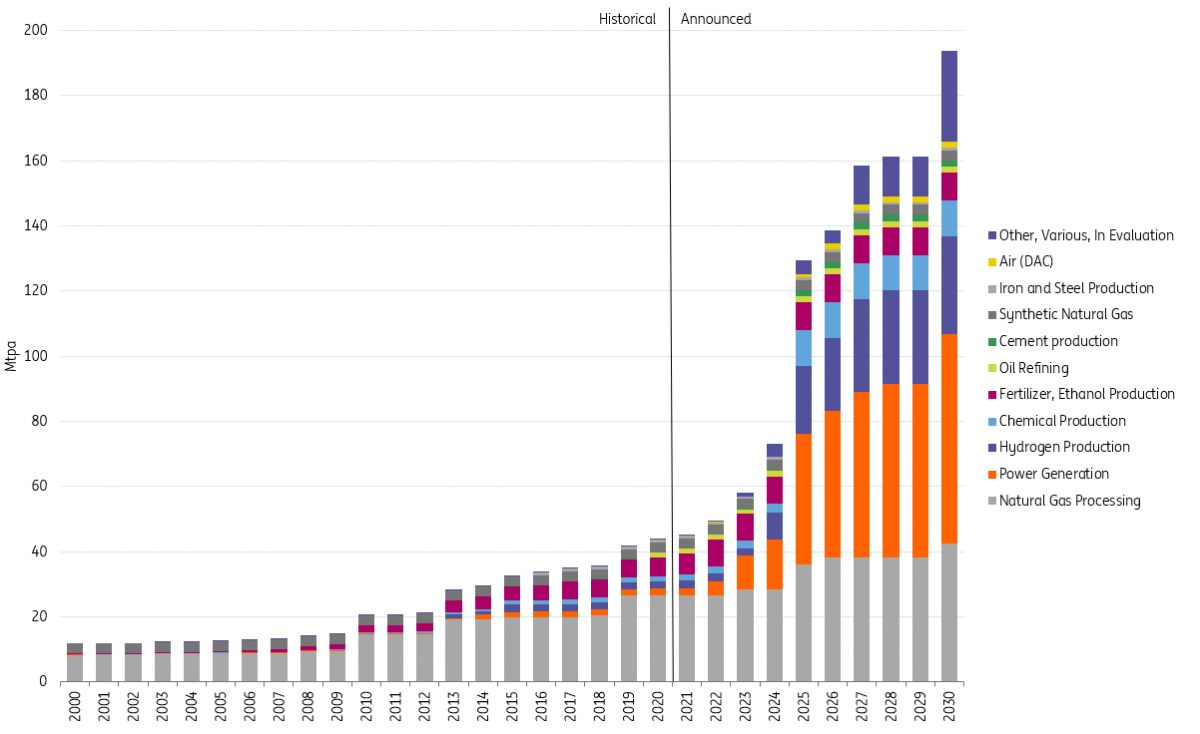

Companies around the globe are increasingly looking to deploy carbon capture and storage technology. They're acknowledging the huge potential of CCS in strengthening corporate sustainability efforts and decarbonising the global economy and we're already seeing a steady rise of such projects worldwide. As of 2021, all operating CCS facilities that were operational or in construction had a capacity of capturing roughly 40 Mt of carbon dioxide annually. These projects also feature a growing trend of diversification in both geography and point source capturing.

