Bank Pulse: December eurozone bank lending to business more than triples

- 28 January 2022

- Financial Institutions

While bank lending to households declined gently in December, net bank lending to businesses tripled compared to November. Banks probably wanted to make sure they’d qualify for favourable rates on their TLTRO borrowing

TLTRO-driven spike in bank lending

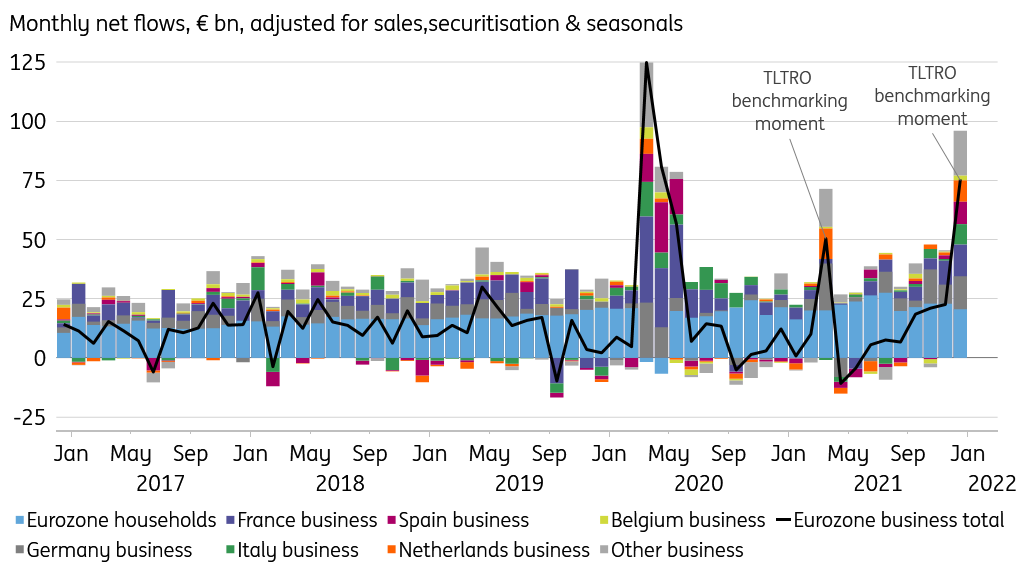

The December ECB monetary figures show an interesting spike. Monthly net bank lending to eurozone business jumped from €23bn in November (seasonally adjusted) to a whopping €75bn in December. It may be tempting to read this as a signal of economic growth picking up. Yet this is not mirrored in other indicators and another explanation is more compelling.

December marks the end of the ECB’s “additional special reference period”. If banks managed to keep their business lending portfolio (plus non-mortgage lending to households) at least constant between October 2020 and December 2021, they qualify for a favourable -100bp rate on funds borrowed under the ECB’s Targeted Longer-Term Refinancing Operations (TLTROs), between June 2021 and June this year. If banks did not clear this hurdle, the rate turns out less favourable, following a complex calculation, but let’s simplify to say it will drop to -50bp during this period. The benchmark performance also affects the TLTRO rate after June this year.

With €2.2tr of TLTRO funds outstanding, eurozone banks have some €11bn of negative interest rate revenues at stake for the June 2021 - June 2022 period only. This provided a strong incentive to make sure they cleared the benchmark hurdle set in December. The chart below shows a similar lending spike in March 2021, when the previous TLTRO benchmark period expired.

Eurozone bank lending to households and non-financial businesses

Though we don’t have individual bank data, country-level data suggests that most banks will have succeeded. Spain was most at risk, trending below the benchmark until November. But Spanish banks lent some €9bn in December, taking them above their benchmark. So we tentatively conclude from this that most eurozone banks will have qualified for the favourable -100bp TLTRO rate in the June ’21 – June ’22 period.

The ECB's negative rate incentive framework is set to change substantially in June

This also means we don’t expect a lot of TLTRO repayments at the end of March. TLTRO repayments in June are a different story and will depend on any changes to the complex negative rate incentive structure the ECB may announce in the months ahead. In particular, we expect the ECB to increase the tiering multiplier determining the exemption of the negative deposit facility rate banks face when parking reserves at the ECB.

The ECB effectively pre-announced a review of the two-tier reserve remuneration in December. The problem there remains that any change to the multiplier does not address the skewed distribution of reserves across Europe; while TLTRO funds are borrowed everywhere, the reserves that are created in the process still gravitate towards northern eurozone banks, putting most of the negative rate burden on them.

Household borrowing and deposit growth remain on a decelerating trend

Returning to the December monetary data, lending to households (which mostly consists of mortgages that are not relevant to the TLTRO benchmark) continued its gently decelerating trend. Back in July, net monthly household borrowing exceeded €25bn for the first time since September 2007. December net borrowing stood at €20.6bn. The deceleration in net borrowing coincides with the bottoming out of household rates. We expect rates to rise this year, and consequently household borrowing is likely to decelerate further.

December net growth of bank deposits continued its decelerating trend, at least for households. Business deposits saw an uptick that is, however, directly linked to the lending surge and unlikely to persist.

The December spike in bank lending to business is likely a one-off driven by banks making sure to clear the TLTRO benchmark hurdle. The precedent in March ’21 suggests that this spike has front-loaded some borrowing demand, suggesting lending performance will be weak in the first months of 2022. Any such dip should not be misread as signalling economic weakness, just as the December spike does not reflect extraordinary economic strength.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more