Asia week ahead: Regional inflation readings and an MAS decision

The coming week features inflation readings from China and India, plus a meeting for the Monetary Authority of Singapore (MAS), where policy settings are likely to remain untouched

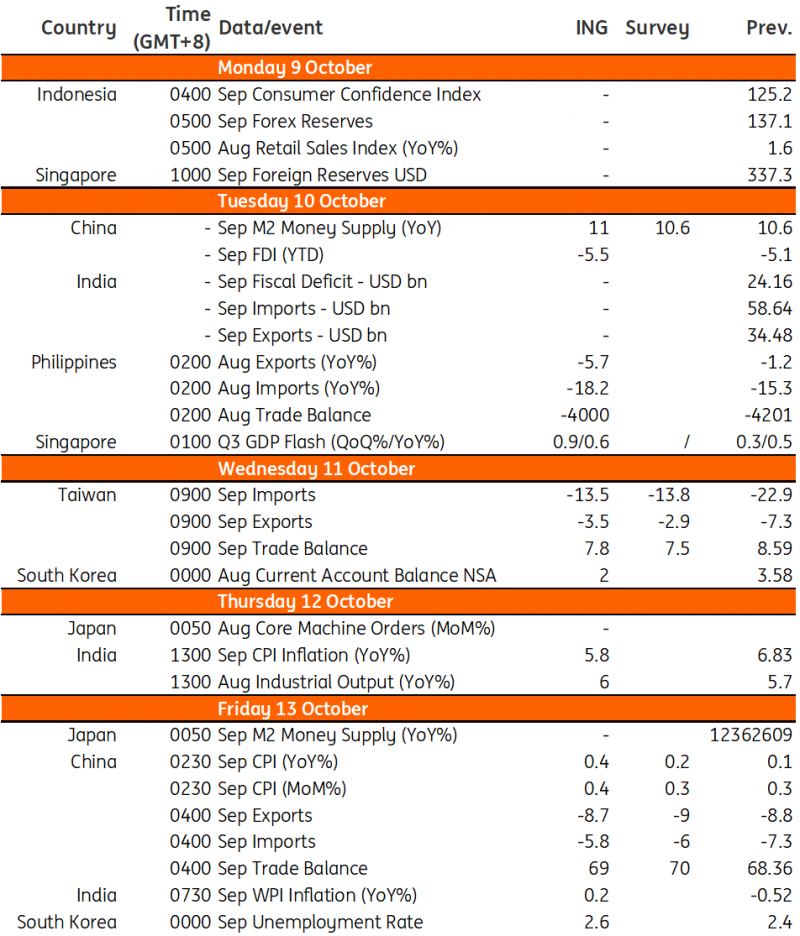

China inflation in the positive territory

China’s CPI inflation has returned to positive territory last month after it briefly slipped to -0.3% year-on-year in July. We expect the inflation to edge slightly to 0.4% YoY as the recent data suggests that the government’s efforts to boost the economy have had some impact.

On top of that, surging oil prices are likely to increase transport and energy costs for the period.

India inflation to settle within RBI’s target range

With supply concerns easing for key vegetables like tomatoes and onions, prices for these important commodities should moderate. As food items account for the bulk of the overall inflation basket, this should help bring India’s inflation down to 5.8% YoY, just within the 2-6% target range set by the Reserve Bank of India.

MAS expected to keep setting untouched

The Monetary Authority of Singapore (MAS) is likely to retain its current policy setting next week. The MAS looks to balance slower growth alongside still elevated inflation and will opt to keep settings untouched. Growth has struggled as of late, with exports dragged down by soft global demand. Meanwhile, inflation has been on the downtrend but could flare back up given a renewed rise in global energy prices.

Singapore GDP expected to remain subdued

Singapore’s third-quarter GDP figures will be reported next week. We expect growth to settle at 0.6% YoY, rising 0.8% from the previous quarter. Retail sales were the lone bright spot for Singapore, managing to post modest growth for the quarter.

The return of visitors to Singapore could be one factor helping support retail sales. On the other hand, contracting industrial production and falling non-oil domestic exports will be the main elements pulling down growth.

Key events in Asia next week

Download

Download article6 October 2023

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articlesThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more