Banks take up gauntlet against climate risks

- 2 November 2021

- Financial Institutions

Reducing exposure to ESG risks and identifying and improving the taxonomy compliance of balance sheets will remain a high priority for banks in 2022, particularly as developments here could increasingly start to impact funding costs

Moving forward from E to S and G

The European banking sector will continue to have its work cut out next year as it strives to meet the sustainability disclosure requirements set by European law. These disclosures will give market participants more insight into the environmental and social efforts made by banks. The 'E' in ESG, in particular, will remain in the spotlight, as banks take their first steps towards reporting on the taxonomy compliance of their balance sheets. The supervisory climate stress test, to be conducted by the European Central Bank for individual banks in 2022, will give further information on the climate risks that European banks may be exposed to.

Proposals on an extension of the taxonomy are looming

Meanwhile, regulatory and supervisory developments will continue to move forward at full speed, providing banks with new opportunities and challenges. While the technical screening criteria for the remaining four of the taxonomy’s six environmental objectives have yet to be established, new proposals by the European Commission on an extension of the taxonomy are looming. These will ultimately give banks further guidance on how to inform market participants about their efforts to transition away from environmentally harmful activities, and instruction on social and corporate governance. However, these developments will also likely give rise to new reporting challenges, while banks are already struggling to prepare for disclosure requirements related to the current environmental taxonomy.

We believe that showing a commitment towards meeting ambitious ESG objectives will remain crucial for the banking sector from a reputational point of view, but also increasingly from a funding costs perspective.

Banks will take the first step towards reporting green asset ratios

As part of their non-financial disclosure requirements, European banks will have to publish a number of key performance indicators (KPI) giving insight into the environmental sustainability of their business operations. The most important KPI is the green asset ratio (GAR). This ratio measures the share of the credit institution’s taxonomy-aligned balance sheet exposure versus its total covered balance sheet exposure, which will initially exclude exposure to central governments, central banks and supranational issuers.

The key performance indicators measuring the taxonomy alignment of the banks will not have to be disclosed until 1 January 2024. However, from 1 January 2022 onwards, banks will have to start disclosing their exposure to taxonomy-eligible and taxonomy-non-eligible economic activities. Reporting a large proportion of taxonomy-eligible exposure means that the credit institution will have a broader base of exposure from which to measure its taxonomy alignment later on. As such, this could be seen as supportive towards the institution’s future green asset ratio disclosures.

Being taxonomy-eligible is not the same thing as being taxonomy-aligned

Taxonomy-eligible are activities which have been specified in the European Commission’s climate delegated act as most important in making a substantial contribution to the climate change mitigation and climate change adaptation objectives. The climate delegated act will be complemented by the environmental delegated act, setting the criteria for the other four environmental objectives over the course of next year.

Taxonomy-aligned are activities which not only make a substantial contribution to one of the taxonomy's six environmental objectives, i.e. that meet the technical screening criteria defined by the delegated acts, but also do no significant harm to any of the other five environmental objectives, while complying with the minimum safeguards.

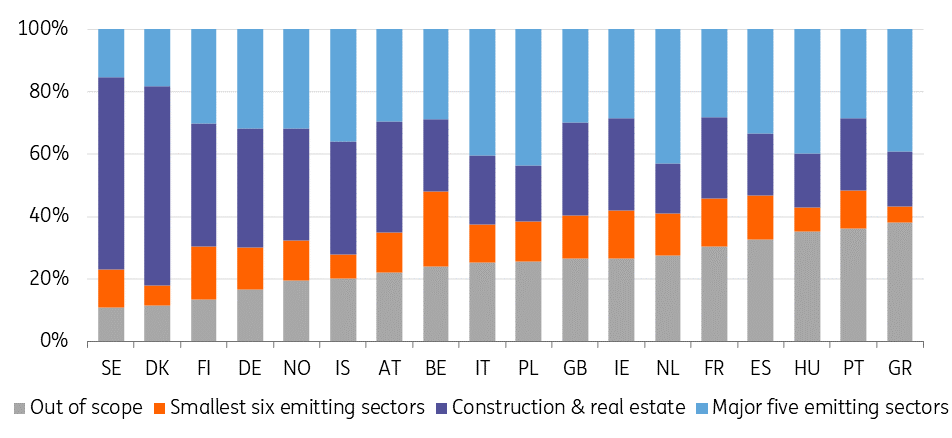

As an indication, in our report “Green asset ratios – What’s in store for banks?” we estimated that roughly 25% of the European banking sector’s loans and advances to non-financial corporations would not be taxonomy-eligible, as this exposure represents level 1 NACE activity which is not covered by the climate delegated act. Nordic banks would, on average, likely have the highest corporate loan exposure to taxonomy-eligible activity. In the report, we also found that Nordic banks tend to be less exposed to the more polluting activities covered by the climate delegated act, which will likely support their future green asset ratio disclosures.

