Canada inflation preview: The only way is up

- 21 March 2019

- Canada

Inflation should stay below-target in February, but from here the trend is more likely to be upwards. But with the Fed hinting at a long pause and a mixed economic backdrop, a Bank of Canada rate hike later this year hangs in the balance

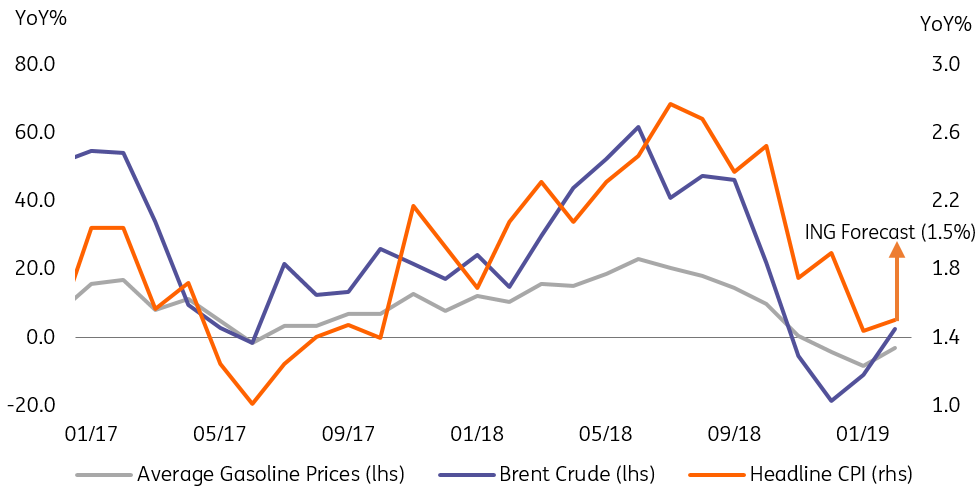

January took the brunt of the late-2018 decline in oil prices, but things are looking slightly better in February

Weak gasoline prices took their toll in January, which saw headline inflation sink to 1.4%. However, we see a slight change of tune in February. The negative effect of weak energy prices should begin to dissipate, and while we anticipate the headline figure (1.5%) to sit below-target, we suspect this will be the beginning of an upward trend in prices. Our commodities team see oil prices edging slightly higher throughout this year and next.

Gasoline prices recovered in February, though are still in negative territory

Alberta’s crude-by-rail plan: A temporary reassurance for oil prices?

Canada’s energy sector has been battling with transportation constraints for some time now, and these aren’t expected to be alleviated until new pipelines come into operation. Meanwhile though, the Alberta government will invest $3.7 billion into the shipment of crude oil via rail – one of the only alternative forms of transport in light of major pipeline shortages. If this plan is able to facilitate higher crude exports, and perhaps help support Canadian prices, it could add some extra impetus to inflation too.

February painted another positive picture of the labour market, but core inflation could still be at risk

Another month, another welcome pick-up in wage growth (2.3% YoY). In our recent piece (Canada’s labour market: Resistant to the turbulence) we discussed the increasing signs of strength in the labour market, and we reckon that this should add a decent level of support to core inflation. That said, the housing market and overall spending performed poorly in the fourth-quarter of last year, suggesting the labour markets strength is struggling to translate into better household activity.

the labour markets strength is struggling to translate into better household activity

The Liberal government’s 2019 federal budget (released recently) could offer some respite. Amongst the budget winners were first-time home buyers who, due to the government offering to absorb part of the costs, are incentivised to jump on the housing ladder. This alone won’t prevent the housing market from slowing, but it could help avoid a significant downturn.

Bank of Canada: Waiting for it all to blow over, however long that takes

The labour market is undeniably healthy and the Bank of Canada’s (BoC) three main measures of core inflation have happily sat around the 2% target for a while now, but these factors alone aren’t expected to push the central bank out of wait-and-see mode.

The timing of the next rate hike is contingent on how household spending, oil markets and trade developments between the US and China all evolve over the coming months. If we don’t see a materialisation of risks in these three areas, the BoC could still make a move later this year (potentially the fourth quarter). But with the Federal Reserve firmly in dovish territory, the Canadian central bank could equally follow suit and keep policy on hold for longer.

See here for further details on why the Bank of Canada is firmly in wait-and-see mode.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more