Australian supply risks hang over the gas market

The last month has been a volatile period for gas markets, particularly in Europe. A combination of extended maintenance in Norway and uncertainty over potential strike action at Australian LNG facilities has left the market nervous. However, European storage is comfortable and we'd need to see prolonged strike action in order to be overly bullish

Europe looks comfortable despite Australian supply risk

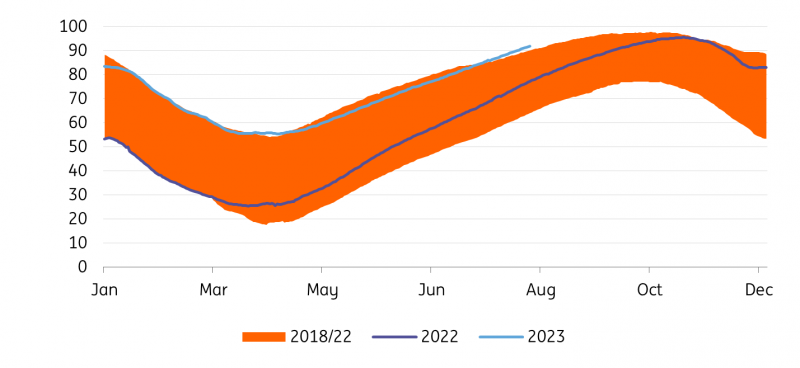

The European gas market is in a strong position. EU storage is now 92% full, above the 78% seen at this stage last year and also a record high for this time of year. Crossing the 90% threshold also means that Europe has hit its goal of having storage 90% full more than two months before the European Commission’s target date. Assuming no significant supply shocks, the EU will go into the next heating season with storage 100% full. This suggests that prices ahead of winter should weaken to divert LNG elsewhere, while time spreads are also likely to move into deeper contango, reflecting the well-supplied prompt market.

However, the big upside risk for the market is if potential LNG strike action in Australia runs into the 2023-24 winter. While it appears as though strike action at Woodside’s 16.7mtpa North West Shelf has been averted, there is still uncertainty over what will happen at Chevron’s Gorgon and Wheatstone facilities, which have a combined capacity of 24.5mtpa and make up around 6% of global LNG supply.

Australia is not typically a supplier of LNG to the EU – however, the removal of this supply would see Asian buyers having to look elsewhere. As a result, we'd likely see more aggressive competition for supply in a tighter LNG market.

A short strike will be manageable. However, a strike that runs through a large part of the northern hemisphere winter would be more of a concern. European gas demand basically doubles over the winter months, and so storage will naturally draw. In a market where a large share of global LNG supply is absent, storage would decline at a quicker pace – particularly given Europe’s higher dependence on LNG. This would likely drive prices higher than initially thought.

For now, we have kept our forecasts for TTF unchanged. We still expect TTF to average EUR32/MWh in the third quarter of this year and EUR50/MWh over the fourth quarter as the market starts to draw down storage over winter. Europe will still be vulnerable over 2024 given the lack of new LNG capacity coming onto the market, which suggests that prices are likely to remain well supported through next year. Much will also depend on weather through the 2023/24 winter.

European gas storage hits Commission target well in advance (% full)

A summer of volatile gas flows

Gas flows into Europe have been fairly volatile over much of the summer. This volatility has been largely driven by Norway, where summer maintenance led to reduced flows. While much of this maintenance was planned, some of it did go on for longer than expected. As a result, from early April through until mid-July, Norwegian flows averaged a little over 260 mcm/day, down from 312mcm/day over the same period last year. More recently, further maintenance has seen flows fall from close to 340mcm/day to around 255mcm/day. Despite the reduced flows, European storage has still filled up at a good pace.

Stronger LNG imports helped the European market in April and June, evident by LNG send-outs hitting record levels in late April. However, since June, LNG inflows have started to trend lower. Given the comfortable storage levels, Europe does not need to pull in LNG at the pace it has for much of the injection season. This again is reflected in the JKM-TTF spread, which currently sees the Asian LNG market trading at a premium to Europe. Given the expectation that European storage will be full ahead of the heating season, TTF will need to continue to trade at a discount to JKM for at least the next couple of months.

