Asia week ahead: Japanese inflation and South Korean sentiment data

- 20 March

- Asia week ahead United States

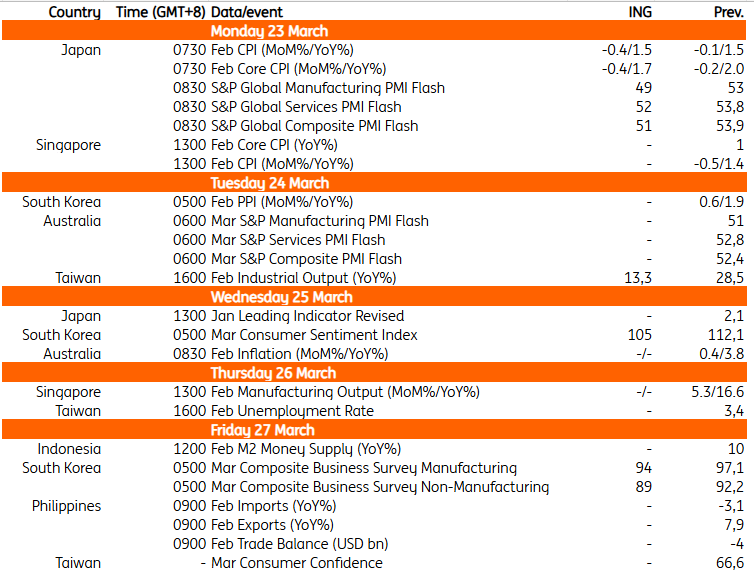

Japan releases February inflation data, while South Korea reports on March sentiment. Other key releases include Taiwan's industrial production data

Japan: CPI expected to cool further

Consumer price inflation is expected to slow further in February, primarily due to the government’s energy subsidy. It’s likely to show that the deceleration in inflation we saw before the Middle East crisis persisted. Yet core-core inflation is expected to stay well above 2.0%. Higher energy prices are likely to push up inflation again in the coming months, prompting the Bank of Japan to keep the door open to rate hikes. At the same time, the flash purchasing managers’ index is expected to drop sharply, with manufacturing falling more than services amid concerns about events in the Middle East. Overall, the timing of the next hike remains uncertain. In our view, an April move is unlikely, as the BoJ needs more time to assess the effects of rising energy prices on the economy.

South Korea: Sentiment data becoming less optimistic

Survey results on South Korean sentiment are likely to be less optimistic, as heightened geopolitical tensions reduce both confidence and economic activity. Higher gasoline prices and financial market instability are expected to significantly dent consumer sentiment. This will likely be reflected in the business survey as well.

China: A calm week ahead

It's a quiet week is ahead for China, with most of the key economic data already out for the month. We’ll get industrial profits data for the first two months of the year on Friday. Markets will watch for any improvement from the sluggish 0.6% year-on-year growth rate in 2025.

Taiwan: Moderating industrial production following Lunar New Year

Taiwan releases its February industrial production data on Tuesday. We expect activity to moderate toward 13.3% YoY thanks to the Lunar New Year effect. But production should be quite robust to start the year amid strong external demand.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more