Brazil: The (micro-)economic revolution

- 3 September 2019

- Brazil

Doubts over Brazil’s growth outlook have not ended with the passage of the pension reform and the impressive progress in the pro-business micro agenda. These have lifted our optimism about the longer-term, but external uncertainties and the inability to jumpstart activity through fiscal stimulus suggest that near-term prospects are not easy to assess

Policy directives are laser-focused on boosting productivity

Even though the big macro-economic fiscal reforms such as the social security and tax reforms tend to get the big headlines, perhaps the most consequential changes taking place in Brazil right now are happening somewhat under the radar.

These are part of a longstanding productivity-enhancing agenda that has gained unparalleled momentum under the current administration. The current effort is spearheaded by Economy Minister Paulo Guedes’s team, with the critical help from Central Bank governor Roberto Campos.

As illustrated by the approval of several critical micro-focused initiatives during President Temer’s tenure, this agenda was not created by the current administration. Among the many legislative achievements by Temer, easily the most successful of any previous administration on this metric, we’d highlight five:

- the labour reform, which reduced Brazil’s record for spurious labour litigation,

- the outsourcing law, which regulated outsourcing for a broader range of activities,

- the reorientation of the policy directives for the BNDES development bank, with material implications for monetary and fiscal policies,

- the establishment of electronic invoicing, which vastly improved the quality of the collateral in some business loans, and, lastly,

- the “Distrato Law”, which restricted the ability of residential buyers to unilaterally withdraw from a contracted sale of a still-unfinished residential project, sharply reduced the financial risk incurred by builders.

To a significant degree, this agenda is inspired and steered by the World Bank’s “Doing Business” project, which uses objective metrics covering business environment and regulations to rank countries with an “Ease of Doing Business” score.

Despite all that was achieved by President Bolsonaro’s predecessor, the level of ambition to fight well-entrenched special interest groups feels new, as any visit with the Economic Ministry team in Brasilia would attest. Special interest groups that recently clashed with the administration include wide range public sector associations, and, for instance, private sector groups representing the construction and the print-media industries.

The sense of urgency created by the severe impact of the economic recession and widespread unemployment may help explain that determination. But it’s also driven by the implicit support provided by popular fatigue with left-leaning policies, notably the long-dominant agenda promoted by public sector employees, the failure of the left in the elections and their reduced size in Congress, which severely curtailed their ability to block legislation.

It’s difficult doing business in Brazil, but change is coming

Few global multinationals are not present in Brazil, given the size of the domestic market and how closed it is to external competition. Still, talk with any corporate operating in the country and it quickly becomes clear their immense frustration with the excessive cost and uncertainty inherent to doing business in the country.

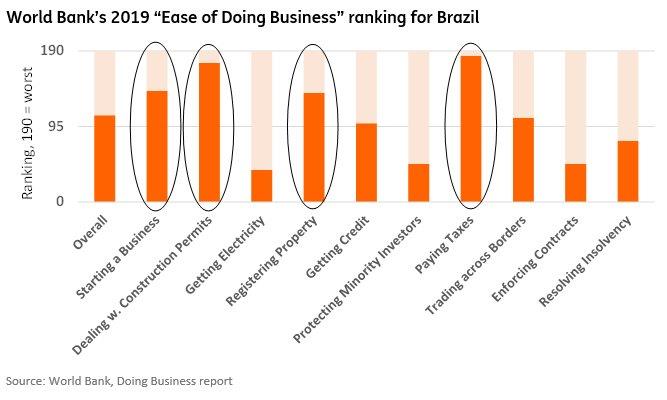

Those challenges are often a result of the encroachment of the state in business activities in Brazil. And this economic “dead-weight”, as Economy Ministry officials like to say, can be illustrated by the poor ranking received by Brazil in the World Bank’s “Doing Business” project, which ranks Brazil (the 9th biggest economy in the world by GDP and 6th by population) with a low 109th place (out of 190 economies).

The chart below, depicting Brazil’s ranking in each of the components of the overall “Ease of Doing Business” indicator, serves as a useful reference to understand current policy priorities.

As seen in the chart, the biggest obstacles businesses face in Brazil, ie, where the country is a big outlier when compared with other economies, involves the difficulties in paying taxes and in obtaining all the permits and licenses while meeting the myriad of regulatory requirements needed to start and run a business in the country.

