Brazil: A monetary policy test for the BRL

- 16 June 2020

- Brazil

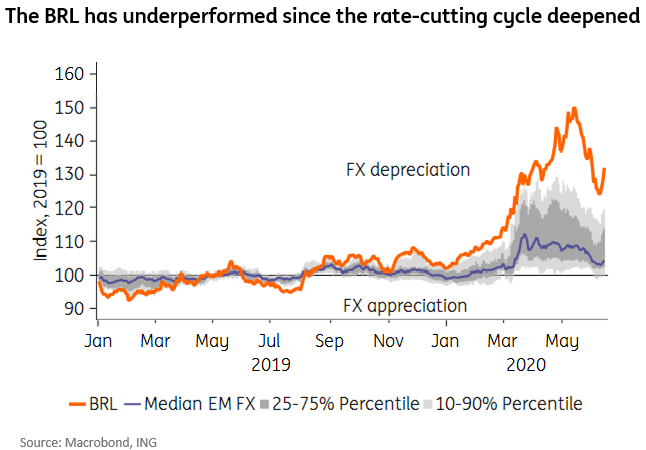

The BRL’s substantial underperformance over the past year can be traced to the structural break represented by the extraordinary drop in interest rates seen in Brazil over this period. For the Real to find a stronger footing, the central bank would have to signal, at tomorrow’s policy meeting, that scope for additional cuts is closed, or very nearly so

Another, possibly the last, rate cut

The Brazilian central bank (BACEN) meets this week, and market consensus calls for the bank to implement an additional 75bp rate cut, bringing the SELIC policy rate to a record-low of 2.25%.

The chief disagreement among analysts refers to the guidance BACEN will adopt. Bank officials have already signaled, at their last meeting, that this would be the last rate cut of the cycle. But market consensus appears to incorporate a slightly less hawkish guidance.

In our view, the market is pricing a scenario in which bank officials downplay the need for additional rate cuts, but do not close the door completely, for additional easing. The guidance would suggest that, should market conditions change materially, the bank would not rule out cutting the reference rate a bit further.

Nearing the “lower bound” for the SELIC rate

How much additional room BACEN would have to cut the policy rate is also a major source of debate, inside and outside the central bank. The consensus appears to be that the “technical minimum”, or the “lower bound” for the SELIC rate in Brazil is now at or above 1.5%.

In that case, for a majority of analysts, BACEN would have at most 75bp in additional scope to lower the policy rate beyond 2.25%.

But it appears that for some central bank official, and for many analysts, rate cuts beyond 2.25% would already pose some risks. The concern is that a policy rate of 2% (or less) would destabilize FX markets as it could create, under certain market conditions, arbitrage opportunities that would sharply increase demand for USDs.

A more hawkish guidance would add material support for the BRL

The best scenario for the Brazilian BRL, and our preferred outcome for this week’s meeting would be for the central bank to surprise by sending a more forceful hawkish message, signaling that room for additional drops in the policy rate has been exhausted.

But we agree with the consensus view that, given the heightened uncertainties and the deeply recessionary outlook for the domestic economy in the nearer term, the most likely outcome is for BACEN to signal caution, but not close the door to further rate cuts.

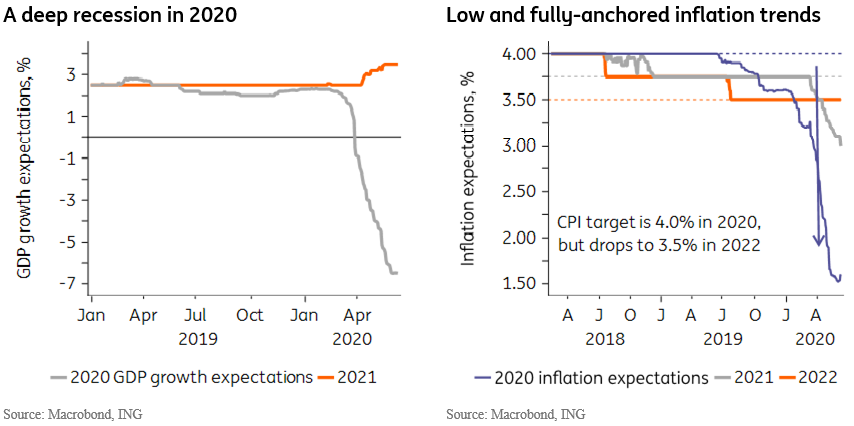

As seen in the charts below, consensus estimates for GDP growth have deteriorated sharply in recent weeks, and now suggest a 6.5% drop in GDP in 2020, while inflation forecasts remain deeply below target for the foreseeable future, trending near 1.5% in 2020, a record-low, and 3% next year.

