CAD: Uncertain path, but the best choice in the $-bloc

A resurgence of lockdown-related risks and choppier risk environment highlight more limited downside potential for USD/CAD. Still, a well-paced economic recovery in Canada, no further stimulus from the central bank, a still positive oil outlook and lingering CAD short positioning should favour CAD’s outperformance vs AUD and NZD

The current re-pricing of the global economic recovery, as new virus waves and restrictions loom, has inevitably hit the pro-cyclical Canadian dollar, which is back at the 1.34 level last seen in July. Recent developments are forcing us to slightly revise our views on the loonie, although we continue to identify some factors that suggest CAD may not stand out as an underperformer among the pool of activity currencies. We see four key factors at work:

Bank of Canada unlikely to add more stimulus

The Bank of Canada has so far broadly followed the Federal Reserve in enacting emergency policy measures to counter the effects of the pandemic: cutting the policy rate to 0.25% and starting quantitative easing.

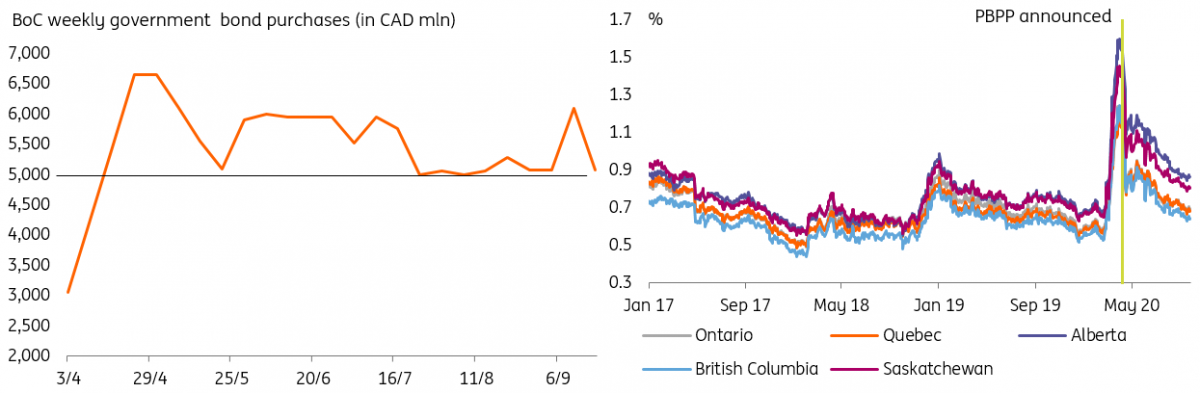

The BoC has not touched its QE programme (neither quantitatively nor qualitatively) since it introduced facilities to purchase provincial and corporate bonds to accompany its bond-buying scheme in April. For now, the new Governor, Tiff Macklem, has not seen enough reasons to add stimulus to the already large monetary package: the pace of purchases under the Government of Canada Bond Purchase Program (GBPP) has not been increased , as most weekly purchases were slightly above or at the minimum CAD 5bn amount set by the BoC (Figure 1). This may signal a relatively low interest to increase the minimum amount of weekly bond purchases anytime soon.

Looking at the provincial spreads, they have been tightening (Figure 2) at a constant pace since the introduction of the Provincial Bond Purchase Program (PBPP), easing the Bank’s concerns.

Figure 1 & 2 - BoC QE and provincial spreads

Accordingly, the sharp rise in the BoC's balance sheet, also compared to the Fed’s (Figure 3), has been followed by some stabilisation in late summer. From a currency perspective, a slower rise in the balance sheet suggests less negative implications for CAD.

All in all, we see the current amount of monetary stimulus provided by the BoC as adequate to support the recovery and do not expect any increase in the size or spectrum of asset purchases and – even less so – any rate cut in the foreseeable future.

This could create some monetary policy divergence within the G10 commodity space, considering that the Reserve Bank of New Zealand is openly planning to embark on negative interest rates early next year, and speculation around a possible cut in Australia has also risen.

