Bank of Canada preview: Time is ripe for a cut

We think markets are underestimating (16bp) the chances of a rate cut next Wednesday. Consensus is split, but with inflation within the BoC’s comfort band and unemployment rising, we see policymakers narrowly favouring a 25bp cut. However, the BoC may be cautious on signalling further easing as the rate spread with the Fed may widen excessively

Why we expect a cut next week

Out of 26 banks surveyed by Bloomberg there are 16 going for a 25bp rate cut by the Bank of Canada on 5 June, versus 10 favouring the BoC keeping the overnight lending rate at 5%. Markets are seeing a similar balance of probabilities with around a two-in-three chance of a 25bp rate cut currently priced. The data is seemingly arguing in favour of a move and we think, given the BoC’s history of being prepared to make bold calls, that it will narrowly opt for a 25bp cut. The caveat is that BoC officials haven’t been especially vocal on the prospect of a cut and they may instead choose to use this meeting to tee up a move in July. A move at that meeting is currently fully priced by financial markets.

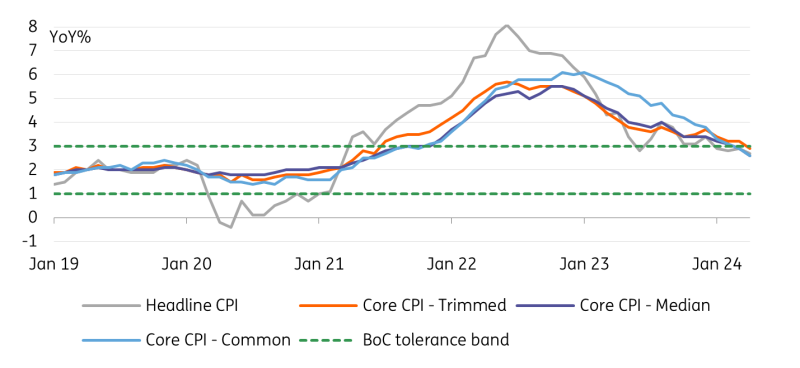

The key to the June rate cut view is that consumer price inflation has slowed to 2.7% with core inflation also now below 3% year-on-year, meaning that both inflation metrics are within the BoC’s comfort band of 1% to 3%. Unemployment has risen to 6.1% from a bottom of 4.9% in mid-2022 while wage growth is rangebound at just under 5% YoY. First-quarter GDP likely grew a little above 2% annualised after a weak second half of 2023, but this was primarily due to a 0.5% month-on-month jump in activity in January as February recorded a more muted 0.2% growth rate and March expected to post a flat output.

Moreover, the effects of tight monetary policy are becoming increasingly apparent with the household debt service ratio at a record high at 15% versus 9.8% in the US. The risk of rising loan delinquencies is very real with unemployment on the rise, which would heighten the chances of a potential recession. Note that in this regard three consecutive monthly falls in retail sales is not a good look at a time when immigration growth has been so strong.

Canadian inflation back inside the target band

BoC should not sound too dovish on future policy

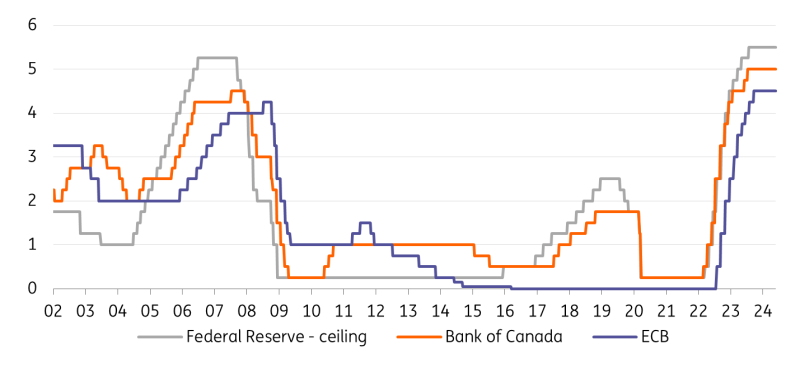

Given this backdrop we believe the BoC will choose to cut interest rates by 25bp, but it will likely be wary about cutting too far too quickly given it could create the impression of clear divergence from the US. After all, if we are right and the BoC does cut by 25bp on Wednesday the spread between the fed funds ceiling rate and the BoC policy rate would widen out to 75bp.

This would be the widest since July 2019 and if the BoC were to cut again in July before the Fed acts (we expect it to cut rates in September) we would see the widest spread since 2009. This could potentially have implications for the Canadian dollar so we expect the BoC to come out with relatively cautious messaging on the prospect of more rate cuts. Nonetheless, with the Fed expected to cut from September onwards we do see room for the BoC to lower the policy rate to 3.5% in the first half of 2025.

BoC rates versus Fed and ECB

Canadian dollar to weaken in the crosses

Markets are, in our view, underpricing both the chances of a rate cut in June and those of further easing by year-end. Despite the faster-than-expected decline in Canadian headline and core inflation, BoC market pricing has remained highly influenced by Fed expectations: with markets having turned less dovish on the Fed, the implied probability of a June BoC cut has also not exceeded 70/75% throughout April and May – now at around 65% or 16bp. A total of 52bp of BoC cuts are priced in by year-end, around 20bp more than for the Fed.

Our view on the BoC has been more dovish than markets for quite some time, and has fed into our view that the Canadian dollar will prove to be a laggard in the coming months. Along with the wide room for a dovish repricing (we expect three more BoC cuts in 2024), CAD also tends to underperform other commodity currencies when US data surprise on the downside. If we are indeed going to see softer US data, CAD may end up performing closer to USD than to the rest of G10.

In the commodity FX space, we expect the loonie to trade on the soft side mostly against NZD, AUD and NOK, as markets should prefer to reward those currencies that can count on hawkish central banks. When it comes to USD/CAD, the direction of travel should still be primarily set by the USD leg, thus by US data and the Fed. We expect a first Fed cut in September and suspect the USD may have already traded at its pre-US-election peaks. With that in mind, a move to 1.35 in USD/CAD over the summer remains our base case, despite BoC easing.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article