Bank Outlook 2023: The make-or-break year for digital currencies

- 1 November 2022

- Financial Institutions

Financial institutions and supervisors will be preparing for the crypto and stablecoin regulatory framework next year; it comes into force in 2024. The Eurosystem will also start work on a digital euro payment scheme rulebook, which will assume importance beyond any central bank-issued digital currency

Decrypting the markets in crypto-assets regulation

Just a few weeks ago, the European Council (consisting of EU national government representatives), Parliament and Commission agreed on the “Markets in Crypto-Assets Regulation” (MiCAR). This crypto framework regulates both the issuance of cryptocurrencies and assets, and transactions, e.g. trading, investment and payments. A few things to consider:

- While MiCAR has now been agreed upon at a political level, it is expected to take until 2024 before it actually enters into force. In the meantime, details of regulation have to be worked out in technical standards, and supervisors have to prepare themselves. That said, MiCAR already changes the conversation between financial institutions and supervisors today, as the contours of the future regulatory framework are now clear. This might convince some European banks to press ahead with crypto-related services and experiments ahead of MiCAR actually coming into force, probably in 2024.

- The arrival of MiCAR is certainly positive for the coming of age of the crypto sector, and for banks’ possibilities to engage with crypto. At the same time, any engagement in crypto, by banks or otherwise, is hampered by the fact that a lot of crypto activities are not covered by MiCAR. This applies for example to “decentralised finance” (DeFi), the attempt to replicate financial services on a blockchain infrastructure, without traditional intermediaries. DeFi may have looked and behaved a bit like a casino so far, but it has potentially promising applications as an additional financing channel next to the bank and market finance channels available today. But proper DeFi regulation will have to wait until MiCAR v2.0.

- While attempts were made in the European Parliament to restrict the energy-intensive “Proof of Work” transaction validation mechanism (used by e.g. bitcoin), MiCAR in its final form does not contain any restrictions, but only sustainability disclosure requirements. Meanwhile, the world’s second most important blockchain Ethereum has switched to PoS, a much less energy-hungry mechanism. As a result, developing services around Ethereum will save financial institutions from difficult discussions with policymakers, regulators and the wider public, compared to Bitcoin-related services.

- Insofar as the provision of crypto services by banks would involve taking them onto balance sheets, the prudential treatment matters. This is not part of MiCAR, but is currently under consideration by the Basel Committee for Banking Supervision. The direction of travel is that tokenised traditional assets and selected, really stable, stablecoins would fall under existing prudential rules, though with an additional charge for “infrastructure risk”. But most crypto assets, given their risks and volatility, would in essence need to be backed one-on-one with capital. This would make it very costly to hold such assets. Moreover, the Committee has proposed that crypto assets' total exposure should be limited to 1% of capital.

From a regulatory perspective, the approval of MiCAR means the clearance of an important hurdle. Prudential treatment of crypto has not yet been codified, but the thinking in Basel provides guidance to supervisors. Meanwhile, the “crypto winter” which set in this year may have made the business case to engage in crypto less obvious. Yet some financial institutions may look through current price developments and instead consider the long-term possibilities of crypto and decentralised finance.

