Brazil: End-cycle uncertainties

- 3 February 2020

- Brazil

Despite the FX weakness, market pricing for one last 25bp rate cut should help tip the balance in favour of a cut at this week’s policy meeting in Brazil. Moreover, the negative shock represented by the coronavirus outbreak has also increased the risk that further cuts may be considered, which would weigh on the Brazilian Real

The risk of a dovish surprise has increased

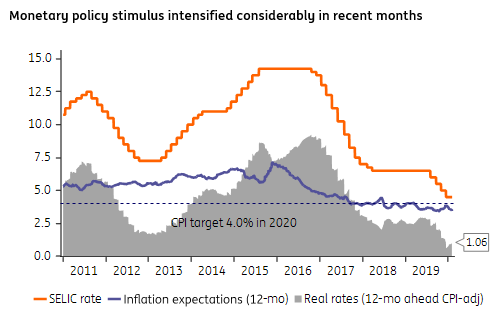

This week’s monetary policy meeting has become the subject of intense local market debate. Contrary to what we had expected, the Brazilian central bank (BACEN) did not close the door to additional rate cuts at its December policy meeting, when it matched expectations by cutting the SELIC rate by 50bp to 4.5%.

Moreover, recent public statements by bank officials further fuelled expectations that the bank was comfortable enough with the inflation outlook, despite the recent (temporary) rise in headline inflation, to deepen the easing cycle a bit further.

Local market pundits are split on what’s the right thing to do, but consensus in favour of a cut has strengthened lately. Despite the recent inflation surge, from a 2.5% year-on-year low in October to 4.3% now, inflation expectations remain fully-anchored and below-target for 2020, while the moderate pace of the economic activity recovery suggests that scope for monetary stimulus should remain ample in the foreseeable future.

However, monetary policy is already quite expansionary, with real rates having now reached all-time lows of 1%, versus neutral levels possibly in the 3-4% range. Moreover, the Brazilian Real has weakened considerably in recent months, with the USD/BRL consolidating now above 4.20.

The uncertainty about the impact that rate cuts would continue to have over FX markets is, for us, the main argument for BACEN to avoid additional rate cuts. But, despite FX risks, market pricing of one last 25bp rate cut should tip the balance in favour of a cut on Wednesday, bringing the SELIC rate to 4.25%. Moreover, the risk of a deeper China-driven external shock could lead BACEN to keep the door open to further cuts.

USD/BRL consolidation above 4.20 calls for caution

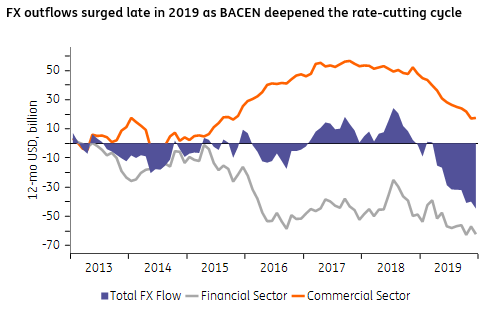

BACEN officials can claim that with inflation expectations still fully anchored, FX weakness is not a major macroeconomic concern. Still, as the extraordinary amount of FX outflows seen in recent months continues to show no sign of abating, a pause in the rate-cutting cycle would likely help facilitate an orderly local market transition to this new environment of record-low interest rates.

Much is not well-understood about the causes for the massive amounts of FX outflows seen in recent months in Brazil, and that totalled USD45bn last year (as seen in the chart below). One way or another, outflows have been a result of large-scale adjustments in the local economy as it transitions to this new low-rate environment.

The replacement of external debt with (cheaper) local-currency alternatives is one of the chief drivers for these outflows, as often highlighted by BACEN officials.

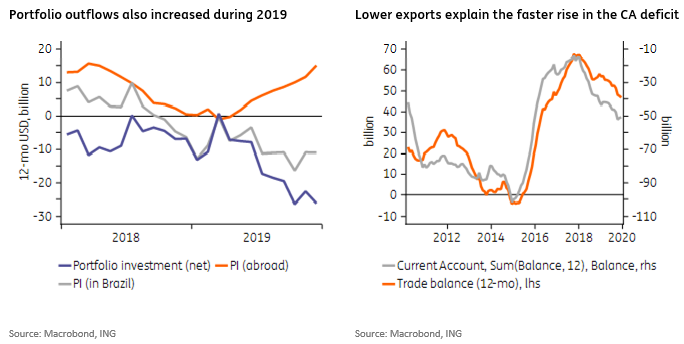

But other factors also help explain FX outflows. They include portfolio outflows, which have risen as locals have tried to diversify their financial holdings by shifting part of their portfolio abroad (chart below). In addition, the current account deficit has also risen faster than expected, having ended 2019 near 3.0% of GDP, up from a low of 0.7% of GDP in 2017, largely thanks to the fall in exports to key markets such as Argentina and China.

