Bank of England set to cut rates before the Fed as officials turn dovish

The Bank of England is right to draw a distinction between the UK and US inflation outlook, and we expect the first rate cut to be in August or maybe even June. Sterling could come under greater pressure, but we think this is less of a concern for the BoE now than it was in 2022 or 2023

The Bank of England is turning dovish

The Bank of England is trying to tell us something, and markets are finally starting to take notice.

Bank of England Governor Andrew Bailey has hammered home the message that the UK’s inflation outlook is “rather different” to the US. That sentiment was echoed by Deputy Governor Dave Ramsden last week who said that the UK is “catching up fast” on disinflation, a significant intervention from one of the more hawkish members of the committee.

Investors now expect two rate cuts in the UK this year

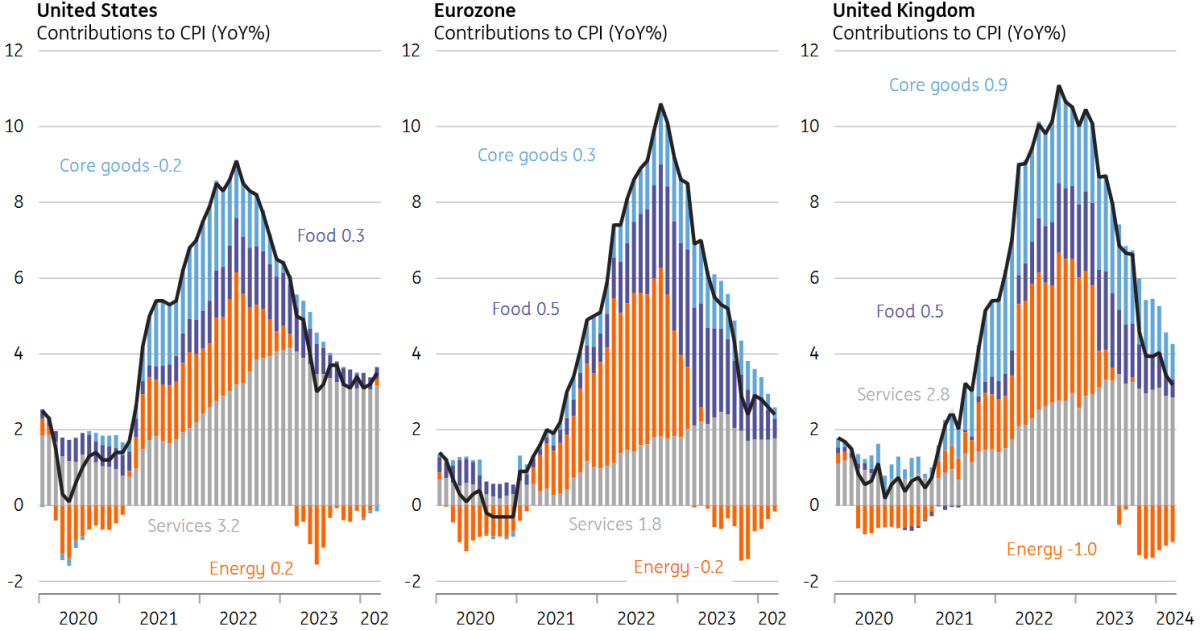

Up to now, investors had been expecting the Bank of England to largely mirror the Fed on rate cuts this year, despite growing divergence between Fed and European Central Bank expectations. UK services inflation (6%) is noticeably higher than the US (5.3%) or eurozone (4.0%) and investors have understandably found it hard to see the BoE being able to cut ahead of the Fed.

But that’s changing. Investors now expect two rate cuts in the UK this year, starting in August. This repricing could have further to run.

2024 rate cut expectations are creeping up in the UK relative to the US

Remember that we don’t hear from BoE officials nearly as often as we do from their colleagues at the European Central Bank or Federal Reserve, where there is near-daily commentary on the rates outlook. There’s an apparent reluctance to fine-tune market pricing unless it is materially diverging from what the BoE thinks is realistic. The aftermath of the 2022 mini-budget crisis was a rare example of the Bank telling markets they were wrong on rate hike expectations.

The current chorus of optimism on the inflation outlook among key BoE figures, therefore, feels both intentional and significant. And we could see the Bank’s signalling on rate cuts becoming bolder still in the coming days, given the realignment of market pricing has only just begun. The next meeting in a little over two weeks will be key.

There is further disinflation in the pipeline in the UK

After all, we think the Bank is right to draw a distinction between the inflation outlook in the US and the UK. Where US inflation is now virtually entirely service-driven, there are more obvious near-term sources of disinflation in the UK.

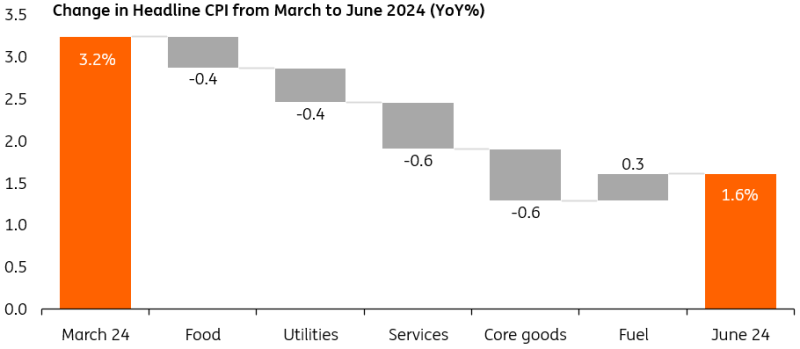

The well-telegraphed 12% fall in household energy bills in April will drag headline inflation lower, and that’ll likely be followed by a further decline in costs in July. Food inflation, currently at 4%, is also falling fast and will be close to zero by the summer, given what we’re seeing in producer price data. We expect further disinflation in core goods too.