European gas demand still struggles

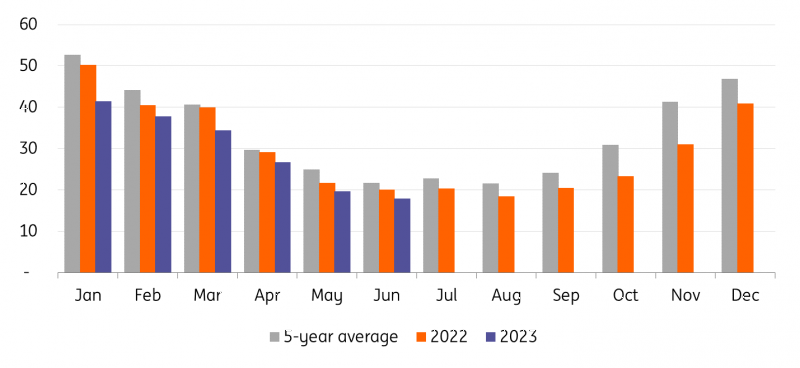

A factor that has helped storage reach the levels it has is the fact that demand is still not showing any strong signs of recovery despite the broader weakness we have seen in European natural gas prices this year. Our balance sheet towards the end of the last heating season suggested that EU demand only needs to be around 10% below the 5-year average in order for storage to be comfortable going into the 2023-24 winter. However, demand has clearly remained much weaker than this. The latest numbers from the European Commission show that consumption in June was around 17% below the 2017-21 average and 11% below last year’s levels. Germany, the largest gas consumer in Europe, saw total demand in July down more than 22% from the 2018-21 average.

There is a combination of reasons that continue to weigh on demand, including energy-intensive industries still running well below capacity, energy efficiency gains, fuel switching and the permanent shutting of production capacity. For example, chemicals producer BASF announced permanent capacity closures in Europe earlier this year due to high energy costs.

EU gas demand remains under pressure (bcm)

China imports slowly pick up

China’s LNG imports got off to a slow start this year. However, as we have progressed through the year, import volumes have picked up and cumulative imports over the first seven months are up 9.3% year-on-year to a total of 39.24mt (53bcm). This is still 13.3% below volumes imported over the same period in 2021. These volumes appear to largely reflect term contracts while China remains largely absent from the spot market. Given the current domestic macro environment, it is difficult to see China being extremely active in the spot market for the remainder of the year. Industry is a key consumer of gas in China and has clearly been under pressure this year.

US insulated from Australian supply risk

The US market has been more immune to the volatility we are seeing in Europe as a result of the Australian strike risk. This shouldn’t be too surprising, given that US export volumes will already be at or very near export capacity. Therefore, any supply disruptions in the global LNG market cannot be offset by additional supply from the US.

US natural gas storage has been filling up at a good pace for much of the injection season. Working storage stands at 3.08Tcf, which is 20% above levels seen at the same stage last year and 9.5% above the 5-year average. Since mid-July, the pace of injections has been somewhat lower than we have seen in recent years – although the US should still go into the start of the heating season with comfortable storage levels.

Despite good storage, we still hold a somewhat constructive view on the US gas market. The low price environment has seen the US gas rig count fall by 25% year-to-date to 117 rigs according to Baker Hughes, the lowest levels since February last year. Given a large share of US gas production is from associated production, it is also worth looking at the oil rig count, which has fallen by 16% so far this year to 520 rigs. As a result of this slowdown in drilling activity, US natural gas output is expected to grow at a much more modest pace. For the remainder of 2023, US gas output is expected to be largely flat, whilst for 2024, output is expected to grow by a little more than 1bcf/d from 2023 levels. We will need to keep an eye on how drilling activity evolves in the months ahead. A continued slowdown would likely eat further into expected supply growth for next year.

This modest growth – along with additional LNG capacity set to start up over the latter part of 2024 – suggests that we could see the US market start to tighten up over the course of next year. As a result, we expect Henry Hub to average US$3.30/MMBtu in 2024, up from around US$2.50/MMBtu at the moment.

ING natural gas forecasts

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more