Nordic banks have least exposure to corporate sectors that are out of the taxonomy scope

Disclosing meaningful taxonomy KPIs will take time

While at first, banks only have to disclose the proportion of taxonomy-eligible activities, some may already wish to publish preliminary green asset ratio estimates as a means of informing investors who are in the process of preparing their own taxonomy-related disclosures. These taxonomy-alignment indications will probably not be very high.

The EBA estimates that the aggregated green asset ratio for EU banks is only 7.9%

The EBA estimated earlier this year that the EU aggregated green asset ratio at this point would be as low as 7.9%. The European Central Bank recently came to a similar conclusion for the taxonomy alignment of European bond and equity market exposure. The central bank projects that only 1.3% of EU bond and equity markets are now financing activities aligned with the taxonomy for the objective of climate change mitigation, whereas around 15% of the market currently finances eligible activities.

Low taxonomy compliance numbers are not yet a realistic measure of environmental performance. An important reason is that banks are still in the process of obtaining all the required information allowing them to identify assets on their balance sheet that are taxonomy compliant. Besides, even within the group of activities that are covered by the climate delegated act some level of exposure may not initially count towards the green asset ratio. This includes, for instance, exposure to non-EU companies and SMEs, which for data availability reasons will probably be recognised in the numerator of the GAR only at a later stage as of 2025, subject to an impact assessment.

Coverage limitations, data availability and cautiousness on the side of the banks when reporting green asset ratios are reasons why it will possibly take a number of years before banks are able to report meaningful green asset ratios that properly reflect the environmental sustainability of their balance sheets. Meanwhile, the potential expansion of the taxonomy regulation will likely present banks with new disclosure challenges and/or opportunities in the years to come.

SFDR disclosures promote taxonomy compliance

The sustainable finance disclosures regulation (SFDR) requires financial market participants, such as asset managers or banks providing portfolio management services, to disclose whether their products (a) promote environmental or social characteristics (Article 8 products), (b) invest in an economic activity that contributes to an environmental or social objective (Article 9 products), or have neither one of these two purposes (Article 6 products). The EU taxonomy regulation introduced additional transparency requirements under the SFDR on the taxonomy alignment of Article 6, 8 and 9 products. While the SFDR’s level 1 disclosure provisions have already been applicable since 10 March 2021, the level 2 regulatory technical standards (RTS), including those on the taxonomy related disclosures, will likely become applicable per 1 July 2022, once adopted by the European Commission.

These disclosure requirements will make investors more demanding towards issuers regarding the information offered on the taxonomy compliance of their activities.

This also may have consequences for the (bond market) funding costs of financial and non-financial corporations. Bonds that are 100% taxonomy compliant will likely see the best investor demand, particularly if they are sold as EU green bonds under the future EU green bond regulation. Sustainable bonds that are not fully taxonomy compliant will also count towards the taxonomy KPIs of investors for the part that they do finance taxonomy compliant activities. The same holds for vanilla bonds, which will be able to count as taxonomy-aligned to the extent that the entity issuing the bonds is taxonomy compliant as disclosed under the NFRD. This alone will already form an incentive for banks to report solid green asset ratios.

Expanding the taxonomy: setting standards for environmentally harmful and social activities

By the end of this year, the European Commission will publish a report on the extension of the scope of the taxonomy regulation by:

- Economic activities that do not have a significant impact on environmental sustainability (NSI);

- Economic activities that significantly harm environmental sustainability (SH);

- Other sustainability objectives, such as social objectives.

In preparing its advice to the European Commission, the EU Platform on Sustainable Finance (PSF) presented two draft consultation reports on 12 July 2021, one discussing the ideas on a social taxonomy, and the other one discussing the possible extension of the taxonomy by activities significantly harmful to environmental sustainability and activities with no significant impact on environmental sustainability.