The difficulties created by Brazil’s byzantine tax code are well-known but it is still surprising to realize that it is surpassed only by six other countries, according to the report, with Brazil occupying the 184th place. For instance, corporates spend nearly 2,000 man-hours per year to prepare, file and pay for taxes in Brazil, versus 159 hours in high-income OECD countries.

To help address this issue, Congress is currently debating a tax reform, which is expected to be approved in the Lower House by year-end and in the Senate by next year. This is a high-stakes reform and its chief aim is to simplify and rationalise the tax code, merging several taxes into a single VAT tax. We are confident that a reform will be approved, but just like the social security reform, the question is whether the tax reform will cover just federal taxes or a wider range of local and federal taxes, in which case its impact on business productivity would be much greater.

For the other three areas highlighted in the chart, the report finds that, for instance, to register a new business, incorporation lawyers spend the equivalent of 18.5 days in Brazil vs 9.3 days in high-income OECD countries. In dealing with construction permits (Brazil’s ranking = 175), a company must follow 20 procedures and it takes 404 days to build a warehouse vs 13 procedures and 153 days in high-income OECD countries. Lastly, in order to register a property in Brazil, buyers and sellers must go through 14 legally required procedures vs an average of 4.7 in high-income OECD countries.

Fighting “all kinds of little things”

Many of these obstacles are already being addressed by Congress, or directly by the executive, as much of it requires just the sign-off from the executive branch. The general aim is to rationalize and simplify Brazil’s labyrinthine regulatory code, increasing transparency and minimizing red tape.

The number of regulatory changes being targeted (the so-called “regulatory norms” or “NRs”) is too large to list here, with several involving red-tape in rules and regulations involving the workplace for instance. But we’d highlight the changes included in the recently-approved Economic Freedom executive decree, which focused on drastically simplifying the regulatory regime in place to open and run small businesses.

A sharply-reduced number of legal procedures are now required to open small businesses, which now can operate more freely, with a simpler, less intrusive and innovation-friendly regulatory regime that eased restrictions on a wide range of issues including hours of operation, inspection and price-setting.

To borrow from an interview recently given by former CB governor Arminio Fraga, what we are witnessing is a “guerrilla-type warfare against all kinds of little things”. Alone, they may not amount to much but, in aggregate, and in conjunction with the superior macro-policy directives being implemented, they should help generate considerable productivity gains for private sector activities. The competitiveness of local producers should gradually improve and, eventually, this should pave the way for the reduction of import barriers and tariffs, which is another key policy goal of the current administration.

The upcoming “credit revolution”

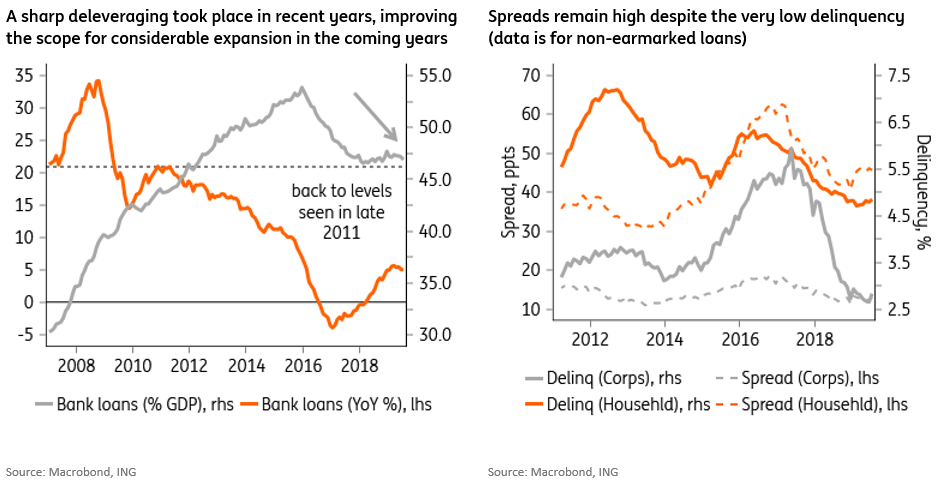

Even though Brazil doesn’t rank so poorly on credit-access metrics – as seen in the chart above – the country gets an exceptionally low score for its laws covering collateral and bankruptcy proceedings. This severely increases the risk of lending in Brazil, which helps explain the notoriously high spreads prevailing in the local financial system.

A new law covering these issues has been under debate in Congress for a couple of years now, and government officials believe that the debate is now at its final stage, and that the political momentum is favourable for its eventual approval over the next year.