MiCAR birds-eye view

A birds-eye view of the markets in crypto assets regulation

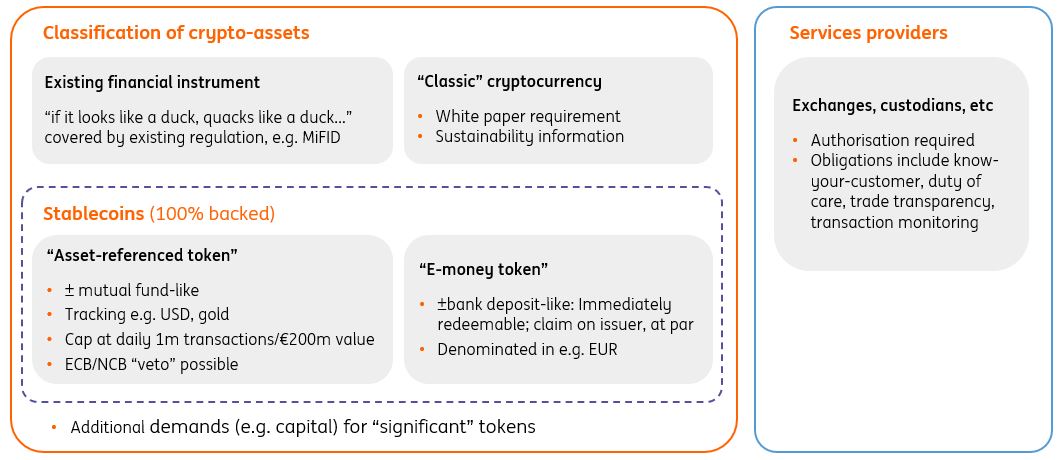

- MiCAR intends to supplement existing financial services regulation. This means for example that if tokens issued on a “distributed ledger” (a blockchain) have the characteristics of a security, then MiFID and other securities' regulations will apply. MiCAR only comes into view when tokens are not covered by existing regulation. For plain vanilla cryptocurrencies, the most important requirement for issuers is to provide a white paper, which has to contain specific information for investors. The white paper requirement parallels the requirement for securities issuers to provide a prospectus.

- So-called “stablecoins”, given their promise of stability, face additional requirements. Stablecoins not denominated in euro (or another EU currency) typically classify as asset-referenced tokens (ARTs). Their regulation somewhat resembles mutual fund regulation. Importantly, ARTs face volume and transaction limits, and central banks may refuse authorisation if an ART poses risks “to monetary policy transmission, monetary sovereignty, the smooth operation of payment systems, and financial stability”.

- Stablecoins denominated in euro (or another EU currency) typically classify as an e-money token (EMT). From a prudential perspective (though not a business conduct or anti-money laundering perspective!), they are treated mostly like bank deposits. In particular, users have a claim on the issuer (unlike with ARTs or ordinary cryptocurrencies).

- An authorisation regime will apply to crypto asset service providers, including exchanges and custodians. In addition to already existing requirements regarding anti-money laundering, their duty of care is spelt out in MiCAR, as well as requirements regarding things 'know-your-customer' and trade transparency.

- But it’s also important to consider what is not covered by MiCAR. The problem that supervision tends to focus on (legal) entities, and does not fit truly decentralised tokens, protocols and platforms, has not been solved. In practice, the responsibility and liability is placed with crypto asset service providers to make sure that the tokens they list are compliant. If users interact with truly decentralised tokens directly, they venture outside regulated space. In practice, the impact of the problem is diminished by the fact that only a small portion of tokens and platforms which claim to be decentralised, truly are.

- Also out of scope are non-fungible tokens and decentralised finance (“DeFi”). The latter may prove problematic if and when DeFi space develops lending, borrowing and insurance beyond the crypto investment and speculation applications it is currently mostly confined to.

Given the fast-developing crypto sector, the European Commission needs to conduct an interim review within two years, which will likely result in recommendations to expand MiCAR to (parts of) DeFi and NFTs.

Building the digital euro

The crypto winter has done little to curb central banks’ enthusiasm for digital currencies, at least insofar as those issued by themselves. 2023 is promising to become another busy year for the “digital euro”, the ECB’s retail-oriented CBDC project. The ECB realises that to make the digital euro a success, they have to look beyond issuing. A common eurozone or EU-wide digital method of paying is needed. The tried and tested way to realise such a method in the world of payments is to agree on a scheme with a common rulebook to ensure compatibility among all payment processors and other participants. The ECB intends to start work to develop this rulebook in early 2023. In our view, such a scheme rulebook can make or break the digital euro, as it determines the ease of adoption and the innovations that can be built on top of it. The rulebook might also be useful beyond central bank digital currencies if it allows the processing of payments with commercial bank money or stablecoins.

Meanwhile, the European Commission will publish its proposal for a digital euro legal framework in the first half of 2023 as well. The ECB’s digital euro investigation phase ends in Autumn 2023, after which the ECB Governing Council decides whether to start the “realisation phase”. Any actual launch is not expected before 2026.

The digital euro’s stated goals – do they make sense?

While the digital euro slowly takes shape, the policy goals it is supposed to serve remain elusive. Judging from central bank reports and speeches over the years, the goals have changed a few times. Most of these goals indeed refer to concerns that would be good to address. What is less clear, however, is whether issuing a digital euro is necessarily the best or only answer. Other policy responses or private sector initiatives might yield the same or better outcomes, and in some cases the introduction of a digital euro, if not managed carefully, could even promote an outcome that policymakers sought to avoid in the first place:

| Digital euro justification | Assessment |

|---|---|

|

Monetary anchor needed: maintain public access to and full usability of central bank money in a digital world |

