Asia week ahead: Regional manufacturing and inflation numbers in focus

- 29 July 2021

- Asia week ahead

Next week features a stacked economic calendar in Asia with regional manufacturing and inflation in focus and three central bank meetings

Regional PMIs

This week the focus shifts back to the manufacturing sector.

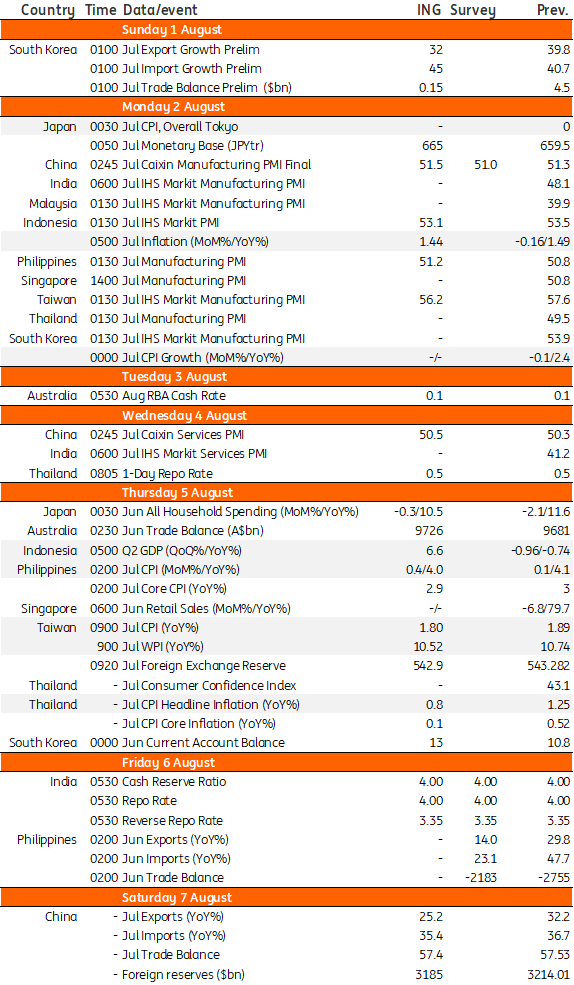

Market participants will be looking to see whether recent tighter mobility curbs have found their way through to Asia’s manufacturing sector. We expect a pickup in China’s Caixin PMI manufacturing to 51.5 (vs 51.0 consensus) as semiconductor chip production offsets slower output from the automobile sector. Meanwhile, manufacturing activity for the rest of region is expected to remain in expansion mode, though Indonesia and Taiwan are both expected to see a less pronounced pace of growth as recently imposed mobility restrictions start to weigh on overall economic activity.

Trade numbers still affected by base effects but new trends emerging

We will also get trade data from Korea (1 August) and the Philippines (6 August).

Both reports will show base-effect induced trade growth for the period, but looking past the “strong” growth rates, we notice rapidly rising imports in Korea and the Philippines as economic activity picks up relative to 2020. Surging imports in Korea could translate to a whittled down trade surplus of $145 mn - a stark drop from $4.5 bn in June. A similar trend for the Philippines could lead to a trade deficit of $2.2 bn. Accelerating imports, which could suggest a demand imbalance, may strengthen the case for a rate hike by the Bank of Korea in the coming months – following their guidance earlier this month.

Central bank meetings and inflation reports out during the week

Three central bank policy meetings are also scheduled next week, although all of them will likely leave policy settings as they are.

The Reserve Bank of Australia (RBA) will probably leave all aspects of their current stance unchanged despite a pickup in inflation in 2Q21. Market participants are still waiting to see whether the price spike in Australia pushes into wages. That said, the latest batch of Covid-19 induced lockdowns may encourage the RBA to take an even more dovish approach to previous guidance on asset purchases later this year. Both the Bank of Thailand and the Reserve Bank of India are also likely to be on hold.

India's central bank will most probably look past surging inflation (6.3% YoY in June) even though price pressures are likely to stick around and threaten their 6% upper inflation limit for the remainder of the year. Inflation in the country is forecasted to remain at elevated levels in the coming months, and we look to bring forward the timing of the first 25 basis points rate hike from 3Q22 to early 2022.

We'll also get several inflation reports from the region. Most of them should be subdued due to lacklustre domestic demand as parts of Asia have recently tightened or extended the scope of their movement restrictions. Indonesia’s July inflation should settle at 1.4%, below target yet again after the authorities locked down most of the country to deal with the delta Covid variant, while Philippine inflation should finally fall back within target at a relatively elevated 4% as supply conditions for food items ease.

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Good MornING Asia - 2 August 2021

- This bundle contains 5 Articles