Bank of England hikes rates again amid dire UK recession warnings

- 4 August 2022

- FX Rates United Kingdom

The Bank of England has hiked rates by 50 basis points while also now forecasting a recession lasting for five quarters. That shows just how worried it is that worker shortages and supply issues could keep inflation elevated even as the economy weakens. Another 50bp hike in September seems plausible

Bank hikes 50bp despite grim new forecasts

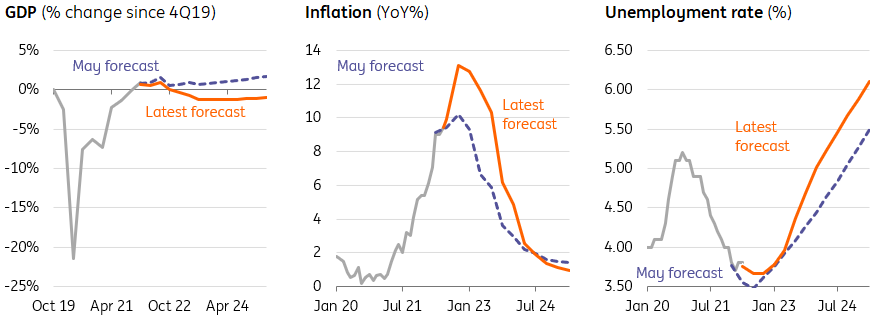

The Bank of England has stepped up the pace of its tightening cycle with its first 50 basis point (bp) rate hike, and has once again signalled a willingness to act ‘forcefully’ amid high inflation. What’s fascinating is that all of this comes alongside new forecasts, which show a recession lasting five quarters from late this year, the unemployment rate rising above 6% during 2025, and inflation well below target by then too. It expects the economy to shrink by more than 2% in total between Q3 and early 2024.

The fact that the Bank is stepping up the pace of rate hikes while also forecasting a meaningful recession shows just how worried it is that worker shortages and supply issues could keep inflation elevated even as the economy weakens.

In other words, it’s the supply side of the economy – much more so than what’s happening with demand – that will heavily determine when and after how many more hikes the BoE will stop tightening. The Bank will want to see signs that skill shortages are easing and that wage pressures are showing signs of abating. Its own ‘Decision Maker’ survey recently suggested that two-thirds of firms are still finding it ‘much harder’ than usual to find staff.

How the BoE's new forecasts compare to the May report

Given that only one official dissented on the decision, and the fact that the Bank reiterated its willingness to act ‘forcefully’ to curb inflation, we think there's a strong possibility of another 50bp hike in September – particularly if that’s what both the Fed and ECB end up doing too.

Still, look closely and there are hints that the Bank won’t need to go that much further than that before pressing pause on its tightening cycle. The BoE's new grim set of forecasts are premised on the Bank Rate peaking close to 3%, which is what markets currently expect. But the fact these projections show inflation well below target can be read as a hint that it won’t need to tighten as aggressively as investors think – even if officials also acknowledge that they're putting less weight on these projections than usual.

For now, we think the Bank’s next rate hike in September could be the last. The window for further hikes further appears to be closing, not least because outside of the jobs market, there are signs that some of the key inflation drivers may be starting to ease.

High-risk outright sales of gilts to start in September

The BoE plans to sell £10bn of gilts from its QE portfolio every quarter for the next 12 months, starting in September. This corresponds to a balance sheet reduction target of £80bn over the same period (the rest being ‘passive’ non-reinvestment of maturity proceeds). This plan puts the focus on the private market’s ability to absorb more sovereign debt. Assuming a reduction of £80bn per year, this means private investors will have to increase their exposure to gilts by the same amount, on top of regular deficit-financing. This is clearly a risk to our benign gilt yields view.

The second aspect of the BoE QT plan is active sales. Going back to our example above, if the QT target is 80bn per year and that, as is the case in FY 2023-24, passive reduction is only £36bn, this means that the remainder, £44bn, will be achieved via gilt sales. First, this is a non-negligible amount. For reference, the past 10 years have seen gross gilt sales of £171bn per year by the DMO. Secondly, we do not think current market conditions, judging by gilt bid-offer spreads and by rates implies volatility, make this a risk worth taking.

If market conditions improve, we expect sales to occur at the earliest in September, but we think it will take much longer to say with any degree of confidence that the market can accommodate this amount of gilt sales without posing risks to its functioning.

Current market conditions make gilt sales a riskier endeavour

FX: Sterling takes a dim view of events

Sterling has sold off about 0.5% since the rate announcement. There were no surprises in the size of the rate hike, nor the voting pattern, yet the BoE’s narrative of further forceful tightening even as the economy heads into recession is a tricky one for growth-sensitive sterling.

On the one hand, we think extreme inversion of the UK Gilt curve and a policy rate over 2% in September could actually help sterling from the bond side. Here foreign bond investors into Gilts will probably be cutting FX hedge ratios on their bond portfolios to avoid paying away more in hedging costs than they pick up in yield at the longer end of the curve..

Yet a central bank reluctantly tightening rates to address supply side shocks is not particularly positive for sterling. GBP/USD remains vulnerable to the strong dollar and a difficult risk environment, but aggressive BoE tightening and an equally dim view for European growth prospects suggests EUR/GBP may continue to trade in a 0.8350-0.8450 range over the coming weeks.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more