CCS to play a unique role in the transition towards a net-zero economy

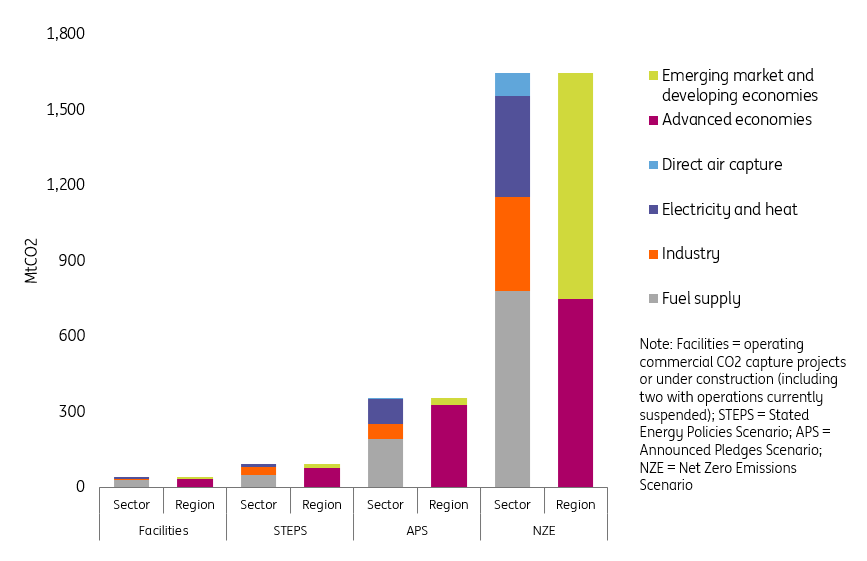

The deeper decarbonisation there is in future energy scenarios from the International Energy Agency, the bigger the role CCS will play. Under the IEA's Announced Pledges Scenario (APS), where all governments’ climate commitments are set to be met in full and on time, carbon capture capacity will grow to 350 Mt CO2 per year by 2030. That's from the current 40 Mt CO2 per year.

Estimated CCS capacity will surge further under the Net Zero Emissions Scenario by 2050 Scenario (NZE) to around 1.7 Gt CO2 per year in 2030—almost five times bigger than under the APS. The IEA also forecasts that CCS will account for as much as 18% of the emissions reduction needed between 2030 and 2050 to get the world to net-zero emissions by the middle of the century.

CO2 capture capacity by project and scenario, 2030

Emissions reductions by mitigation measure in the Net-Zero Emissions scenario, 2020-2050

Admittedly, the biggest challenge to the scaling-up of CCS has been cost. For instance, the levalised cost of production with CCS can range from $70-$130 per tonne in cement production, featuring an increase from $30-$80 per tonne when production is unabated.

However, if industrial producers are looking to reduce their emissions, which they will increasingly be required to do as companies and governments work toward realising their net-zero targets, CCS is now one of the cheapest options. In ammonia and ethanol production (that is based on natural gas), incorporating CCS would raise the cost by 20%-40%, whereas electrolytic hydrogen would increase the cost by 50%-115%. This is why CCS is—with its potential to capture large amounts of CO2 per year—is likely to be particularly attractive for hard-to-abate sectors such as cement, steel, and fertiliser. The technology is gaining additional attention with its potential to be paired with bioenergy (known by the acronym BECCS) and generate negative emissions.

CCS will become a crucial way of reducing net emissions

And since fossil fuels will not be completely phased out by the middle of the century, even in the Net Zero Emissions Scenario, CCS will become a crucial way of reducing net emissions. Yet because of this, CCS also risks being used to delay disruptive carbon reduction as opposed to being viewed as an adjunct to decarbonization efforts. To tackle this problem, a range of efforts is needed from governments, investors, corporates, environmental groups, and the public to keep CCS in check. It's become clear that CCS used for coal-fired power generation will be way less tolerated in the future.

That said, despite its key position in reducing global emissions, CCS is still in a nascent stage of development and corporates will need to rely on government incentives to reduce cost and/or enhance revenue to deploy more, larger projects. Governments are recognising CCS’s potential, and many are embedding—even prioritising—CCS policies and initiatives into their climate plans.

The US: Benefitting from CCS tax credits and network effects

The US has been gaining stronger momentum in developing CCS: during the first nine months of 2021, 36 of the 71 newly added CCS projects worldwide were in the States. This is not only because of the country’s geological advantage in storing CO2 but also because of government policies and investment plans.

The US has been gaining stronger momentum in developing CCS

One major revenue stream is the Internal Revenue Service’s Tax Credit for Carbon Sequestration (Section 45Q), which was enhanced in 2018 to allow industrial players to receive up to $50/tonne of CO2 that is permanently sequestered and up to $35/tonne of CO2 utilised.

It is possible that the Section 45Q tax credits will be raised again.

