Bank of England poised for July rate hike on energy spike

- 11 June

- United Kingdom

A material spike in oil and, crucially, natural gas prices this July would make it harder for the Bank of England to avoid hiking rates. We're pencilling in a one-and-done rate rise this summer

A June rate hike now looks unlikely, but...

If we’re right about energy prices, it’s going to become increasingly difficult for the Bank of England to avoid a rate hike this summer.

That said, the case for moving in June has weakened. Natural gas prices have stayed remarkably benign – and that matters, because Britain remains one of the most gas-reliant economies in Europe. Household energy bills are set to rise by 13% in July, but on current pricing they’re likely to fall by around 7% in October.

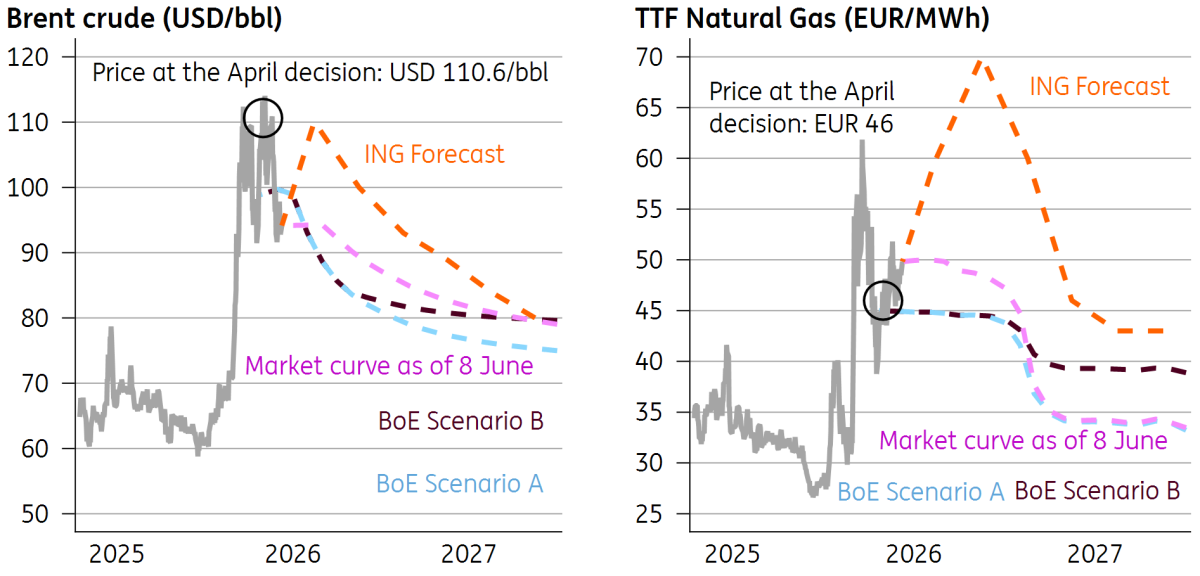

Back in April, the BoE sketched out three scenarios. Right now, markets look closest to the middle one – 'scenario B' – which most officials felt didn’t necessarily require further tightening. The Bank’s models reckoned this scenario would be roughly consistent with 55bp of tightening versus a pre-war baseline. And given it had expected to cut rates twice this year, that means simply holding Bank Rate at 3.75% would probably do the trick.

But by July, the backdrop could look very different. Our Commodities team sees oil pushing up to $120/bbl, with natural gas climbing towards €70/MWh by the fourth quarter (about 175p/therm on the UK benchmark).

That would take us well away from the Bank’s 'scenario B' and halfway towards the more adverse 'scenario C'. In our new base case, we see headline CPI peaking at 4.3% early next year, as higher gas prices feed through into household energy bills and keep food inflation elevated into the winter.

Our forecasts are above the Bank of England's 'scenario B' from April

A July hike is likely if energy prices spike

If disruption in the Strait of Hormuz hasn’t eased by the July meeting, the Bank will also have to lean more heavily against the tail risks, however unlikely, that the disruptions extend into the autumn. Policymakers are acutely aware that the longer this lasts, the greater the risk of second-round effects.

Against that backdrop, we think the BoE will tilt towards a July hike. It’s not a done deal – and a faster resolution that avoids the renewed spike in oil and gas prices we’re now forecasting would more easily justify a prolonged pause.

Even then, any move is likely to be one-and-done. Data over the past month has been a stark reminder that the UK economy is less susceptible to another prolonged bout of inflationary pressure. The jobs market is weak. Consumer-facing employment has fallen 2-3% over the past year, and the pace of the decline shows little sign of slowing.

Wage growth is dropping sharply and should soon fall below 3% in the private sector. Much of that reflects last year’s tax and minimum wage hikes – a reminder that UK corporates have far less pricing power than they did during the last energy shock.

In short, the case for sustained tightening remains far from clear-cut. And we still think we’re likely to see a return to rate cuts in 2027, something markets aren’t currently pricing.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Already playing into extra time

- This bundle contains 14 Articles