Significantly harmful versus no significant impact activities

An expansion of the taxonomy for significantly harmful and no significant impact activities will, in the opinion of the platform on sustainable finance, help improve clarity in financial markets regarding different environmental performance levels and different levels on environmental impact. As such, it will make efforts made by banks to support the transition of certain activities from a significant harm performance level to an immediate performance level (intermediate transition) more transparent. Under current regulation, only improvements towards the significant contribution level (green transition) show up in the form of higher green asset ratio disclosures.

The PSF proposals for integrating SH and NSI activities into the green taxonomy

The platform of sustainable finance proposes extending the current green taxonomy for activities that significantly harm (SH) environmental sustainability and economic activities that do not have a significant impact (NSI), by means of a matrix structure.

The rows in this structure represent three levels of the environmental performance of economic activity by means of a traffic light system:

- Significant contribution (SC) performance level (green): activities that meet the technical screening criteria for significant contribution to an environmental objective.

- Intermediate performance level (yellow): activities with environmental performance levels between the technical screening criteria for significant contribution and the do no significant harm level.

- Significant harm (SH) performance level (red): activities that do significant harm to the environmental objective and perform below the threshold set in the technical screening criteria for do no significant harm.

The columns in the matrix represent all activities in the real economy organised in four different boxes:

- Box 1: activities excluded from the green taxonomy as they are significantly harmful to one or more of the six environmental objectives, and are unable by their nature to transition.

- Box 2: prioritised activities under the climate delegated act for the climate change mitigation and climate change adaptation objectives of the green taxonomy.

- Box 3: activities to be included in the yet to be developed environmental delegated act for the other four environmental objectives identified in the green taxonomy.

- Box 4: activities that might be classified as not having a significant impact (NSI).

The platform on sustainable finance would prioritise the extension of the taxonomy regulation towards significantly harmful activities and recommends a rapid phasing in of an extended SH taxonomy, aiming at a first reporting by 2023.

However, the concept of a ‘valid transition’ away from the significant harm category would still stand or fall with the criteria to be defined to identify significantly harmful activities. The platform on sustainable finance proposes making the do no significant harm criteria fit for purpose to act as significant harm criteria. This could mean that based upon the criteria for doing no significant harm to the climate change mitigation objective, construction and real estate economic activities would then potentially be considered significantly harmful in the following cases:

- Buildings dedicated to the extraction, storage, transport or manufacture of fossil fuels;

- Buildings built before 31 December 2020 that are in the energy performance class (EPC) of D or lower, or as an alternative are not within the top 30% of the national or regional building stock expressed as operational primary energy demand (PED).

- Buildings built after 31 December 2020 and newly constructed buildings for which the primary energy demand (PED) setting out the energy performance of the building fails to meet the threshold set for nearly zero-energy buildings.

Reshaping do no significant harm provisions as criteria for significantly harmful activities may not always be easy

Any improvement in the energy performance of a building from a G to D category would, in this case, not be seen as a valid transition as the building would still remain in the significant harmful space. Alternatively, setting the cut-off towards the intermediate performance level at 30% best in class, would leave quite a substantial part of the building stock being classified as significantly harmful. The 30% is also a fixed percentage, meaning that a transition of one building to the top 30% will in parallel see another building migrate to the 70% worst performing category. This shows that making the DNSH criteria fit for purpose to act as SH criteria may not always be simple.

Social taxonomy has the purpose of directing capital to socially sustainable activities

Shaping a social taxonomy, including the related technical screening criteria and do no significant harm provisions, will also be high on the agenda of regulators in the coming year. However, key to the impact of the social taxonomy will be how it is integrated within the environmental taxonomy. The platform on sustainable finance discusses the implications of two options in more detail. Both take a separate social and environmental taxonomy as the basis, with governance safeguards binding to both taxonomies.

Taxonomy compliance will be impacted by the way the social taxonomy is introduced next to the environmental taxonomy

The link between the social and environmental criteria can then be introduced in different ways. 1. Environmental minimum safeguards can be added to the social taxonomy comparable to the minimum social safeguards complementing the environmental taxonomy. 2. Environmental and/or socially-sustainable activities would have to meet all the relevant environmental and social do no significant harm criteria (leaving no need for separate minimum safeguards). In both situations, companies would report separately on their social and environmental taxonomy alignment. However, the platform on sustainable finance recognises that the second option would probably leave fewer activities compliant with the social or environmental taxonomy as they would have to meet the complete set of do no significant harm criteria for both social and environmental objectives. Such an approach could therefore result in lower reported KPIs on taxonomy alignment, and fewer assets being linked to taxonomy compliant activities for the purpose of sustainable bond issuance.