Under the proposed Build Back Better bill, CCS projects would be eligible for an $85 credit per tonne of CO2 stored. The bill is currently stalled due to objections from key Senate Democrats. The tax credit increase for CCS could be smaller in the final bill, but it would still play a boosting role in incentivising CCS deployment. On the state level, California’s Low Carbon Fuel Standard (LCFS), which allows more low-carbon technologies to be eligible for carbon credits, offers additional incentives for the development of CCS.

Yet scaling up CCS needs not only revenue stream incentives but also fast advancing technologies to reduce cost and increase efficiency. The Energy Act of 2020 directs over $6bn for CCS research, development, and demonstration (RD&D) from 2021 to 2025. This includes rolling out commercial-scale demonstrations, large-scale pilot projects, and front-end engineering and design studies.

Moreover, Biden’s infrastructure bill, signed into law last November, plans to invest $11bn in CCS demonstration and networks. Currently, the largest CCS network in the US is ExxonMobil’s proposed Houston Ship Channel CCS Innovation Zone at the Gulf of Mexico, with an ambition to capture 100 Mtpa of CO2. Meanwhile, BECCS networks are emerging in the Midwest, thanks to lower costs of bioethanol production. That said, the US is expected to further benefit from the cluster effect of CCS networks.

Europe: Netherlands, UK, Germany and Nordics racing to the top

A world leader in setting ambitious emissions reduction targets and legislating climate action, Europe is also an early adopter of CCS. Indeed, Norway’s Sleipner facility was the world’s first commercial CO2 storage project, operational in 1996 and capable of capturing 1 Mtpa of CO2. Today, the Netherlands, the UK, Germany, and the Nordic countries are all in the race to scale up CCS.

Europe is an early adopter of CCS

The Netherlands, with a target to halve emissions from 1990 levels by 2030, envisions CCS to contribute to 50% of the emissions reduction required in the industry sector. To realise this goal, the Dutch government expanded its energy production subsidy scheme (SDE++) which now include CCS. The government provided $6bn during the first round of subsidy applications in 2021. Of this, $2.4bn was granted to develop the large Porthos CCS facility that would store CO2 in the North Sea.

The UK aims to capture 47 Mtpa of CO2 by 2050 by investing in RD&D, expanding infrastructure, and enhancing financial incentives. Moreover, the UK picked two sites in northern England last year to develop industrial CCS clusters. The East Coast Cluster, supported by BP, Equinor, Drax, and SSE is expected to capture 27 Mtpa of CO2 by 2030. The HyNet North West project backed by Eni and Progressive Energy hopes to produce low carbon hydrogen from capturing 10 Mtpa of CO2.

Germany, the EU’s largest cement and steel producer, is suited to developing CCS in the long-term with its proximity to the North Sea. However, due to opposition from various stakeholders, Germany’s law prohibits developers from storing carbon. But it does allow them to capture CO2, transport it, and store it abroad. This requires CO2 infrastructure from industry clusters such as the Ruhr area to the northern part of Germany and/or connections to the future CO2 infrastructure in the Netherlands. Other efforts are also picking up speed; Germany established a subsidy program to scale up CCS, direct air capture, and BECCS, with €105mn allocated for the year.

The Nordic countries are also active in implementing their CCS strategies. Among others, Norway greenlighted $1.2bn worth of funding to the Northern Lights CCS project that is led by Equinor, Shell, Total to capture 1.5 Mtpa of CO2 per year. In late 2021, the Danish Energy Agency granted €26mn to the Greensand project that is led by INEOS and will be the pillar of a CCS network in Demark.

Looking to the wider European Union, two key frameworks can boost the adoption of CCS. The first is that the EU ETS carbon price for the power and manufacturing sectors has now reached levels that support many CCS applications. We've written about that here.

Europe's carbon price tripled in 2021 to €90

European carbon price in mandatory EU ETS market

The second is the EU Taxonomy, a classification system defining which projects are sustainable and directing investment toward these projects. The EU Taxonomy sets carbon intensity thresholds for cement, steel, chemicals, hydrogen and natural gas. CCS will become attractive to investors if a project developer can demonstrate that the integration of CCS can bring their carbon intensity to below the taxonomy’s standard. For example, the proposed emissions norm for newly built gas-fired power plants can only be met through the application of CCS.

