Banks put the squeeze on US economy as lending conditions tighten further

- 31 July 2023

- United States

The Federal Reserve's Senior Loan Officer Opinion Survey shows banks are being increasingly restrictive in their lending practices while households and businesses are wary of taking on additional borrowing. Given how important credit flow is to the US economy it boosts the chances of a slowdown that will bring inflation back to target

Banks tighten lending conditions across the board

The Federal Reserve’s efforts to bring inflation under control appear to be bearing fruit based on recent core inflation prints coming in at 0.2% month-on-month, although the US remains some way off from the 2% year-on-year target. The Fed has hiked the policy interest rate 525bp and embarked on quantitative tightening, but access to credit is just as important as the cost of credit in taking heat out of the economy. Today’s Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) underscores how the tightening of lending conditions will continue to put the brakes on activity and contribute to inflation sustainably returning to target. The concern is that it will also heighten the chances of recession.

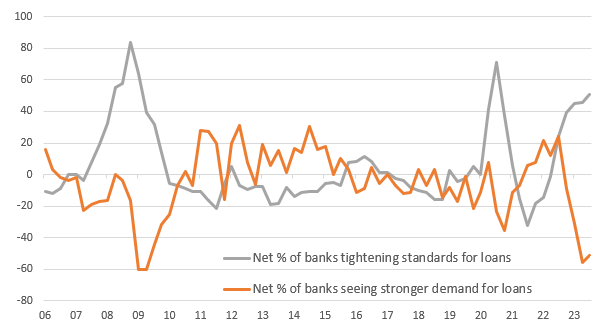

Tighter lending standards point to credit contraction

Demand for loans falls further

Lending conditions started tightening sharply in the third quarter of 2022 and that continued in subsequent quarters as concern about potential loan losses in a weaker economic environment led banks to become more wary about who they lend to, how much they lend and the terms on what they lend. This then accelerated in the wake of the failures at Signature Bank, Silicon Valley Bank and Credit Suisse’s enforced sale to UBS. Today’s report shows banks have tightened lending conditions even further for all forms of borrowing through the second quarter and into the third while demand for loans have deteriorated as well.

Net % of banks tightening lending standards and net % of banks seeing rising demand for corporate loans

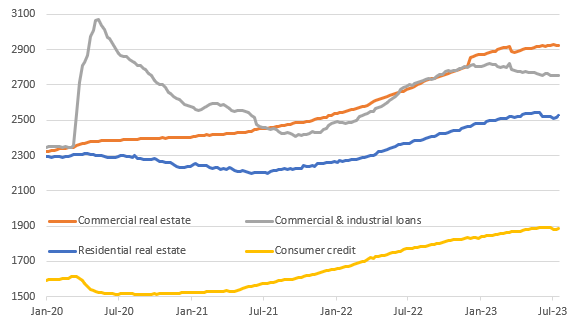

Outstanding bank lending is already dropping

With banks remaining risk averse in their lending and business and households reluctant to borrow, the risk is that credit contracts in coming quarters as our first charts suggests. Given the importance of credit flow to the US economy, this means we cannot dismiss the possibility of a US recession despite the market’s relaxed mindset right now.

The Federal Reserve’s high frequency weekly data shows lending has fallen in six out of the past 18 weeks since the small banking stresses came to the fore in March. Those down weeks have been larger in volume than the up weeks with outstanding lending at $10.09tn as of last week versus $10.13tn the week of 13 March.

The chart below shows the composition of the outstanding lending with commercial real estate out in front, but plateauing at $2.92tn with residential real estate lending topping out at $2.56tn while even consumer credit is seemingly stalling at just under $1.9tn. The concern is that commercial and industrial lending has been trending downwards, which suggests a declining appetite to put money to work and invest in business growth.

Outstanding stock of commercial bank lending by sector ($bn)

Credit squeeze heightens the chances of a sharper slowdown

When asked about what banks will be doing to their lending standards and what they expect in terms of loan demand the SLOOS survey concluded “Regarding banks' outlook for the second half of 2023, banks reported expecting to further tighten standards on all loan categories. Banks most frequently cited a less favorable or more uncertain economic outlook and expected deterioration in collateral values and the credit quality of loans as reasons for expecting to tighten lending standards further over the remainder of 2023”.

As such, we are somewhat sceptical of the markets current viewpoint that the US economy can avoid recession via a 'soft landing'. Although borrowing costs are relatively high, it isn’t the last 25bp rate hike that turns struggling businesses into failing businesses. It’s when a company has a couple of orders cancel on them and the business goes to its local bank and asks for a line of credit to see them through, but the bank says “no”. We run a much higher risk of this happening when lending conditions are as tight as signaled by the SLOOS report.

Big businesses have little issue given the competition amongst global banks with strong balance sheets who are still keen to lend to robust companies. It is the small and medium sized firms where pain is more likely to be felt. Small and regional banks do the bulk of this lending and in the wake of Silicon Valley Bank/Signature etc they have had to cope with deposit flight, the prospect of greater regulatory oversight and higher capital commitments and a fear factor in boardrooms that naturally comes when competitors collapse.

But it will also dampen inflation and offer the Fed room to cuts rates in 2024

This report makes it all the more likely that the Fed will not need to hike interest rates further since tighter lending conditions and reduced loan demand point to further credit contraction will naturally take heat out of the economy. Markets are currently pricing around 5bp of tightening for the September FOMC meeting and a cumulative 9bp by the November FOMC meeting, so less than a 40% chance of any further rate hikes from the Federal Reserve. This looks sensible to us while we continue to see a strong chance the Fed will reverse course and start cutting interest rates from March next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more