Brexit and the pound after parliament suspended

The UK government's decision to suspend parliament means the Brexit process is likely to go down to the wire. 'No deal' has become more likely, although we still narrowly think a no-confidence vote, which leads to an Article 50 extension and early elections, remains the most probable scenario

UK prime minister Boris Johnson has announced that parliament will be prorogued – or suspended – between the weeks of 9 September until 14 October, when the Queen's speech will take place.

The big question for markets is: does this decision make a ‘no deal’ Brexit more likely?

We think the answer is yes – slightly – although we suspect the underlying motivation is to steer parliament’s anti-no deal efforts towards a vote of no confidence and election, rather than the legislative path that has emerged over recent days.

It goes without saying however that the next few weeks are heading into unchartered territory. For the pound, all of this means further weakness to come.

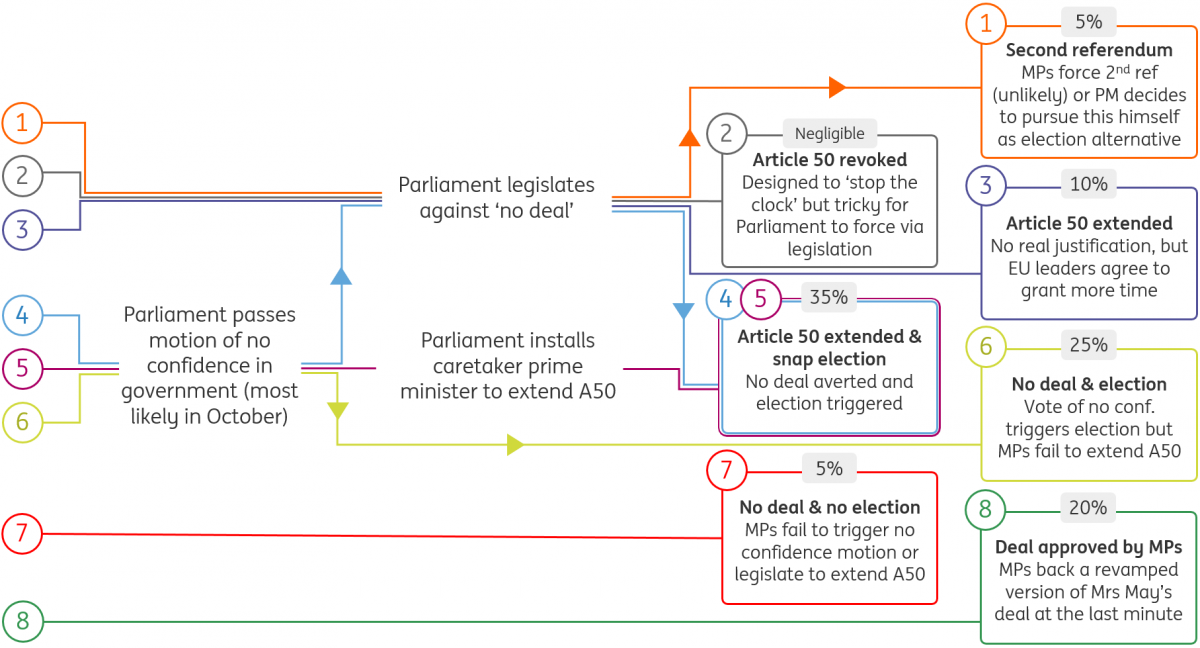

Latest Brexit scenarios and probabilities

Legislative path to blocking no deal now much harder – albeit not impossible

In theory, suspending parliament is a fairly normal event. In simpler times, the government would prorogue parliament for roughly a week before the Queen’s annual speech, used to announce the prime minister’s plans for the next year. But what is more unusual and controversial this time is the length of time involved – around five weeks, which means that when MPs return from recess next Tuesday, they will only sit for around a week before parliament is closed down until mid-October.

The main implication is that this will make the legislative path to blocking a ‘no-deal’ Brexit much harder. This route – which would involve MPs passing legislation to force the prime minister to ask for another Article 50 extension – was already looking difficult. Finding the necessary time in the House of Commons agenda (which is normally controlled by the government) looks tough, and will rely heavily on Speaker John Bercow’s discretion. Even if the time can be secured, lawmakers will need to act fast to pass the necessary legislation to force the prime minister to ask for another Article 50 extension.

Vote of no-confidence may be the only way to block ‘no deal’

If legislative attempts fail, opposition MPs may be left with little choice, but to back a motion of no-confidence if they want to stop a ‘no deal’ Brexit.

This poses a dilemma for many lawmakers, particularly those who are within the Conservative Party, who have previously indicated they’d be prepared to back a no-confidence motion if it were the only way of stopping ‘no deal’.

That’s because the government’s official aim is still to negotiate a deal – and this was backed up by PM Johnson’s constructive approach he reportedly adopted in Brexit talks with European leaders over the past week.

Will these senior Conservative backbenchers be prepared to vote the government down while it’s still seeking a deal? We think it’s unlikely, and so suspect a no-confidence vote will not succeed over the next week or so.

Two main routes to stopping a ‘no deal’ – both are complex and potentially time-consuming

This takes us down to the wire in October

The result is that all of this may well go down to the wire. But while it’s tempting to conclude that the decision to prorogue parliament is to force through a ‘no deal’ exit, we aren’t necessarily convinced this is true. Mr Johnson could have set the date for the Queen’s speech much closer to the 31 October deadline – or indeed after it.