Australia: Long-term investment and carbon credit rewards

Developing CCS has also been a priority for Australia. It adopted a national Technology Investment Roadmap in 2020, aiming to direct Australian investments in new and developing low emissions technologies in the short, medium, and long term. Under the roadmap, CCS is identified as one of the prioritised low-emissions technologies.

To achieve these goals, the Australian government is investing more than A$300mn in CCS over the next decade, with A$250mn dedicated to developing CCS hubs, expanding infrastructure, and backing RD&D projects, and the remaining $50mn allocated to funding six specific CCS projects.

Last October, the government also announced that it would issue Australian Carbon Credit Units (ACCUs) to CCS projects. Under Australia’s carbon market, the government can purchase ACCUs that are created from qualified carbon reduction or avoidance projects through the established Emissions Reduction Fund. LNG producer Santos’ Moomba project, which expects to capture 1.7 Mtpa of CO2 in north-eastern South Australia, expects to sell generated ACCUs either to the government or privately.

CCS developers need to conduct rigorous planning, testing and management early on

Admittedly, Chevron’s Gorgon CCS-incorporated LNG facility in Australia did not meet the target of capturing 80% of emitted CO2 and operated at half capacity during its initial full year. The operator has announced plans to purchase carbon offset credits as compensation and to invest in low carbon energy projects in the state. While the Gorgon facility did still inject 5Mt of CO2 as of July 2021 and various other CCS projects worldwide have shown success, the takeaway is that CCS developers need to conduct rigorous planning, testing, and management right at the start of a project to avoid overpromising.

China: Five-Year Plan pushes for more CCS projects

As China has established ambitious targets to achieve carbon neutrality by 2060 and peak emissions by 2030, CCS is set to play a crucial role in decarbonising its economy. As much of China still depends heavily on coal for heating and electricity generation, and as the country relies on the industrial sector for economic growth, it could benefit from implementing large-scale CCS projects and networks. It is estimated that a successful CCS roll-out could curb the country’s emissions by as high as 60% by 2050.

CCS could reduce China’s coal emissions

Coal demand in megatons of oil equivalent (Mtoe) in the IEA scenario based on current policy measures by governments

Realising the huge potential of CCS, the Chinese government has, for the first time, laid out a vision to develop large-scale CCS demonstration projects in its 14th Five-Year Plan (2021-2025). China’s CCS capacity is on the rise: last year, Guohua Jinjie coal power plant completed the instalment of a 150,000 tonne/year carbon capture facility - the largest to date - adding to the country’s six operating commercial facilities and 12 operational pilot and demonstration facilities. One of China’s largest producers, CNOOC, has also kicked off the country’s first offshore CCS project with the aim to capture 1.46 Mtpa of CO2. With a handful of projects in development, as well as a CCS hub planned at Xinjiang Junggar Basin, China’s CCS capacity will steadily increase, although the absolute amount is still low compared to the US.

China’s national emissions trading system (ETS), officially launched last year, will in the long term benefit the development of CCS as the technology can help bring down CO2 emissions and generate carbon trading credits, but in the short term, the impact would be limited. China’s national ETS initially covers only some 2,000 power plants and there is no punishment enforced if these entities failed to limit their emissions within the threshold as of now. Since the start of the national ETS, credits have been trading below $10/tonne, which is too low to make the CCS business case more viable.

Japan: Leading on international collaboration and technology know-how

The Japanese government has been making efforts to promote CCS not only domestically, but internationally. Domestically, Japan’s Trade and Industry Ministry (METI) published the Carbon Recycling Map that outlines the potential of commercialising CO2 utilisation technologies. The office of the Prime Minister released the Environment Innovation Strategy in 2020, highlighting the vision of developing low-cost CO2 capture technologies and applying CCS to producing blue hydrogen. METI is also planning to provide financial support to upstream developers which integrate CCS into their production processes.

The country has also been very active in facilitating international collaboration in CCS. In January, Japan and Indonesia signed a memorandum of cooperation on CCS, hydrogen, and ammonia, mainly through sharing technology know-how and encouraging joint investment opportunities. Japan also led the launch of the Asia CCUS Network, including Asia-Pacific governments and more than 100 companies and organisations to nurture a more promising CCS business and research environment in the region.

