Bank of Canada preview: Too early for a radical pivot

Core inflation came in hotter than expected in December which rules out the Bank of Canada shifting meaningfully in a dovish direction at the January meeting. However, higher interest rates are biting and we continue to look for rate cuts from the second quarter onwards. US-dependent BoC rate expectations and the Canadian dollar may not move much for now

Hot inflation warrants caution before dovish turn

The Bank of Canada is widely expected to leave the target for the overnight rate at 5% when it meets next week. Policymakers continue to talk of their willingness to “raise the policy rate further if needed”, and inflation does indeed continue to run hotter than the BoC would like, but we see little prospect of any additional policy tightening from here. Instead, the next move is expected to be an interest rate cut, most probably at the April meeting.

The latest BoC Business Outlook Survey reported softening demand and “less favourable business conditions” in the fourth quarter with high interest rates having “negatively impacted a majority of firms”, leading to “most firms” not planning to “add new staff”. Job growth does appear to be cooling and the Canadian economy contracted in the third quarter and is expected to post sub 1% growth for the fourth quarter. Also remember that Canadian mortgage rates will continue to ratchet higher for an increasing number of borrowers as their mortgage rates reset after their fixed period ends. This will intensify the financial pressure on households, dampening both consumer spending and inflationary pressures. Unemployment is also expected to rise given the slowdown in job creation and high immigration and population growth rates.

Given this backdrop, we expect Canadian headline inflation to slow to 2.7% in the first quarter and get down to 2% in the second versus the consensus forecast of 2.6%. As such, we see scope for the BoC to cut rates by 25bp at every meeting from April onwards – 150bp of interest rate cuts versus the consensus prediction and market pricing of 100bp of policy easing.

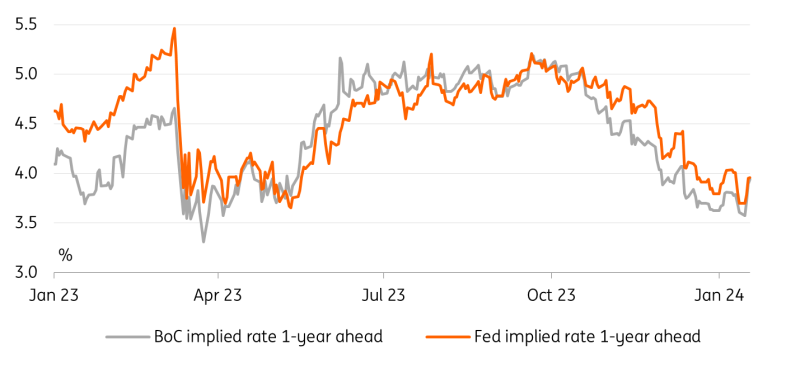

Rate expectations in US and Canada

Fighting market doves is still hard

Markets currently price in 95/100bp of easing by the Bank of Canada this year. As shown in the chart above, the pricing for rate cuts in the US and Canada has followed a very similar path. The implied timing for the first rate cut is also comparable: May for the Fed (March is 50% priced in), June for the BoC (April is 45% priced in). That is despite the communication by the Federal Reserve which has already pivoted (via Dot Plots) to the easing discussion while the BoC officially still retains a tightening bias.

In practice, even if the BoC chooses – as we suspect – to delay a radical dovish pivot and stay a bit more hawkish than the Fed, pricing for the BoC will not diverge too much from that of the Fed. So, the room for a rebound in CAD short-term rates appears more tied to USD rates than BoC communication.

FX: USD/CAD to stabilise

In FX, the story isn’t much different. The Canadian dollar has been a de-facto proxy for US-related sentiment, acting less and less as a traditional commodity currency – that would normally be hit by strong US data – thus outperforming the rest of high-beta G10 FX since the start of the year. The rebound in USD/CAD to 1.35 is in line with a restrengthening of the USD primarily due to risk sentiment, positioning and seasonal factors, rather than a divergence in Fed-BoC policy patterns. In fact, the USD-CAD two-year swap rate gap has widened further in favour of CAD so far in January, from 20bp to 32bp.

We expect the impact on CAD from this BoC policy meeting to be modestly positive as expectations of a radical dovish shift are scaled back. However, Governor Tiff Macklem already introduced the idea of rate cuts in a speech this month and will need to acknowledge the downward path for the policy rate to a certain extent. While waiting for the Fed meeting a week later and the crucial US CPI numbers for January, US-dependent rate expectations in Canada may not move much. USD/CAD may trace back to 1.34, but we don’t see much further downside for the pair this quarter as USD shows the last bits of strength.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more