Bank of Thailand to signal end of its easing cycle

- 22 June 2020

- Thailand

The case for further monetary easing remains strong but there is not much easing space left for the Bank of Thailand. We consider the current easing cycle to be over

| 0.50% |

BoT policy rateNo change expected |

On hold policy rate at 0.50%

Thailand's central bank, the Bank of Thailand, holds its monetary policy meeting on Wednesday, 24 June. Three 25 basis point cuts so far this year have pushed the policy rate to an all-time low of 0.50%.

There is a solid consensus behind the view that the BoT will leave the policy rate unchanged this week; out of 24 analysts in the Bloomberg survey only three expect a further 25bp cut. We are in the ‘on hold’ camp.

Still strong case for rate cut

A significant dent to GDP growth and CPI inflation due to the Covid-19 pandemic and prospects for a weak recovery from this slump argue for continued policy stimulus. Although Thailand was relatively unscathed by the disease, with only 3,022 infections and 58 deaths so far, the greater dependence on trade and tourism, and perennially weak domestic demand make it the most economically vulnerable to the disease.

The disease spread is well under control, the infections curve is flat, and the movement restrictions have almost ended. But the complete economic fallout from the disease has yet to be realised. And with a prolonged slump in the key drivers of trade and tourism, the negative impact is likely to stretch well beyond the current quarter and through 2021.

At -3.4% year-on-year in May, CPI inflation is the lowest since the global financial crisis (GFC) in 2009. And with continued weak demand ahead, it won’t be turning positive anytime soon. GDP growth slipped into negative territory in 1Q20 with a 1.8% year-on-year fall. We anticipate an 8.3% YoY plunge in 2Q20, the worst performance since the Asian crisis in 1998. The negative growth trend will remain in place through the first quarter of 2021.

Expectations that the Covid-19 outbreak would dent exports and tourism led the Thai baht (THB) to depreciate earlier in the year. But not anymore. Despite increasingly weak fundamentals, the currency has returned to its former status as an emerging market outperformer since April and is the second-best currency in Asia after the Indonesian rupiah. The strong currency has reignited policymakers' concerns that it could potentially hinder the export and tourism recovery. More steps to encourage outward capital flows are under consideration though most such steps since last year have been in vain.

But not enough easing space

All these factors may strengthen the case for a further cut to the BoT policy rate this week. However, from where the policy rate sits currently, we don’t think the central bank would consider nudging it down further.

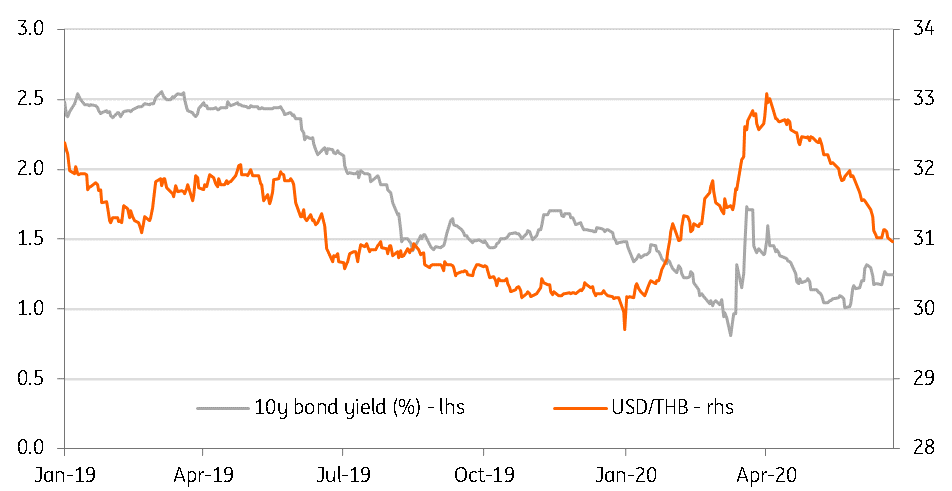

Supporting our view of a stable policy rate is a 20bp rise in the 10-year government bond yield over the last month. We also view the divide among policymakers over the latest 25bp cut on 20 May, with some favouring no change, as signalling the end of the easing cycle – the no change votes might have been in favour of saving some easing space for the future in the event of a second wave of the virus.

We think the BoT will argue that both growth and inflation may bottom out in the current quarter, with a reopening of the economy helping the recovery for the rest of the year. Another argument for keeping rates on hold would be the large fiscal stimulus being undertaken to facilitate the post-Covid-19 recovery.

With rate policy reaching its limits and the government on a borrowing spree to fund a huge fiscal stimulus, the idea of unconventional or quantitative easing (QE) may hold some ground, though we don’t see the BoT moving onto that path either in the near-term.

Thai baht vs. 10-year government bond yield

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 23 June 2020

- This bundle contains 5 Articles