Brexit blog: What the latest impasse means for the UK economy

- 18 October 2018

- United Kingdom

As Brexit negotiations stall, the ever-increasing uncertainty surrounding 'no deal' could see businesses take more concrete action and consumers turn even more cautious. For the Bank of England, this makes a rate hike unlikely before March 2019

As another crunch EU Council meeting comes and goes without agreement, the critical issue of the Irish backstop - the insurance policy that would kick in in the event of the UK leaving the single market and customs union - remains unresolved.

Two weeks ago, we discussed how a possible compromise appeared to be in the offing, which would see the UK government accept the EU's backstop proposal, if Brussels kept the door open to Britain remaining in a customs union as a whole. In other words, this plan, which has been rather clunkily labelled the "backstop to the backstop", would eliminate customs checks between Northern Ireland and the rest of Britain in the event the backstop kicked in, but would require goods to be checked against EU rules.

Over the past few days, there have also been indications from both sides that the door could be left open to extending the transition period beyond December 2020. In theory, this would allow more time to find a more workable solution to the Irish border challenge - and in any case, the length of the transition period as it stands is unlikely to be long enough to agree upon the overall future trading relationship.

As ever, the challenge has been to conjure up a 'wording' that will convince enough UK lawmakers to approve this fudge - and recent reports suggest that even the most creative choice of policy wording may not be enough to reassure MPs from the Democratic Unionist Party or Conservative Brexiteers. The DUP has long been concerned about the spectre of regulatory checks between Northern Ireland and the rest of the UK, while Brexiteers within the Conservative Party worry the mooted customs compromise could effectively see Britain tied to the EU for long after the transition period ends.

We are unlikely to know for sure whether 'no deal' has been averted until much closer to the UK's scheduled exit date

Nobody really knows exactly how many of these MPs could ultimately reject the deal when it comes to Parliament. But with no obvious way of squaring the circle, it looks increasingly likely that the UK government is going to play for time. The later the Prime Minister can leave agreeing a deal with Brussels, the later the Parliamentary vote will be held. This would mean the choice MPs face would become a much more binary decision between PM May's agreement, and an economically-risky 'no deal' scenario.

If this is indeed the tactic, it looks increasingly likely that a deal won't be settled until the December EU Council meeting. Given that this summit comes just days before MPs leave for the Christmas recess, it seems likely that the 'meaningful vote' would then follow in mid-to-late January. The government is obliged to give lawmakers a say by 21 January.

In short, we are unlikely to know for sure whether 'no deal' has been averted until much closer to the UK's scheduled exit date in March.

For the economy, this could see growth momentum slow again over the winter as uncertainty rises - and there are two key factors in particular that we think will be worth keeping an eye on:

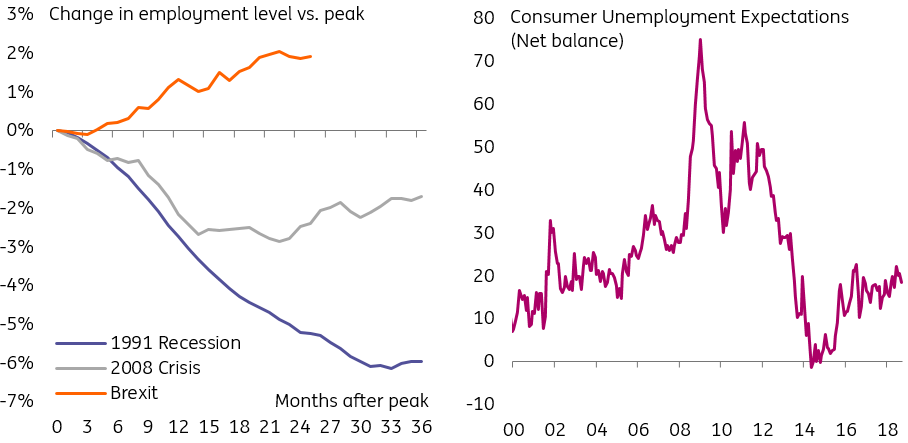

Spending could come under pressure again if job uncertainty builds

With the sun shining, there's little doubt the UK economy had a brighter summer, with consumers bucking the trend of the previous twelve months and spending more. The question now is whether this is the start of a more permanent growth recovery.

For now, we suspect it isn't. There is some limited evidence in the Bank of England's latest credit survey that demand for credit card borrowing surged in the third quarter, suggesting this summer spending can't be sustained indefinitely. And despite some decidedly better news on wage growth over recent months, the near-10% rise in petrol prices since March means incomes are still being squeezed to some degree.

This means retailers will face another testing Christmas trading period, but the real wildcard for the high street stems from how consumers might react to the 'no deal' threat. With businesses becoming more vocal about the impact 'no deal' would have on operations, households may begin to take a more cautious stance if they gradually become more wary about their job security. There is already some evidence - albeit fairly tentative at this stage - in the latest set of jobs numbers that firms are beginning to hold back on hiring decisions.

Consumers currently relaxed about job security - but that could begin to change

Will inventories come to the rescue? We aren't fully convinced

As we discussed back in August, the potential for disruption and delays at UK ports in the event of a 'no deal' would have big implications for supply chains. With time running out, firms may look to insulate themselves where possible by stockpiling items in advance of March to keep their operations moving. The Guardian recently reported that some food-suppliers would look to order extra goods if there is no deal agreed by Christmas.

But while 'no deal' would spell bad news for growth beyond March 2019, any stockpiling efforts could actually theoretically increase GDP before then. This is because it would increase inventories, a notoriously volatile part of the national accounting that frequently triggers large swings in the quarterly growth numbers. However, we think there are a couple of reasons why this may not be the case this time.

Firstly by definition, any pre-Brexit stockpiling would simply result in a corresponding increase in imports, so the impact on domestic demand should largely net out.

Secondly, and more importantly, it's not obvious where firms would store these extra supplies. According to property firm Savills, the US has five times more warehousing capacity per capita than the UK. And most of what Britain does have has been utilised following the rapid rise of internet shopping over recent years. Their data shows that the vacancy rate for warehouses in London sits at just 3%, indicating that there is very limited scope for firms to store large volumes of goods. This is probably even more true of specialist or perishable goods, where the availability of storage that meets their additional requirements is in shorter supply.

Bank of England's November meeting comes at an awkward time

All of this makes for a challenging period for the Bank of England.

In any other situation, we suspect policymakers would like to up the pace of rate hikes given the increasingly good news on wage growth. However, with uncertainty rising, we think a rate hike is unlikely before the UK leaves Europe in March. If a deal can be agreed and passed by Parliament by the end of January, then we think the Bank will look to increase interest rates in May 2019.

However, if the Brexit timetable slips, or the loss of momentum over the winter is more severe than expected, that date could easily be pushed back.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: A sense of urgency, perhaps

- This bundle contains 8 Articles