But, for the central bank, legal insecurity is only part of the problem. And tackling other elements that contribute to the high spreads, such as competition and financial innovation, appears to be one of the most urgent items on the bank’s agenda.

The sharp expansion of subsidised and targeted credit helped temporarily. In particular, bank officials are keen on incentivizing private sector innovation in banking and insurance, expanding the number of financial products offered and increasing competition by encouraging the participation of new players, notably fintechs.

Several initiatives have been introduced to help develop real estate-related credit, including reduced capital requirements for home equity loans, and initiatives aimed at boosting mortgage securitisation, such as the introduction of new CPI-indexed mortgage facilities, and facilitating funding, by incentivizing the use of the covered-bond securities launched last year, known as Letras Imobiliárias Garantidas (LIGs), that banks can issue to fund mortgage activities.

The much-anticipated “cadastro positivo” (“positive registry”), which paved the way for the arrival of US-style credit bureaus is another landmark piece of legislation that was just approved and is about to become reality. Up until now, only delinquency registries (or “bad credit” bureaus) were allowed in Brazil. The new regime should help reduce delinquency and the spread for good borrowers.

It should also contribute to the democratization of credit as the incorporation of telecom/electricity payment tracking in the system should allow for a large segment of the population that is currently unbanked, to gradually build a credit score, which should improve prospects for higher bankarization.

Improving financial education is another key focus of this agenda, as Brazilians have been used to high interests for so long that it may take a while for them to, for instance, abandon the widely-used overdraft facilities, known as “cheque especial”, which still charges 300% interest. This is similar to the 2017-18 bank initiatives that successfully restricted the use of costly revolving-credit lines offered by credit card companies and, with the help of increasing competition, sharply reduced the fees charged by credit card processing firms.

Several other initiatives have been implemented and many more are in the process of being implemented. As CB governor Roberto Campos recently stated, credit will play a central role in Brazil’s recovery, and the central bank is “thinking big”: “we know how to create the biggest credit market revolution Brazil has ever seen”.

“We know how to create the biggest credit market revolution Brazil has ever seen”, said the CB's Campos

These are strong words coming from an institution known for carefully-considered assertions, but it reflects the enthusiasm easily found among government officials in Brasília these days.

Campos should be helped by the sharp deleveraging that took place in recent years (as seen in the chart above) and the fact that the SELIC policy rate is on track to drop to a record-low 5%, and this is altering the incentives by borrowers and lenders in a way that should facilitate the “revolution” he seeks. This is evident in the new appetite Brazilians are showing to shift their savings away from government Treasuries and money market instruments and into higher-yielding alternatives in both credit and equity markets.

And, as a result of that, new funding opportunities for (corporate) borrowers should open as the local credit and equity markets deepen.

The retrenchment of state banks is long-overdue but add to the fiscal contraction

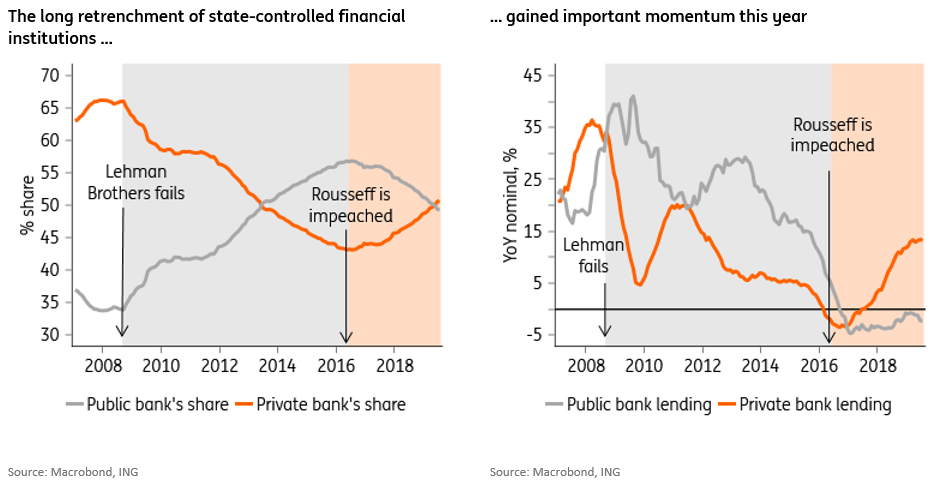

The state presence in the financial industry expanded enormously during the PT years, as seen in the charts below. This reflected the fact that state banks were deployed as an arm of the Finance Ministry to boost (para-fiscal) policy stimulus.

