Bank Indonesia cuts rates for the third time

- 19 September 2019

- Indonesia

Today's rate cut reinforces growth overtaking currency stability as the main driver for Indonesia's central bank policy. And if that is the case, the easing cycle still has room given the aggressive tightening in 2018

| 5.25% |

Bank Indonesia policy rateAfter 25 basis point cut today |

| As expected | |

Rate cut - again!

Indonesia's central bank cut the policy rate by 25 basis points - the third rate cut taking the policy rate to 5.25%.

The decision was consistent with the broad consensus. We were in the minority, only seven out of 28 analysts in the Bloomberg survey forecasted no rate cut. A policy pause after two consecutive rate cuts looked more plausible in a turbulent market environment threatening the rupiah's stability.

Despite elevated market volatility

September did bring some relief for markets, thanks to the slight thawing of US-China trade relations, making the case for opportunistic BI easing.

But the relief was short-lived and, in unanticipated support to our stable policy forecast came the Saudi Aramco facilities crisis causing the worst oil price spike in decades threatening IDR stability. Indeed, the IDR has been the worst-performing Asian currency this week, warranting stable BI policy.

Recall that currency weakness was behind all that aggressive policy tightening in 2018 with 175bp of rate hikes.

What did policymakers say?

The central bank Governor Perry Warjiyo described today’s move as “a pre-emptive step to support the momentum of domestic economic growth amid slowing global economic conditions”. He also said, “The policy is consistent with an estimate for inflation to remain low at below the mid-point of our target range and the yield of domestic financial assets remaining attractive”.

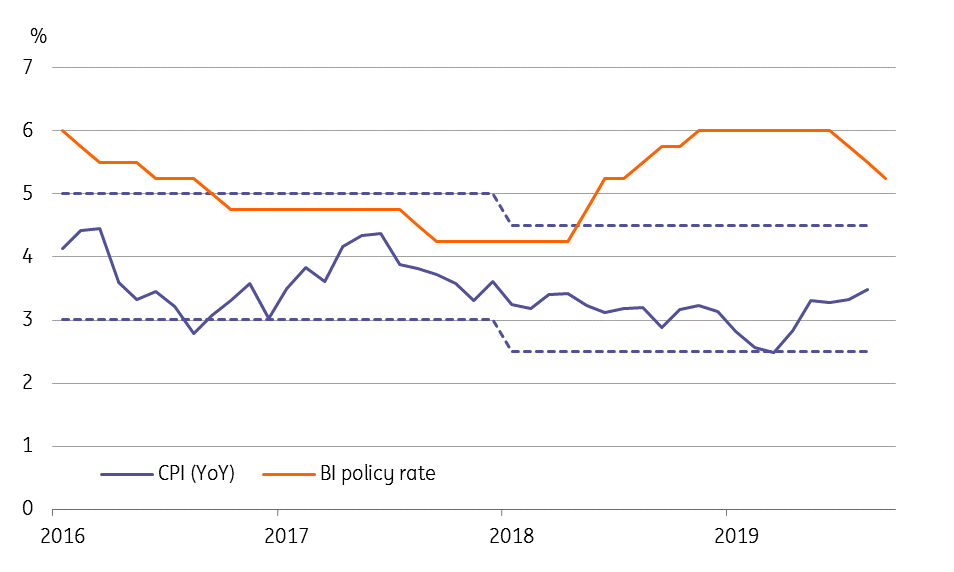

Indonesia's central bank targets inflation in a 2.5%-4.5% range and it’s been under the 3.5% mid-point of this target since January 2018. Growth has been stuck around 5% since 2014 and BI sees it at 5.1% in 2019, or near the low end of its 5.0%-5.4% forecast range.

Well-anchored inflation allows for more easing

Not done just yet

Clearly, growth has overtaken currency stability as the main policy driver while inflation continues to be under control, barring an oil price shock.

If we are correct, then there is a greater likelihood of BI utilising the policy room created by the tightening in 2018 to substantiate President Jokowi’s push for faster, investment-led growth in his second term in office.

Although we expect the central bank to continue to tread a cautious policy path, more so after renewed inflation threats from an oil price shock, we're not ruling out at least one more 25bp rate cut before the end of the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more