Bank of Canada outpacing the Fed as inflation fears mount

- 13 April 2022

- Canada

The Bank of Canada has hiked its policy rate by 50bp and has announced the start of quantitative tightening. A strong outlook for growth is heightening concerns that inflation is becoming embedded with more large rate hikes on their way. This should be a supportive environment for the Canadian dollar

| 50bp |

Bank of Canada's policy rate change |

Aggressive Bank of Canada puts pressure on the Fed to follow suit

The Bank of Canada (BoC) has raised its policy rate by 50bp to 1%, in line with expectations, and will cease buying government bonds on 25 April. This marks the start of a fairly aggressive quantitative tightening process since there is no gradual managed roll-off as with the Federal Reserve in the United States. Assets will just be allowed to mature, and given around 40% will do so in the next two years this will result in a much swifter run down of the Bank of Canada’s balance sheet than the $95bn or roughly 1% of its balance sheet the Federal Reserve is proposing each month.

With the Reserve Bank of New Zealand also having hiked rates 50bp in the past 24 hours, expectations will undoubtedly rise that the Fed has to follow suit. It may also spark some of the more hawkish members of the Federal Reserve to propose larger monthly roll-offs, or even asset sales.

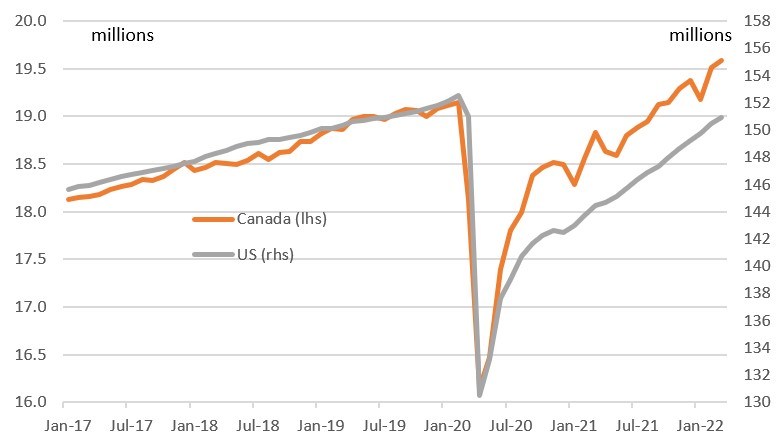

Canada's jobs market has outperformed the US's

Inflation risks are mounting, growth looks resilient

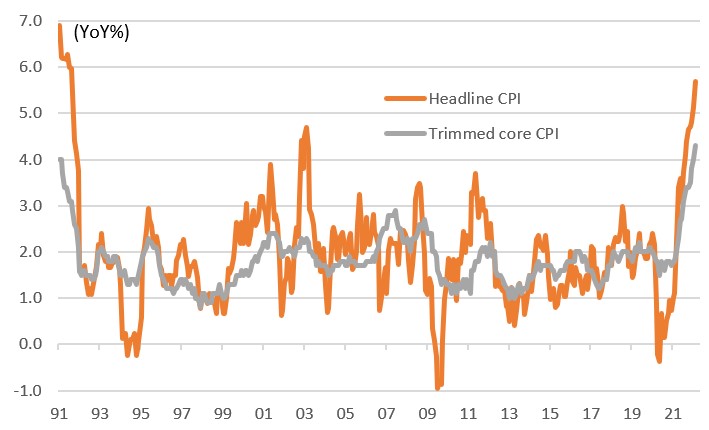

Within the statement, the BoC cites the war in Ukraine, Covid-19, and ongoing supply chain issues as reasons for economic uncertainty, but they also contributed to “a substantial upward revision” to the bank’s outlook for inflation. CPI is now expected to average 6% through the first half of the year and not get consistently back to the 2% target until 2024.

Furthermore, the BoC remains upbeat on growth with GDP forecasts of 4.25% in 2022, 3.25% in 2023, and 2.25% in 2024 with excess demand, a tight labour market, and rising wage growth underpinning activity. Canada’s important commodity production sectors also provide reasons for optimism on activity with high prices boosting profitability, investment, and jobs while rising immigration will add to the economy’s productivity potential.

Canada inflation is at 30-year highs

Another 50bp in June looks likely

Given this situation, the statement talks of the risks of inflation becoming embedded and inflation expectations unanchored with an acknowledgement that "interest rates will need to rise further". There is little to suggest any meaningful changes in the global backdrop imminently and with such a strong domestic story – set to be underscored by another sharp rise in CPI next week – we look for another 50bp hike on 1 June with the policy rate set to hit 2.75% before year-end.

Canadian dollar should remain in demand

As a net commodity exporter, Canada remains less exposed to the stagflationary forces at work in regions like Europe. The Bank of Canada actually highlighted that in today’s policy statement. This should serve as a reminder that the BoC has more cause than many to undertake an aggressive tightening cycle.

Today’s bullish BoC statement and, as James notes its relatively aggressive balance sheet run-off, should continue to position the Canadian dollar as an out-performer – or one of the currencies best positioned to withstand what should prove a strong, Fed-powered US dollar this summer.

Indeed, today’s rate meeting has seen short-dated Canadian yields hold onto more of their recent gains than US yields, for example. We suspect any USD/CAD move over 1.27 should prove short-lived and that USD/CAD can even drift to the 1.20/23 area later this year. And given the more severe challenges faced in Europe, EUR/CAD can work its way to the 1.32 area.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more