The sharp expansion of subsidised and targeted credit helped temporarily sustain GDP growth, but it also had a considerable detrimental effect over the effectiveness of monetary policy and it distorted the economy’s asset allocation.

As the charts above show, as the global financial crisis intensified, following Lehman Brothers' failure in mid-2008, not only the Lula administration kept-up a fast budget-spending pace as revenues collapsed but, crucially, it pushed state-controlled banks to sharply expand lending at an unprecedented pace. State banks were eager to comply and by mid-2009 their loan portfolio was increasing at a 40% YoY pace.

By June 2013, state-controlled banks controlled the largest share of the local financial system for the first time since 2000. But that process is quickly reversing now and, as of May this year, private sector banks again control the largest share of the loan portfolio.

Importantly, just like this policy change resulted in substantial (para-)fiscal policy stimulus during the PT years, the opposite is taking place now, adding material downside to near-term growth. But, in our view, the medium-term advantages of current policy directives vastly compensate for the short-term downside it represents in terms of near-term growth.

The medium-term advantages of current policy directives vastly compensate for their short-term downside

Among other things, the reorientation of public bank policies will 1) help alleviate fiscal accounts as it allows these institutions to repay their Treasury loans sooner, 2) increase the overall efficiency of asset-allocation in the economy, as government-selected “national champions” become a thing of the past, and 3) perhaps more importantly, it deeply alters monetary policy.

One reason for that is the fact that the local financial market used to operate essentially in two separate segments: one for borrowers that had access to subsidized state-bank funding, including the now-retired TJLP, and one for the rest of the economy. As a result, the SELIC policy rate had to be set at a higher level given that a large chunk of Brazil’s credit market was insensitive to the policy rate, as market-set rates only affected those that did not have access to the subsidized rates available at state-banks.

As a result, 1) monetary policy is much more effective now, as a much larger share of the local financial system is now sensitive to the policy rate, and, as a result, 2) historical estimates of the neutral level for the policy rate are likely biased to the upside.

The second point is particularly pertinent now that the SELIC rate is reaching record-low levels and authorities try to assess the appropriate level of monetary stimulus to deploy.

Monetary policy stimulus is here to stay

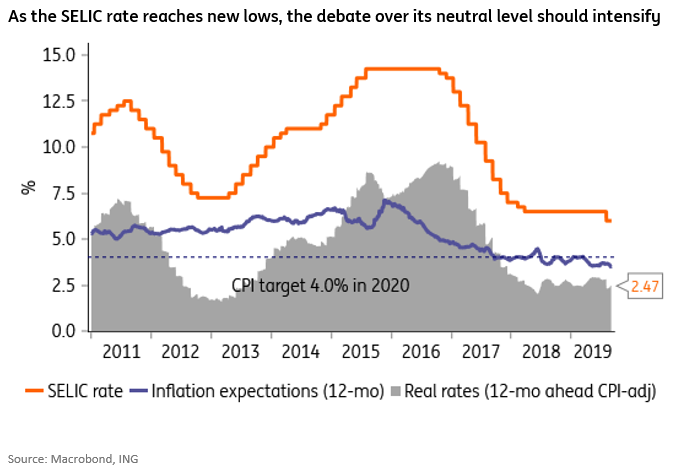

Although the central bank does not publicize its estimate for the neutral level for the policy rate, it has historically been considered to be very high, in the 4-5% range in CPI-adjusted terms. This is much higher than the levels prevailing across inflation-targeters in LATAM, generally estimated in the 1-2% range.

Even though there’s growing acknowledgment in the local market that structural changes in credit markets have caused the neutral SELIC rate to drop, the only statement bank officials express in public is that, in their assessment, the current level for real rates, 2.47% as seen in the chart below, is considered to be expansionary, ie, the neutral is estimated to be somewhere above 2.5%.

We believe that local assessments for what is the neutral rate in Brazil will evolve considerably in the coming quarters, as the structural changes that have been implemented since the end of the Rousseff administration deepen. And, in our view, the bias is to the downside, such that the levels prevailing in Brazil move gradually closer to the levels prevailing among its regional peers.

Monetary policy will also be critically informed by the evolution of fiscal policy. And as seen in the 2Q GDP report, government consumption is likely to be a drag in economic activity in the foreseeable future.

This reflects the fact that the public sector fiscal balance needs to tighten by at least 4-5ppt of GDP to return to a sustainable trajectory, and this substantial fiscal tightening (intensified by the retrenchment of state-banks) will add an important hawkish bias to the policy mix in the coming years.

