Bank of Canada: We expect a cut this week

- 2 March 2020

We look for a 25bp cut by the BoC this week as coronavirus worries increasingly weigh on the economic outlook. This should translate into more Canadian dollar weakness in the short-term, mostly versus low-yielders

We have been pencilling in a 25bp BoC rate cut in early 2020 for some time now, but recent data had led to some doubts given robust job and wage figures while inflation was broadly in line with target. However, it is increasingly apparent that the coronavirus outbreak will be a major drag on both the global and Canadian economies in 2020. With G7 Finance ministers and Central Banks scheduled to hold a conference call to discuss their responses tomorrow, we confirm our view that the BoC will cut rates 25bp this week with a further 50bp of easing likely in subsequent months

GDP growth had already slowed to just 0.3% annualised in 4Q19 and it seems probable that 1Q20 Canadian activity will be depressed by supply chain disruption because of factory closures in China and other parts of Asia. Exports will also be hurt by weaker demand from the region while protests trying to block the construction of the Coastal GasLink pipeline have had a disruptive effect on rail, road and sea transportation.

The plunge in equities and bond yields means the economy is also facing a financial shock that could lead to economically disruptive strains in lending markets. Then there is the threat of an aggregate demand shock as a sense of fear leads to consumers and businesses changing their behaviour. This would most likely be felt in the services sector with travel, leisure and personal services sectors looking vulnerable to a sharp drop in demand. Add in the plunge in commodity prices, most notably oil, and business investment will likely weaken. As such an outright contraction in economic activity is a distinct possibility for 2Q20.

Swift and decisive

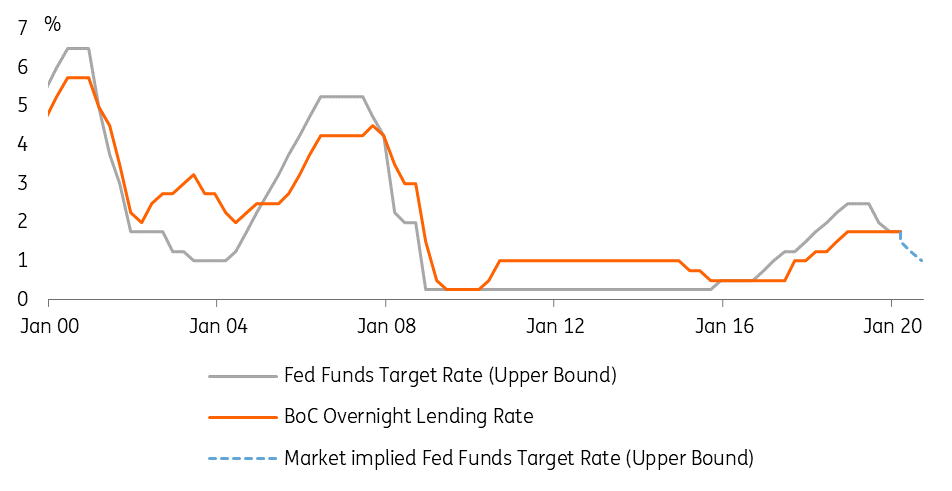

The Bank of Canada has a reputation of being prepared to move early and deliver occasional surprise moves and we expect it to cut rates 25bp on Wednesday. In any case, the BoC has more room than most central banks to provide support to the economy and financial markets (the Overnight Lending Rate is at 1.75%). Given what has happened elsewhere, the domestic newsflow surrounding Covid-19 is likely to get worse before it gets better and we therefore expect the BoC to deliver a further 50bp of rate cuts in coming months.

CAD: More short-term woes

Looking at the market implications, it must be noted that markets have already priced in a significant amount of easing by the BoC for the next months. Despite the easing expectations being less aggressive than those for the Fed, two BoC cuts are already factored into the Canadian OIS curve for the next two quarters.

Despite hardly coming as a shock, markets may well not be entirely positioned for a cut at this week's meeting, so we expect a short-term negative impact on the loonie if our call proves right. The OPEC+ meeting will be another key challenge for CAD this week given markets high expectations in terms of production cuts. Jobs data will also be watched on Friday, with the bar set quite high after the very strong January numbers.

All this suggests that the headaches for the loonie in the short-term are far from over, although USD/CAD may fail to rally significantly more thanks to an underperforming USD as Fed easing expectations rise. In turn, most of the additional downside for CAD should be mostly channelled through low yielders, in particular JPY.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Central banks to the rescue

- This bundle contains 7 Articles