Despite all the noise over the past week, we’re inclined to say the government’s ‘Plan A’ is still to seek a revised deal with the EU. While Mr Johnson adopted a hard-line stance in public while in Europe, reports suggest the British leader was more constructive behind closed doors than the EU had initially expected. The fact that he travelled to Europe last week at all also marked a change of tack – previously Mr Johnson had signalled he would not even be open to talks unless the EU agreed to remove the Irish backstop upfront.

But while the atmosphere surrounding talks may have improved, the path to agreeing to a deal that is both acceptable to the EU and the UK remains as treacherous as ever. The EU has made it clear that the emphasis is now on Mr Johnson to find a way forward, but his recent focus on so-called ‘alternative arrangements’ for the Irish border are unlikely to be enough.

Despite all the noise over the past week, we’re inclined to say the government’s ‘Plan A’ is still to seek a revised deal with the EU

However, there is little doubt that there has been subtle movement on the UK side over recent days – the FT reports that Mr Johnson has signalled to the EU that he is willing to accept the current withdrawal agreement, excluding the backstop. That still sets the bar seriously high for negotiation, but it nevertheless differs to Mr Johnson's earlier stance that suggested he wanted an entirely new deal. Either way, the European Council meeting on 17 October will be a crucial date for the diary.

Of course, getting any agreement through parliament will be extremely tough. Pro-Brexit Conservatives have signalled they may accept nothing short of ‘no deal’. Instead, the government may be betting on the support of a greater number of Labour MPs. There is a pool of say 30 Labour lawmakers who represent staunch Brexit-supporting areas, and according to Politico, some of these lawmakers regret not voting for Mrs May’s deal back in March.

Ultimately though, we still think it will be tough to get the numbers in favour of a deal and think the probability of a deal passing is still roughly 20%.

Key Brexit dates for the diary

Election + Article 50 election still marginally the most likely scenario

If a deal fails to get through parliament – or if we’re completely wrong and a revamped agreement fails to materialise at all – then this brings us back to the vote of no-confidence scenario. If all other routes to averting ‘no deal’ have been precluded, then we think the numbers could quickly materialise in favour of a no-confidence motion.

This is not sufficient in-and-of-itself to block ‘no deal’ on 31 October. MPs will either need to install a caretaker prime minister, or try and rapidly force through legislation, to enable a request to extend Article 50 again. Assuming the latter proves challenging, we suspect the former option would succeed, despite all the current disagreement over who would fill the role of temporary PM.

In other words, we still think a scenario where parliament forces an Article 50 extension along with an early general election (likely to take place post - October 31) is still narrowly the most likely outcome of all of this - perhaps with a 35% probability

Equally though, there’s no firm guarantee that either legislation or a vote of no-confidence will be enough to stop the government if it is really set on pursuing ‘no deal’. We think the probability of the UK exiting without an agreement on 31 October has risen to around 30% - perhaps even slightly higher.

Forced election could suit the government

Having said that, an election forced upon the Conservatives may not be the worst scenario for the government. While conventional wisdom suggests Mr Johnson needs to get Brexit done before an election, going to the polls in the immediate aftermath of a ‘no deal’ exit would be incredibly risky given the potential for severe disruption.

An election that is forced upon the government, and coupled with a further Brexit delay, would allow Mr Johnson to campaign on a tough Brexit stance, without risking the economic impact of a pre-election ‘no deal’. It would also allow him to tell voters that he didn’t want this election or delay, and attack the opposition for trying block Brexit from happening.

Don’t forget that the Queen’s speech, scheduled for 14 October, will give the government an opportunity to formally outline some election-tailored pledges – focussed on the NHS and crime in particular.

GBP: More weakness to come

PM Johnson’s intention to suspend parliament underscores the uncertainty and the ample downside risk the pound faces over the coming weeks.

Even if parliament attempts to legislate against 'no deal', the week-long window before parliament is suspended is unlikely to be long enough for this to succeed. It also seems too early for a no-confidence vote to be successful (this in our view will likely happen in the latter part of October). This suggests more pressure on GBP as the perceived risk of a 'no deal' Brexit won’t be reduced during the first half of September. If anything it could rise, pointing to further sterling weakness.

We look for GBP weakness to build into the mid-October EU summit, given a deal still seems unlikely and the uncertainty about a hard Brexit will increase. This is when we expect EUR/GBP to re-test the multi-year high of 0.9325 reached earlier this month.

The recent compression in GBP risk premia (be it as a measure of our short-term EUR/GBP financial fair value, or EUR/GBP risk reversals – Figures 1 and 2 respectively) points to room for further GBP downside, as risk premium can be rebuilt into GBP yet again.

However, in the final two weeks of October (after the EU summit), the most likely scenario is that the UK parliament delivers a vote of no confidence in the government and paves the way for early elections. This should stabilise GBP in the early part of 4Q19 as the worst case of a 'no deal' Brexit is averted. However, it is still too early position for the eventual GBP rebound at this point as we believe things will get worse before they get better.

Figure 1: GBP risk premium

Figure 2: EUR/GBP risk reversals

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article