This suggests that, when the central bank calibrates the level of policy stimulus needed, it should also incorporate the fact that part of that stimulus is being offset by the fiscal policy contraction. As a result, when taking both fiscal and monetary policy into consideration, the policy mix is likely less expansionary than generally thought.

As a result, given the persistently wide output gap, with large spare capacity seen in both industrial activity and labour market, the SELIC policy rate can be cut at least 100bp further, to 5%, without risking turning the policy mix excessively loose.

In fact, we would not be surprised if the market and analysts start considering prospects of even lower SELIC rates, after recognising that given the very large output gap and benign price dynamics, even lower levels of the SELIC rate should be contemplated, particularly if economic activity remains lacklustre for longer than expected.

Privatization is another emblematic taboo that no longer afflicts Brasília

Perhaps due to a mix of fiscal crisis, widespread evidence of corruption among state-owned companies, and the weakening effectiveness of public sector workers’ associations, another sea-change taking place in Brasilia is the embrace of privatizations, or at least the sharply weakened position of anti-privatization forces.

As Bolsonaro stated a month ago, ideally he would like to see the privatization of at least “one small state-owned company per week”. Statements like these would amount to political suicide not too long ago in Brazil. Apart from historical popular opposition, privatizations have also been resisted by politicians. As the Lava-Jato corruption scandal illustrated, state-controlled companies are a critical link in the political patronage system, which Bolsonaro, under the guidance of Guedes, appears to be intent on breaking.

The new Supreme Court's understanding that allowed subsidiaries of state-controlled companies to be sold without Congressional approval was a landmark decision. That decision already resulted in deep changes for Petrobras and state banks (Caixa and Banco do Brasil), which sold or are in the process of selling all subsidiaries deemed secondary to their core businesses.

Supreme Court decision to allow subsidiaries of state-controlled companies to be sold without Congressional approval was a landmark decision

Another leverage that the federal government has now is the fact that many states are in very difficult fiscal situations. And, in order to qualify for federal assistance, states must now comply with a series of requirements to adjust their fiscal accounts, among these is the sale of state-owned companies they control.

Beyond the sale of assets, it should also be noted the deeply changed mindset inside state-controlled enterprises. The governance shock, which started with the approval of the “Lei das Estatais” (“SOE Law”) in 2016, is hard to overstate, as the curtailment of political appointments (and interference) in SOEs has deepened since Bolsonaro took office. The same applies to regulatory agencies, with the new legal framework recently signed into law by Bolsonaro also helping increase transparency and shield the agencies from political interference.

The changes have been particularly impressive for the banks, and Petrobras, while electricity and public utility companies are also under consideration. In fact, government officials are confident that Eletrobras (LATAM's biggest power utility company) will receive the authorisation by Congress to be privatized next year.

Stronger longer-term growth conviction contrasts with short-term uncertainties

Despite our optimism with Brazil’s new economic policy directives, we remain sceptical about the country’s near-term growth dynamics.

Given their nature, the gains resulting from the bulk of the structural changes being implemented will only materialize in the longer-term while fiscal constraints impede the administration from conducting any type of counter-cyclical fiscal policy.

As a result, the administration is severely constrained in its ability to execute a near-term stimulus package. The upcoming authorization for workers to withdraw some funds from their unemployment savings accounts (FGTS) is the exception here, but its impact on consumer demand is likely to be relatively small (estimated at 0.2-0.4 ppt of GDP in the next 12 months). As a result, the pace of the recovery should be heavily dependent on the private sector’s “animal spirits”.

Local corporates are cautiously enthusiastic about the future, but heightened trade-war-related uncertainties abroad, together with the political noise generated by Bolsonaro’s more controversial pronouncements, have hampered their ability to make big investment decisions.

But the 2Q GDP report provided some encouraging news on this respect. Even though 2Q was a period of heightened domestic uncertainty (ie, before the social sec reform was approved by the Lower House), investment rose and contributed with 50bp of the 1.8% QoQ (SAAR) expansion registered in the period.

The administration could also counter with an even more frontloaded push on the infrastructure concessions and privatizations’ front, but these projects take time to come into fruition.

Overall, even though we’ve become considerably more optimistic about Brazil in the longer term, the risk is that strong headwinds represented by the global slowdown (weighing on net exports) and the fiscal contraction keep near-term growth dynamics weak for longer, and that the recovery is more gradual than the administration would want.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more