Bank of Canada to hike rates by 25bp as domestic pressures build

- 25 February 2022

- Canada

Concern about the Omicron wave led the Bank of Canada to delay hiking rates in January. These worries appear to have been misplaced with the domestic economy firing on all cylinders and inflation at 30-year highs. A 25bp rate hike is our call for next week’s meeting despite geopolitical nervousness, but this may not be enough to lift the loonie

Tightening to start with a 25bp move

Even after Russia’s invasion of Ukraine, financial markets are fully priced for a 25bp rate hike from the Bank of Canada (BoC), with increasing speculation that it could turn out to be a 50bp move next Wednesday. To us, 50bp appears unlikely given the global caution prompted by Russia’s military assault on Ukraine, but certainly there is a strong domestic case for a sustained tightening of monetary policy starting with a 25bp move.

In January, the BoC admitted it was a close call on whether to hike interest rates, but the Omicron variant’s uncertain economic impact made them hold fire. They felt it would "weigh on activity in the first quarter”, but suspected it would be “less severe than previous waves” of Covid and economic growth would “bounce back and remain robust over the projection horizon”.

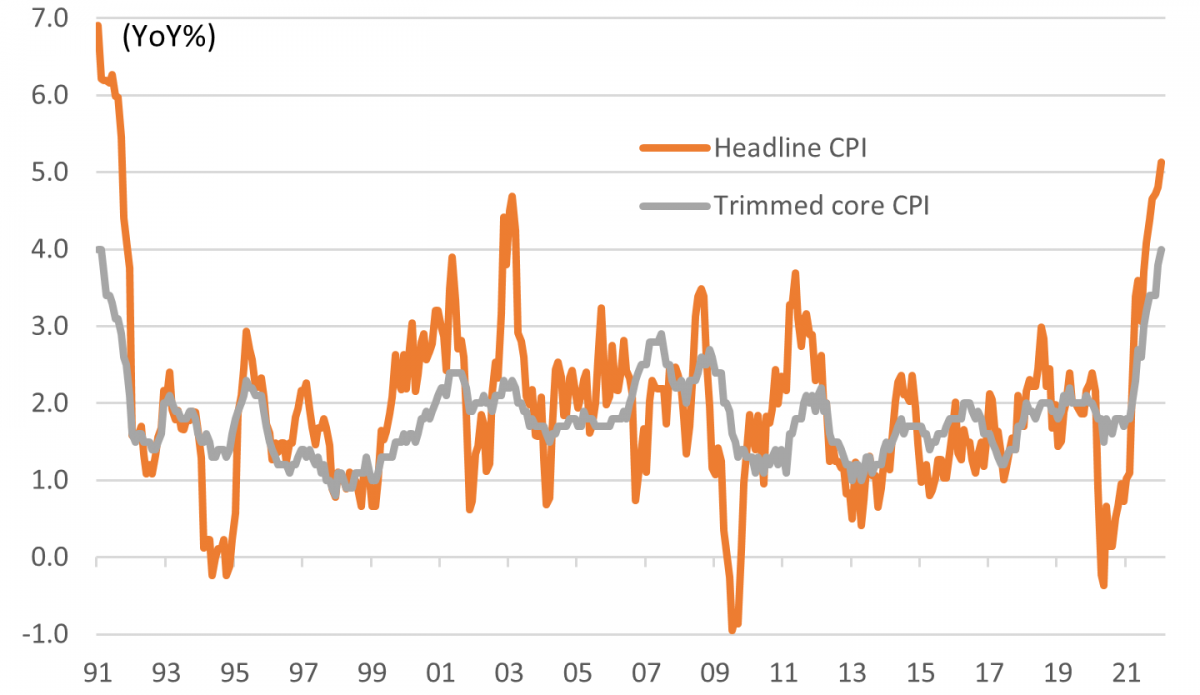

The actual economic impact is likely to be marginal with Covid case numbers plummeting since the start of the year while business and sentiment surveys have improved. The BoC has already admitted that “economic slack” has now been “absorbed” and that “the labour market has tightened significantly”. Moreover, inflation continues to climb and now runs at 5.1% for headline CPI, the fastest rate in more than 30 years.

Deputy Governor Tim Lane, speaking a little more than a week ago, warned that the Bank was “alert” to the risk that inflation may again prove to be more persistent. In turn, this could necessitate the BoC being both “nimble, and if necessary, forceful” in adjusting monetary policy “to address whatever situation arises”.

We continue to look for six interest rate increases in total from the Bank of Canada this year

Given the increase in commodity prices in response to Russia’s military action, this will actually be positive for the Canadian economy, which is likely to stimulate more investment in this key sector. Consequently, we continue to look for six interest rate increases in total from the BoC this year, with a further three in 2023. This would leave the policy rate at 2.5% by the end of next year, a level it was last at all the way back in October 2008.

FX: 25bp hike not enough to lift the loonie

Markets have increasingly speculated about the idea of a 50bp rate hike by the BoC over the past week, with the overnight indexed swap (OIS) market currently pricing an implied probability greater than 50%. As discussed above, this is not a remote possibility, but we expect a more conservative 25bp rise. Accordingly, we expect some weakness in the Canadian dollar (CAD) after the BoC announcement, which may however be moderated by some hawkish forward-looking message, which should cement the market’s expectations of five to six more hikes by the end of the year.

Domestic drivers in most major currencies are currently playing a very secondary role as the Russia-Ukraine conflict keeps sending shockwaves across asset classes. CAD is exposed to the conflict via its high beta to global risk sentiment, but the spike in oil prices and limited direct implications for Canada (unlike for European countries) means that CAD can withstand the Ukrainian crisis somewhat better than some of its peers (like the Swedish krona, Norwegian krone, the euro or the pound).

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more