Drop in interest rates represent a structural break for FX dynamics

Despite the rally seen in the past month, the Brazilian Real remains one of the worst-performing currencies across emerging markets.

In our view, the dramatic drop in interest rates, which intensified following the approval of the social security reform in mid-2019, is the single more important driver for the deep adjustment seen in the BRL over the past year.

Brazil has, finally, over the past year, transitioned to a monetary policy framework that accommodates more “normal” levels of interest rates. This transition was long-in-the-making and, to a large degree, reflects the recovery of the central bank’s credibility since Ilan Goldfajn took over as central bank governor, in 2016, and those credibility gains have solidified with Roberto Campos now at the helm of the institution.

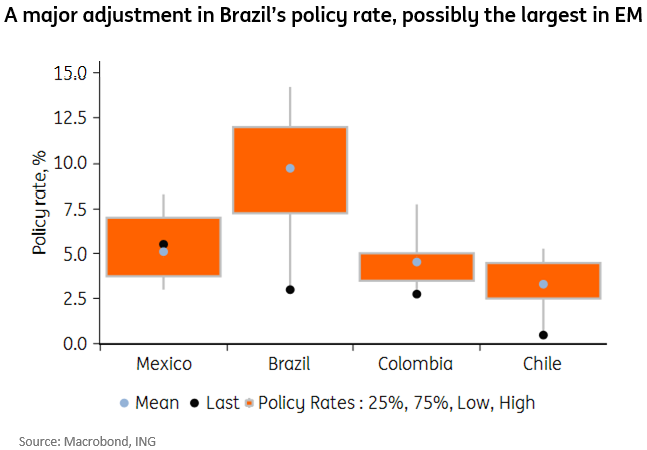

The SELIC rate should drop from an average of 10% in the past 10 years, to near 2% in the next year, while long-term expectations have fallen towards 5%.

And, if we are right, considering the consensus view that the SELIC rate should not return to the levels prevailing in the past, the BRL is also unlikely to rally to levels prevailing in the past.

The new-normal for the SELIC rate is roughly aligned with the normal for interest rates in most EM markets, i.e. Brazilian rates should no longer be an outlier, as it was in the past. As a result, the yield-advantage that the BRL offered in the past is, likewise, behind us.

In that case, the BRL must also adjust to this new interest rate reality, which suggests to us that FX modeling exercises that tend to compare current BRL levels to historical levels would likely overestimate the degree to which the currency is undervalued.

The BRL is likely not as undervalued as some think

We agree that at current levels of more than 5.0, the USD/BRL is probably too high. But the fair value for the pair is, also, probably no longer below 4.0. Under current circumstances and, specifically, under the assumption that fiscal policy in Brazil will be tight in the foreseeable future, the SELIC rate is unlikely to rise anywhere close to historical averages in the next few years.

A deep fiscal tightening is a requirement of the existing fiscal framework, namely the fiscal spending ceiling, and keeping this framework in place has become especially pertinent now, considering the deep deterioration in fiscal accounts that will take place this year as a result of the Covid-19 relief effort.

Fiscal policy assumptions may change over time, and that would be a crucial driver for monetary policy in the coming quarters. For now, our assumption is that even though Congress is likely to be subject to frequent pressures to weaken the spending ceiling, those efforts would, ultimately, be rejected.

As a result, our base-case scenario is that monetary policy stimulus is likely to prevail in the coming years. The eventual rise in the SELIC rate towards levels closer to “neutral” should happen very gradually, and may not start until 2022.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more