The potential dimensions to a social taxonomy

Where it comes to the development of a social taxonomy, the platform on sustainable finance proposes a two dimensional approach. The vertical objectives will focus on improving a) the accessibility of products and services for basic human needs (e.g. water, food, housing, healthcare or education) and b) the accessibility to basic economic infrastructure (e.g. transport, telecommunication, electricity, financial inclusion or waste management). The horizontal objectives will focus more on the entity level processes promoting positive impacts and avoiding negative impacts on affected stakeholder groups, for instance by a) ensuring decent work (impact on workers), b) promoting consumer interests (impact on consumers) and c) enabling inclusive and sustainable communities (impact on communities). Governance will be addressed separately, as a distinct pillar to a social and environmental taxonomy, and covers a) good sustainable corporate governance and b) transparent and economic tax planning.

Climate stress testing to support a greening of bank balance sheets

The economy-wide climate stress test results, published by the ECB in September, mark the beginning of the central bank’s roadmap towards a climate stress-testing framework. This stress test will be followed by a separate supervisory climate stress test for individual banks in 2022, which should form the basis of an introduction to more regular climate stress-testing of banks in 2023-2024. The ECB sees climate change as a major source of systemic risk, particularly for banks that are highly exposed to economic sectors and/or geographical areas facing high physical or transition risk. Physical risks, such as wildfires in particular, are seen as the most important risk to banks if no action is taken. The central bank anticipates southern European countries will suffer the most from wildfires as a consequence of climate change, exposing the banks located in these countries to high physical risk if climate change is not mitigated. We believe the ECB’s climate stress testing framework will form an increasingly important additional incentive for banks to green their balance sheets in the years to come, particularly once these climate risks also become clearer on an entity level.

The ECB’s climate roadmap will support a further greening of bank balance sheets

The development of the climate stress testing framework for banks is just one of the ambitions the ECB has set in its climate roadmap for the coming years. By mid-2022, the central bank also intends to complete a review of its collateral valuation and risk control framework for climate change risks. The ECB is contemplating the introduction of disclosure requirements for private sector assets as a new diversifying eligibility criterion to the collateral and asset purchase treatment of these assets. These requirements are expected to become applicable in 2024 and will take into account the EU regulatory disclosure initiatives. The plans may encompass the first steps towards a more favourable haircut treatment and a stronger asset purchase focus for assets that, based on the sustainability key performance indicators (KPIs) to be disclosed, are considered to have lower climate risks. The changes to be made to the collateral framework could, in our view, contribute to a shift in demand from banks towards debt instruments less exposed to climate risks.

Draft Basel-III reform proposals recognise the urgency of climate risks

That the recognition of ESG risks continues to gain firmer footing in bank regulation was also underscored by the draft Basel-III reform proposals published on 27 October 2021. CRR Article 449a already requires large institutions with securities traded on a regulated EU market to disclose, as of June 2022, information on ESG risks, including physical risks and transition risks. The European Commission’s amendment proposals to the CRR now suggest expanding this requirement to institutions in general, including non-complex institutions, with an annual reporting obligation for non-complex institutions and a semi-annual one for the other institutions. The draft Basel-III reform proposals also introduce harmonised definitions on different types of ESG risk, such as environmental risks, physical risks, transition risks, social risks and governance risks.

By June 2023, the EBA will advise on a differentiating risk weight treatment for high climate risk exposures

However, the most important ESG takeaway from the draft Basel-III reform proposals is, in our view, the suggestion to bring forward by two years the EBA’s mandate to assess the justification for a dedicated prudential treatment of assets exposed to ESG risks. The EBA has to formulate an opinion by 28 June 2023 on whether, for instance, assets with particularly high exposure to climate risk, such as assets in the fossil fuel sector and high climate impact sectors, should be subjected to a different risk weight treatment. The potential future introduction of a less favourable risk weight treatment for exposure to more polluting sectors may at some point form a further incentive for banks to reduce this exposure or to attach a different price to them.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Bank sector outlook 2022: Bracing for transformation

- This bundle contains 6 Articles