CCS could become a $200+bn market annually

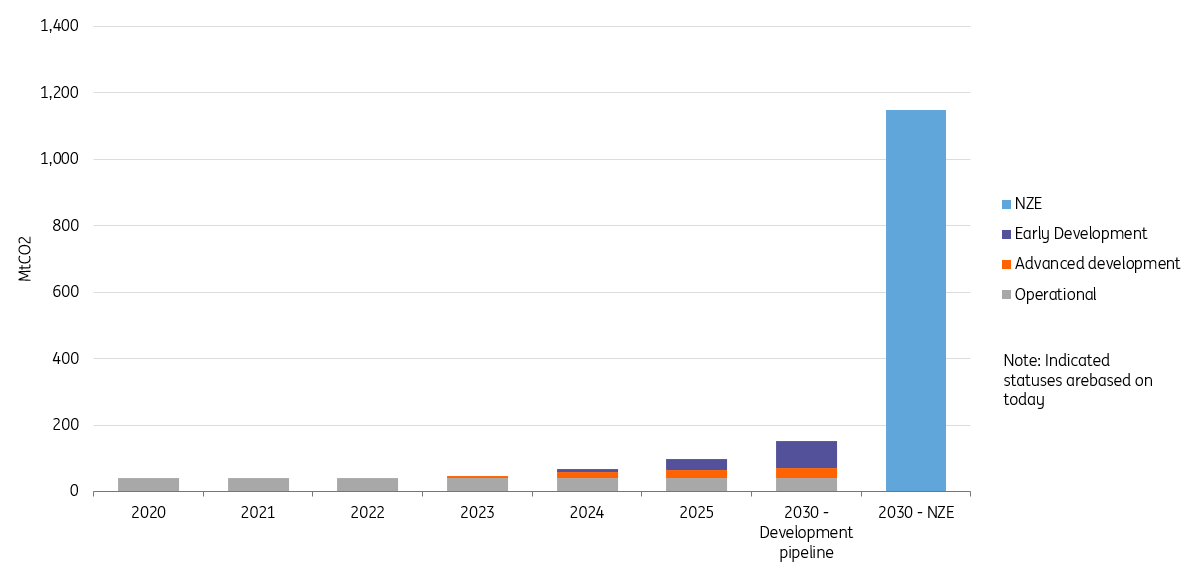

Despite these positive movements, government policies and initiatives so far aren't enough to scale up CCS to a level needed to get the world to net-zero by 2050. According to the IEA, the annual large-scale CCS capacity in industry and transformation needs to reach almost 1,150 MtCO2 by 2030. That is a significant jump from the actual capacity of 40 MtCO2 in 2021.

Large-scale CO2 capture projects in industry and transformation

Actual vs. Net Zero Emissions Scenario (NZE), 2020-2030

Additionally, the IEA forecasts that $205bn is needed annually by 2030 to be invested in CCS development for the world to stay on track to reach net-zero emissions by 2050, but according to Bloomberg New Energy Finance, the global investment in CCS fell slightly to $2.3bn in 2021.

There's still a huge gap to bridge

There's still a huge gap to bridge. And it's also important to remember that CCS is controversial among some environmentalists who regard it as technology that perpetuates fossil fuel exploration and detracts from efforts to eliminate it.

That said, three things need to happen before corporate investment in CCS can really take off:

First governments need to support the designation of storage hub areas and incentivise investments in either new or repurposed existing infrastructure to transport and store carbon as this is not easily done by the market. And there's more; governments need to focus on amending existing policies and licenses to allow (long term) carbon storage.

Second, governments need to establish policies that can enhance CCS projects’ revenue streams making the CCS business case viable for companies. The EU Taxonomy, the US’s Section 45Q credits, and the ETS mechanism in several countries have proven to be effective. But more generous incentives, clearer implementation guidelines, and established enforcement mechanisms are all needed to boost investment in CCS to desired levels, at least from a climate perspective.

Finally, increasing funding in research and development should be devoted to CCS, as more advanced technologies can more effectively capture and store CO2, reduce project costs, and make the technology more scalable and profitable.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more