How UK inflation compares

Even on services, the news should slowly get better. Admittedly, we think services inflation will stay sticky in the near term, and April’s data, due in May, will be heavily affected by annual price hikes. We think this data could come in some way above BoE forecasts.

We reckon that tilts the balance in favour of the first cut coming in August rather than June, though it’s a close call. At the very least, it should make the Bank reluctant to heavily commit to anything at its May meeting. But that doesn’t mean we can’t see further steps to prepare markets for the first move.

How BoE communications are set to change

Could the Bank go as far as saying that a rate cut is likely “over coming months”? That was a phrase that preceded the first rate hike back in 2017, at a time when the committee felt markets were ignoring its previous, more subtle hints on the timing of the first move. That signal was widely interpreted at the time as meaning within three months.

That might be a stretch, but some tinkering with the forward guidance in May is possible. If the Bank waters down the language on rates needing to stay restrictive for “an extended period”, that would be tantamount to signalling policy easing is imminent. It would probably be a catalyst for us to switch our base case to a June rate cut. And if that happens, it would have the potential to be a big market mover.

How UK inflation is set to fall further by June

The UK can diverge from the Fed

Whatever happens, it looks like the Bank of England may well cut rates ahead of the Fed, where we expect the first move in September. We think the totality of BoE cuts this year will be greater too.

That would mark a bit of a departure from the recent rate hike cycle, where the BoE, along with several other European central banks, appeared to chase US rates higher out of heightened sensitivity to currency weakness.

The link between Fed and BoE policy is often overstated

However, that period was unusual, and we think the link between Fed and BoE policy is often overstated. There are plenty of examples where the BoE has diverged from the Fed in a meaningful way, and the US rate hiking cycle in 2016-18 is the most recent.

Indeed, those concerns about the impact of a weaker currency have probably taken a back seat. Not only is inflation much lower and there’s greater confidence about the disfination in the pipeline, sterling has been one of the more resilient G10 currencies in the face of renewed dollar strength. In a sense, that offers a bit of a cushion against any fresh weakness and feedthrough to inflation.

In short, we don’t think the BoE would have many qualms about cutting rates before the Federal Reserve, nor moving a little more quickly in subsequent meetings.

Outlook for UK market rates

Sterling rate markets initially followed the move up in US yields as a 'no-landing' narrative of resilient growth and sticky inflation became more prevalent. But UK yields have started to retrace that move and we think this should continue as the BoE independence from the Fed grows. With the European Central Bank poised to cut in June and the Fed set to stay on hold until September, market pricing for BoE cuts should converge towards that of the ECB. When comparing one-year swap rates, UK rates have at least another 20bp to fall in order to align with the eurozone.

On top of that, we think that sticky US inflation tilts the balance towards higher US rates, especially on the short end of the curve, which is dictated by the timing of the first cut. This week’s PCE inflation number is unlikely to appease markets and thus a further drift up in 1-year US swaps is a likely scenario.

With the Fed pivoting towards a debate on whether a rate cut is realistic this year at all, another rate cut priced out by markets in the coming year is not unrealistic. Together with BoE convergence towards ECB market pricing, this could bring the one-year USD-GBP spread to the range of 60-70bp.

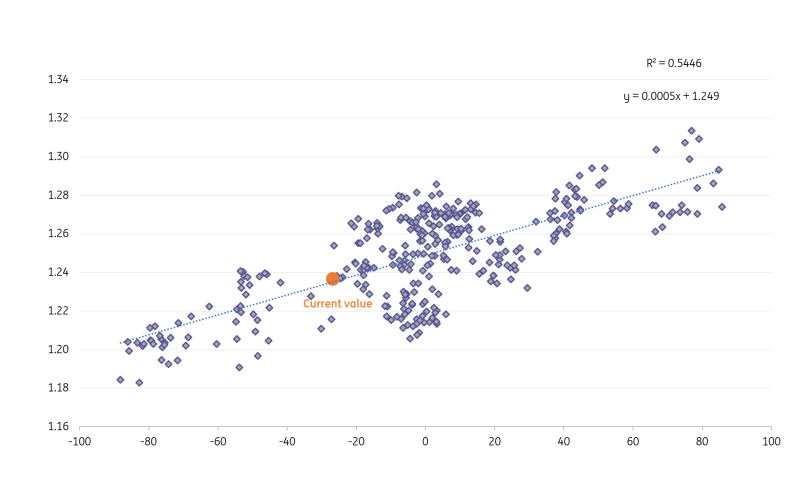

GBP/USD versus the one-year GBP:USD swap differential since January 2023

Outlook for sterling

It sounds like Bank of England communication may be the biggest catalyst for repricing the BoE easing cycle in the near term. If indeed that is the case, we would expect greater differentiation between the BoE and Fed cycles to particularly weigh on GBP/USD. Here, there has been a decent relationship between one-year GBP:USD swap differentials and GBP/USD, as outlined above.

At an extreme, say 50bp, swing in the GBP:USD one-year swap differential in favour of looser BoE policy, the relationship since the start of 2023 suggests GBP/USD should be trading closer to 1.21. In short, it looks like some further sterling under-performance is certainly the near-term risk

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article