Canadian dollar to hit 1.50 as QE looms

More easing by the Bank of Canada (50 basis point cut) is now just a matter of time, and we think quantitative easing is on its way, too. Add to this battered crude oil prices, which pose a serious risk to the oil-centric Canadian economy, and we see USD/CAD marching to 1.50 in the near future

Poor momentum even before Covid-19 hit

The Bank of Canada, like other central banks around the world, has been scrambling to deliver huge stimulus to offset the negative economic shock resulting from Covid-19 and the efforts to suppress its spread. They have delivered 100bp of easing so far and unsurprisingly they “stand ready to adjust monetary policy further if required”. This will almost certainly be the case.

The economic outlook had been weakening even before coronavirus fears started to take hold within Canada. GDP growth had slowed to just 0.3% annualised in 4Q19 and it seemed probable that 1Q20 activity would be depressed by supply chain disruptions because of factory closures in China and other parts of Asia. Exports will also have been hurt by weaker demand from Asia while protests to block the construction of the Coastal GasLink pipeline have had a disruptive effect on rail, road and sea transportation.

As elsewhere, the plunge in equities and bond yields means the economy is also dealing with a financial shock that is increasing the strains in lending markets and depressing both household and corporate sentiment. This is in addition to the demand shock as a sense of fear leads consumers and businesses to change behaviour, which is only exacerbated by government-instigated containment measures. Add in the plunge in commodity prices, most notably oil, and business investment will weaken with the growing threat of job losses in the sector. A sizeable economic contraction is now a certainty for 2Q20.

BoC to deliver 50bp cut and QE

Fiscal policy is set to provide some support, but it is relatively modest compared to other country's proposals. The government will provide what equates to up to 4% of GDP in “direct support to Canadian workers and businesses”. This includes increased child benefit, mortgage support measures, improved access to employment insurance and sickness and care benefits while there are also tax deferral measures included.

Meanwhile, the Bank of Canada has more room than most central banks to provide support to the economy and financial markets with the policy rate at 0.75%. This tool is certainly not impotent since Canada has relatively high household debt levels. We now expect the policy rate to be cut to the 0.25% low reached in the wake of the global financial crisis. The cut may come as part of another impromptu move or at the next policy meeting scheduled for 15 April.

However, with the Federal Reserve ramping up its asset purchase schemes – here’s our take on the Fed’s unlimited QE – and other developed economies having followed suit already, pressure on the BoC to deliver similar measures has been building. This is especially true considering that BoC Governor Stephen Poloz has excluded the prospect of negative rates.

Among countries which have already embarked on QE, Australia and New Zealand – two other open, commodity-dependent economies - may be a framework for the BoC. The Reserve Bank of Australia has recently kicked off its first-ever QE programme (targeting the 3Y yield at 0.25%), and provided forward guidance by announcing that rates will be kept at 0.25% for some time. The RBNZ in New Zealand has taken similar measures in terms of forward guidance by saying that rates will stay at 0.25% for at least 12 months and starting an asset purchase programme on Monday of around NZD 30bn over the year.

We may see the Bank of Canada combining some forward guidance along similar lines with an asset purchase programme, likely more in the style of the RBNZ (and the Fed) rather than the yield-control measures taken by the RBA. Given the BoC has already started to purchase mortgage-backed securities and Bankers acceptances it could be extended to a more formal QE stance that primarily focuses on government bonds, possibly of the order of C$200-250bn, equivalent to around 10% of GDP.

Oil and the end of loonie’s “exceptionalism”

We highlighted above how Canada ended last year with little growth momentum, but other than that, most of the fundamentals did still point to some of that Canadian “exceptionalism” which had helped to keep its currency relatively supported throughout the global trade tensions. Wage growth was high (largely above 4%) compared to other G10 economies, as inflation was solidly at target and, in turn, the BoC saw few reasons to follow the global easing trend. This translated into a highly supportive rate environment for CAD, which was set to lead the carry trade resurgence, as trade tensions appeared to abate.

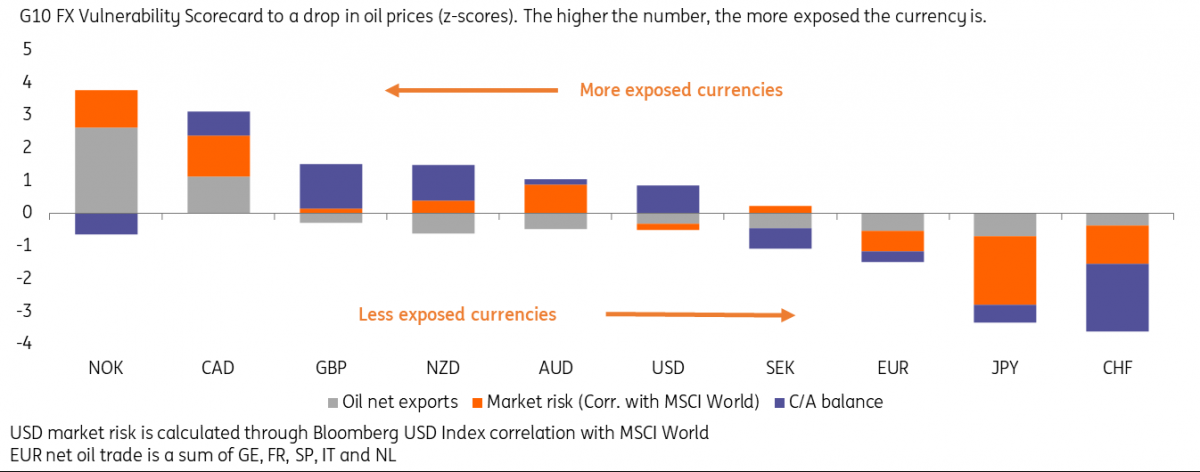

The Covid-19 outbreak has certainly ignited a big correction in risk-sensitive currencies like the loonie, but while the virus-related disruptions are a burden shared by most developed economies, the slump in oil prices is one key idiosyncratic downside factor for CAD, as highlighted in the G10 oil-vulnerability scorecard below (here the original article).

A few statistics reinforce this idea: in 2018, Canada was the world’s fourth largest oil exporter, having sold USD 67bn worth of crude to the rest of the world. This is approximately 15% of total exports and 4% of GDP. The energy industry as a whole accounts for 11% of GDP and is estimated to have employed (directly and indirectly) around 820k people in Canada in 2018.

The oil slump is expected to have a cascade effect on the economy, especially in that of Alberta, where most of the oil and gas industry is concentrated. Covid-19 poses a double threat to the Canadian economy, both internally (as highlighted above) and from an external point of view, as a slowdown in global trade will heavily impact the very open Canadian economy.

CAD highly at risk in our oil-vulnerability scorecard

The fundamental economic resilience relative to most of its G10 peers which had cushioned most of the downside pressure on CAD in the past year is now fading rapidly. And so is that supportive rate environment for CAD, as the BoC will likely push rates to the lower bound and, in our view, embark on QE. CAD was already the least undervalued currency within the G10 $-bloc in the medium term, and our views for relative outperformance in 2020 where based on the highly attractive yield from a carry-trade perspective.

We acknowledge that trying to time the coronavirus narrative (i.e. vaccine, slowdown in infections) is pure guesswork. However, things may well get worse before getting better and excluding the big volatility swings in the USD from the equation, we see the loonie having more room to depreciate, hitting 1.50 in the near future. This is not just because of the Covid-19 story but also because of low oil prices and the ultra-dovish BoC, which are likely going to be the new normal for a while. This simply wipes out any “exceptionalism” that justified CAD's relative outperformance in previous quarters.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more