Is such an anchor really needed? The ECB Kantar study published in Spring 2022 struggled with the fact that people don’t realise, understand or care about difference- commercial vs central bank-issued money |

| Not Libra! Avoid dominance of non-euro, privately issued, stablecoin |

Non-euro stablecoin will be regulated by MiCAR, including a broadly formulated veto for the ECB. Moreover, BigTechs derive their advantage not so much from issuing their own currency, but from providing a seamless payment experience |

| Reduce foreign dependence in payments | Existing card schemes can easily add a digital euro to their offering. To reduce foreign dependence, a European digital payment scheme would be the first step |

| Support innovation | Innovation takes place in payment infrastructure, not in the underlying currency itself |

| Have a response ready to a foreign CBDC | A retail-oriented CBDC cannot be the answer to global trading and financial markets. Instead, this calls for a wholesale/cross-currency solution |

Banks would be well advised to follow developments closely in 2023, to prepare and identify pitfalls and opportunities. Banks may not be obliged to offer digital euro services, but their retail clients will surely expect them to be on offer from day one, including onboarding, transaction monitoring and likely instant “overflow” facilities, where any incoming digital euro that takes holdings above a certain ceiling, are automatically redirected to the client’s commercial bank account. The digital euro may also offer new opportunities for banks, both in their retail and wholesale services offering. The time and resources that banks and other intermediaries need to spend to prepare for all of that, should not be underestimated.

Commercial bank alternatives to the digital euro

As indicated in the box above, the digital euro is not the only, and not necessarily the best answer to all concerns identified by policymakers. One area where commercial banks could play a role is in the issuance of tokenised bank deposits or euro stablecoins. Their potential applications overlap to some extent with central bank-issued digital currency.

In crypto markets, dollar-based stablecoins have played an important role for several years. While euro stablecoins are available, they have not been issued yet by established EU-regulated institutions and so far only play a marginal role. The ECB has indicated that “version 1.0” of the digital euro will not be built on, or directly interoperable with, blockchain. If indeed DLT compatibility is postponed to “version 2.0”, this can realistically not be expected before 2030. This leaves the field open for private sector initiatives. A euro-denominated stablecoin or tokenised bank deposit could play a prominent role in EU crypto markets and help to unlock future-use cases. It could provide a boost for decentralised finance to develop into a more mature funding channel for the real economy..

While stablecoins and tokenised bank deposits can both be issued by banks, they are very different currencies. A tokenised bank deposit is generally taken to be commercial bank money residing on a blockchain/distributed ledger infrastructure. While the technology is different, from a regulatory perspective, it is likely to be be in scope of existing prudential regulation, and be treated like just another bank deposit. This means that the tokenised bank deposit can only be held by clients known to the bank. Also, a tokenised bank deposit is a liability of the bank, and as such is slightly more risky than central bank money. Retail holders will be covered by existing deposit guarantee schemes, so the distinction matters in particular for wholesale usage. Corporate and institutional users may want to limit their exposure to single banks.

A stablecoin, properly issued and regulated, is fundamentally different from a tokenised bank deposit in at least two aspects.

- It is a bearer instrument. In contrast to bank deposits, tokenised or otherwise, the holder need not be known to the issuing bank. From a regulatory (MiCAR) perspective, client onboarding and transaction monitoring are left to the stablecoin services provider (e.g. an exchange), which is not necessarily the same institution as the issuer.

- A stablecoin should be backed by specific safe assets. This implies central bank reserves and high quality liquid assets like sovereign bonds. Depending on the asset mix, the risk profile of a stablecoin is likely lower than that of a commercial bank deposit, and may approach that of central bank money. Again, this should not be a distinctive feature in a retail context, where deposit guarantee schemes provide more than enough coverage for day-to-day current account operations. It does matter in a wholesale context, however.

Tokenised bank deposits and stablecoins have different use cases and come with different regulatory obligations. The former could in principle be launched today, provided that supervisors agree to treat them like ordinary bank deposits. For the latter, the MiCAR framework won’t likely be in place until 2024. Still, that would give banks a headstart to central bank-issued digital currency, which in the eurozone won't launch before 2026 and is at that time likely still unavailable on blockchain.

2023 is going to be a year for banks to pay close attention to digital currencies and their regulatory framework. Important proposals will be launched and decisions will be taken. Moreover, supervisors will start to work out in more detail how crypto and stablecoin supervision should look in practice, while the digital euro payment rulebook should also start to take shape. As abstract concepts become more concrete, banks can also start to think in more detail about the roles they intend to play in the field of digital currencies.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Banks Outlook: The major challenges and opportunities for 2023

- This bundle contains 8 Articles