Overall, it’s unclear how long and how persistent these outflows will be but, for us, a more supportive BRL environment depends on the eventual confirmation that the monetary easing cycle has been concluded (with no additional policy rate cuts) and, more importantly, stronger evidence that an activity recovery is firmly under way.

Favourable base-effects should help 2020 GDP growth

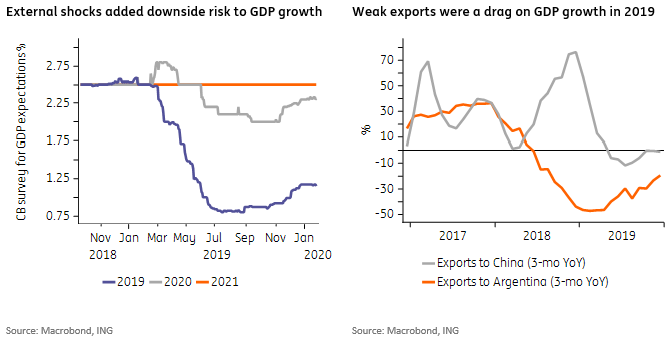

A more positive assessment regarding the outlook for the economic recovery was taking hold at the end of 2019, as seen in the chart below, but recent data, especially the lukewarm activity data for November, frustrated expectations and triggered a reassessment.

4Q GDP data has not yet been released, but 2019 GDP growth should not diverge much from the 1.2% consensus. We see much more room for evolution in the 2020 forecast, which has increased to 2.3% in recent weeks but still looks unstable there.

Our forecast of 2.7% is clearly on the more optimistic end of the spectrum. With a carryover of about 1.0% at the start of the year, the balance of risks to our forecast looks balanced, in our view, but heightened external market uncertainties added material downside risk to near-term trends.

The risk to external trade, which should remain an important drag on Brazil’s GDP growth in 1Q, has increased considering Argentina’s unresolved debt renegotiation process and, especially, China’s coronavirus outbreak. This has increased downside risk to the 1Q GDP print, suggesting that a more positive turnaround in 2020 GDP expectations trajectory may take a little longer to take hold.

As seen in the chart above, exports to Argentina and to China suffered throughout 2019, affected by the recession in Argentina and the swine-flu in China. Recent trends suggest that, following the impressive 35% drop in exports to Argentina, and the 2% drop in exports to China seen in 2019, room for additional drops in 2020 were more limited. The ongoing coronavirus outbreak in China has altered that, and now suggests that exports to China could drop further, delaying the export recovery.

On the domestic front, mining activities should also rise in 2020, following the shock represented by the disaster at Vale’s Brumadinho dam in 2Q19, but the largest driver for GDP growth this year should continue to be rising investment and consumption. Domestic demand should continue to benefit from the reduction in macro uncertainty, following the approval of the social security reform last year, and the impact of the 200bp monetary stimulus that took place during 2H19.

Continued evidence of the steady recovery in the construction sector, a key credit-sensitive and labour-intensive sector, bodes especially well for a faster recovery.

Monetary policy has also had tremendous impact over local capital markets activities, as seen in the surge in local market issuance, both through fixed-income instruments and IPOs. As reported by Anbima, these issuances increased 60% YoY, in nominal terms, in 2019.

Overall, the healthy carryover, the favourable base-effects represented by the removal of the 2019 shocks, reduced macro uncertainty, and a full-year of monetary stimulus bode well for faster economic activity in 2020.

External demand, along with the persistent fiscal contraction, should remain important headwinds, especially in 1Q. But the net-negative contribution of external trade to GDP growth, which helped shed about 0.7 percentage points of 2019 GDP growth, should diminish after that, as import demand from Argentina and China stabilizes.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more