Figure 3 - BoC balance sheet

Canadian economic recovery set to continue

The Canadian economy contracted by 38.7% quarter-on-quarter (annualised) in the second quarter, displaying a worse slump than the US (31.7%), which is understandable considering the stricter containment measures in Canada and the higher exposure to the swings in global trade and commodity prices.

The Canadian economic recovery has been helped by a well-sized fiscal stimulus (already worth around 15% of GDP, waiting for a next round of spending) and monetary accommodation and it has kept pace with the US recovery. The unemployment rate contracted to 10.2% in September after having peaked at 13.7% in May- broadly following the dynamics in the US jobs market. Google mobility data shows that the impact of restrictions in Canada has definitely started to fade and the divergence with the US (which had looser restrictions) has been erased from the mobility point of view (Figure 4).

The Canadian economy has likely digested the slump in oil prices earlier this year, and signs of recovery in global trade have likely fuelled a solid rebound in the third quarter. While the risk of new lockdowns worldwide obviously poses the risk of a slower global recovery, we do not see enough factors to suggest the Canadian economy will lag other major economies.

Figure 4 & 5 - Canada's virus situation is not too alarming

If anything, the virus situation appears more under control in Canada compared to other regions, as shown in Figure 5. While Canada will remain very exposed to new contagion waves and lockdown measures in the US, this may suggest a more limited need for more restrictive measures in Canada compared to other countries, which bodes well for the economic recovery.

Finally, political turmoil appears to be easing in Canada following a complicated summer where another scandal caused the resignation of Finance Minister Bill Morneau. It appears now that the Trudeau administration has made it through the worst, and can still count on a high approval rate for its Covid-19 policy response.

More support for oil is not off the charts

Demand is indeed the key question mark for the crude oil price outlook. The recovery in demand is proving slower than previously expected and a key driver of such recovery – Chinese buying – appears to be drying up. Meanwhile, weak refinery margins are failing to provide much incentive to increase utilisation rates.

On the supply side, OPEC+ is refusing to agree on more output cuts for now, but it is still making steps forward in terms of compliance, by asking those who fell short of their commitments to compensate for their previous poor performance.

While there is plenty of uncertainty around the oil outlook, our commodities team remains of the view that a gradual (albeit slower) recovery in global crude demand should still allow oil prices to stay supported in 4Q, where we expect an average 47$/bbl for Brent and 44$/bbl for WTI. For more details on our oil view, see our commodities team’s update: “Oil demand uncertainties linger”.

Lingering short positioning signals less downside risk

In our latest CFTC positioning review piece, we highlighted how all reported G10 currencies except the Canadian dollar had a net-long positioning vs the oversold USD. While this past week’s market movements have likely generated some USD short-squeeze and possibly sent some currencies back into net-short territory, the resilience of CAD’s shorts compared to its pro-cyclical peers has been evident for a few months now (Figure 6).

Should new swings in global risk appetite generate some dollar short-squeezing events, the CAD should be more protected than its peers AUD and NZD.

Figure 6 - CAD's positioning

CAD outlook: uncertain vs USD, but we see value vs other procyclicals

All the points mentioned above aim to highligh how the Canadian dollar still presents relatively solid fundamentals. But the recent setback in risk sentiment and the rise in Covid cases worldwide do highlight a non-negligible downside risk for activity currencies as we head into the US elections in November. In turn, we now see the USD/CAD outlook as more uncertain compared to a few weeks ago, its downside potential as somewhat more limited, and we are inclined to see the pair staying above the 1.30 mark in 4Q.

Still, we believe that a combination of monetary policy divergence (BoC to stand pat, RBNZ and RBA increasingly dovish), a well-paced economic recovery in Canada, a still optimistic oil outlook and lingering CAD short positioning, all point to better resilience from CAD compared to AUD and NZD in the currently unstable global risk environment.

We see room for the recent downtrends in AUD/CAD and NZD/CAD to extend towards the 0.92 and 0.85 marks, respectively.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

25 September 2020

Covid spikes threaten the recovery This bundle contains 10 Articles