Belgium: The abnormal cycle

- 15 March 2021

- Belgium

From an economic point of view, the Covid crisis is unlike any other. It has been very deep in terms of activity, but the labour market has shown great resilience. Despite some delayed effects on bankruptcies and employment, the conditions seem to be right for the economy to begin its recovery

Uneven negative shock

With a slight decline in activity in the fourth quarter (-0.1%), it can be said that the Belgian economy has limited the economic damage despite the strong second wave of the pandemic. In the end, the Belgian GDP contracted by 6.2% in 2020.

On the demand side, household consumption paid the heaviest price for the crisis. At the end of last year, it was almost 10% below its pre-crisis level. The other components of demand are lagging less far behind. It is particularly noteworthy that after a strong rebound of 20% in the third quarter, productive investment continued its recovery in the fourth quarter (+4.6%), so that by the end of 2020, it only lags 3.6% behind its pre-crisis level. This makes the Covid crisis an atypical one: in a normal cycle, household consumption tends to resist rather well whereas business investment is one of the main drivers of any recession.

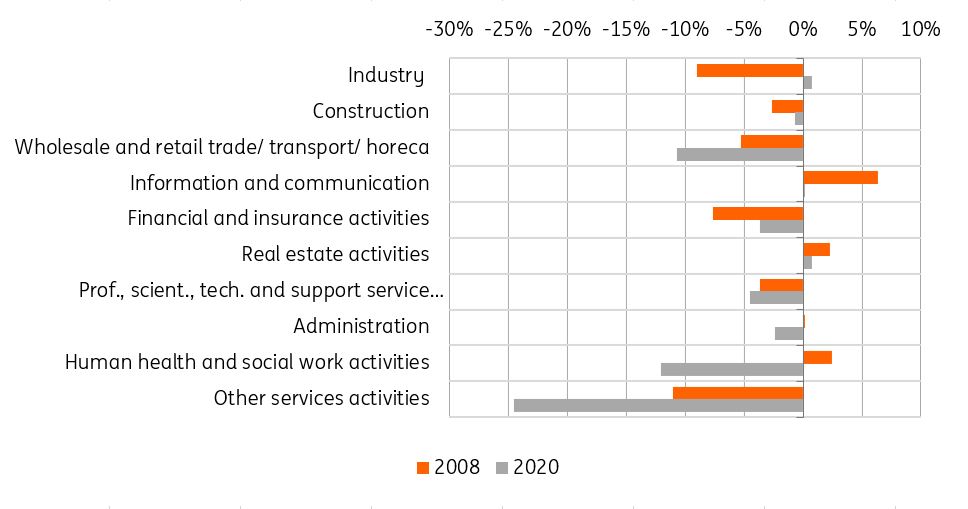

This specificity of the current crisis can obviously be found on the supply side. Four quarters after the peak of the cycle, the loss of activity due to the Covid crisis is still greater than the loss suffered during the financial crisis (which at the time was considered the worst crisis in the post-war period). But the sectoral decomposition of that loss is contrasted. In fact, the contraction of activity in 2020 is particularly marked in trade, transport, hotels and restaurants (-10.7% in the last quarter of 2020 compared to the pre-crisis level) and in the "other services" sector, which include culture, leisure and events (-24.6% over the same period). The other sectors of the economy seem to have resisted better, with industry even finishing the year with 0.7% more activity than before the crisis.

Value added gain(+) or loss (-) four quarters after the beginning of the financial crisis (2008) and the Covid crisis (2020) (in % of the peak of the cycle)

Labor market resilience

The evolution of employment is equally remarkable. After having lost 50,000 jobs during the first and second quarters of last year, the labour market has regained jobs: more than 7,000 in the third and more than 20,000 in the fourth, mainly in the scientific, technical and administrative support professions (+11,600 jobs in Q4) and the healthcare sector (+6,500 jobs). In the latter case, it is most likely linked to the preparation for the vaccination campaign. Notwithstanding the employment support measures (including temporary unemployment), this labour market resilience is surprising and bodes well for the recovery. Since the beginning of the crisis, total employment has contracted by 22,000. But compared to the economic shock, this is a very small correction: following the historical relationship between economic activity and employment, the Belgian economy should already have lost nearly 75,000 jobs!

Delayed effects would be limited?

However, we should not be naive. The effects of the crisis has up to now been masked by support measures, but it is also highly likely that they will be felt with a delay, paradoxically when the economy starts to recover and when the support measures come to an end. Beyond the sanitary situation, the strength of the economic recovery in 2021 will therefore depend heavily on the capacity of the economy to maintain the resilience observed so far. There are indications that this may be the case. On the one hand, we have seen that some key sectors of the economy (industry, construction, etc.) have already returned to their pre-crisis levels. This proves that there is not a general lack of demand in the economy. Bankruptcies and job losses in these key sectors should be limited.

On the other hand, the relatively small decline in household income during the crisis (thanks to support measures and small job losses) and the accumulation of savings should accelerate the recovery of household consumption when the economy reopens. Therefore, even if the sectors directly related to household consumption are currently the most affected, the recovery in these sectors will be stronger than usual, thus limiting the lagged effects of the past crisis. To be sure, there will probably be more bankruptcies and job losses in these sectors, but this will not be commensurate with the past crisis. By way of comparison, if the cumulative loss of activity since the beginning of the crisis is three times the loss incurred during the financial crisis, we expect an impact in terms of bankruptcies to that of the financial crisis, not more.

Public finances challenge

If the labour market and household income have shown resilience during the crisis, it is obviously due to the fact that the governments has supported the largest share of the cost of the crisis. As a consequence, the public deficit reached 10% of GDP in 2020, and the debt ratio increased by 17 points. In 2021, the economic recovery should automatically bring more revenue to the government, while expenditure should logically decrease. That said, the public deficit should remain significant this year, around 5.5% of GDP, or even more depending on the support measures that will be maintained and the stimulus measures that will be decided upon. As long as the ECB acts to maintain a reasonable financing cost and as long as the safeguard clause is in force, the situation of public finances is not a real problem. The whole question is therefore how and when European budgetary rules will evolve again, and until when the ECB is ready to keep financing costs artificially low. It is clear that putting public finances back on a stable track is in the long run one of the greatest challenges for the Belgian economy.

The Belgian economy in a nutshell (% YoY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Quarterly: Still in lockdown blues

- This bundle contains 15 Articles