Asia week ahead: Spotlight stays on China

- 7 February 2020

All that matters for markets is news about the epidemic and how the outbreak will impact economies around the region. Unfortunately, this week's data won't do much to help

Scant economic data from China

As the number of infections and fatalities from the coronavirus continues to rise, the economic data from China remains under scrutiny for the impact of the disease. However, it’s a bit too early for data to capture the impact of the disease, which is still evolving. There isn't much on the calendar this week either, aside from inflation and monetary indicators for January.

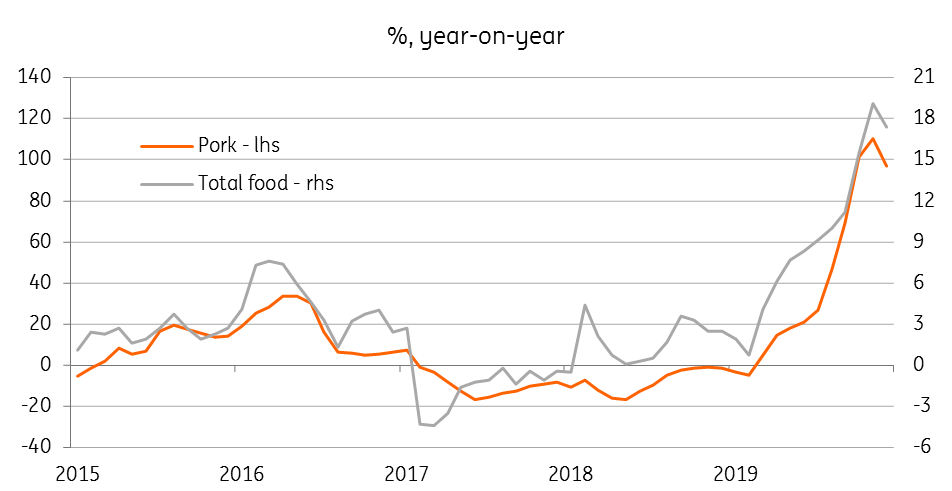

Higher food prices typically boost consumer price inflation in the New Year month. And one of the main drivers within the food category is pork prices. As an added whammy this year, an African swine fever has swelled pork prices out of proportion. On the flip-side though, one could wonder whether the outbreak of the virus and its spread countrywide dampened new year festivities and the food price increase was rather muted.

All that said, in line with consensus we are looking for CPI inflation advancing to 4.9% YoY from 4.5% in November. On the monetary side, behind the consensus of a bounce in new bank lending and aggregate financing lies the pre-holiday boost to the liquidity by the central bank (PBoC).

China Consumer Price Inflation

Not much going on elsewhere either

India’s January CPI data is likely to testify to the central bank's decision last week to leave policy on hold. We expect inflation to remain elevated, but no change from a 7.4% YoY rate in December. The fresh harvest entering the market should ease some pressure on food prices, but that’s likely to be offset by firmer fuel and utility prices.

In Malaysia, moderate manufacturing growth in the fourth quarter of 2019 suggests the same about GDP growth for the period, bringing the annual growth last year to 4.5%, down from 4.7% in 2018. With the coronavirus threatening tourism and overall demand, we would expect a couple more quarters of a slowdown ahead. If so, the Bank Negara Malaysia easing cycle will have further to run, while the government is also drafting a stimulus package.

Elsewhere, the Reserve Bank of New Zealand's policy meeting will almost be a non-event judging from the unanimous consensus forecast of no change to the 1% policy rate. Indonesia’s 4Q19 current account data may have some negative bias for the rupiah as the deficit is expected to widen.

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 10 February 2020

- This bundle contains 5 Articles