Asia week ahead: Important inflation reports and key central bank decisions

Next week in Asia features several inflation reports from the region plus three central bank policy meetings

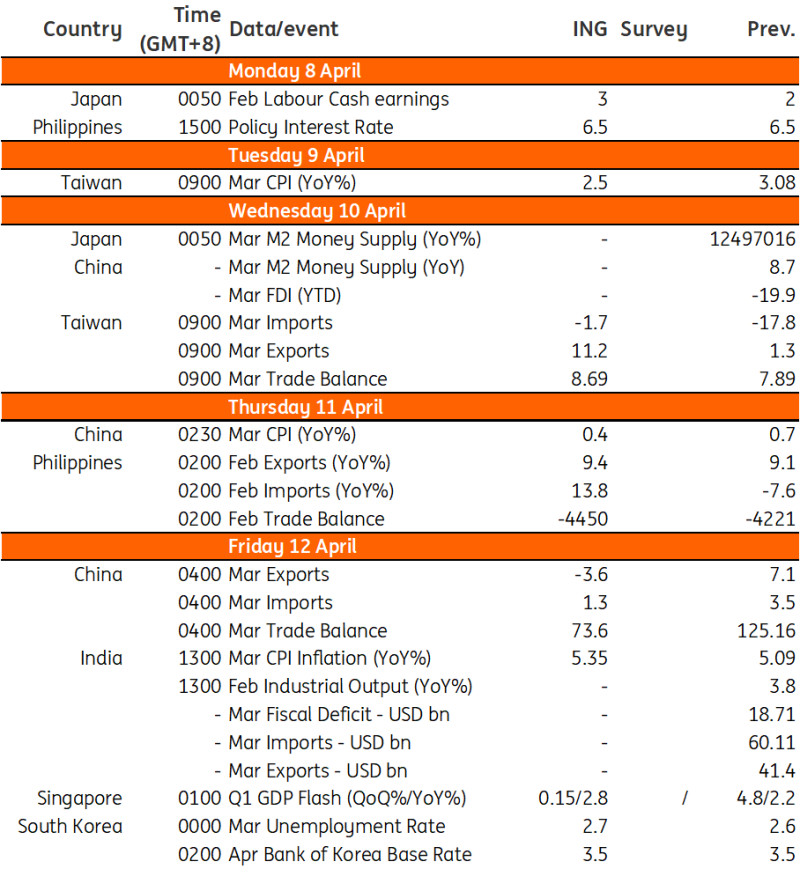

China inflation likely to moderate

China will publish its CPI inflation data next week, and a decline in food prices post-Chinese New Year will likely lead to inflation pulling back to around 0.4% year-on-year. Trade data will also be released on Friday. Positive momentum from the first few months, typical seasonality, and a recovery of export orders in the March PMI will likely lead to sequential solid growth – but YoY numbers may look poor due to a strong March 2024, potentially dropping to negative levels again before recovering in the next few months.

The credit data and FDI data may be published next week as well. Here, we expect a rebound of aggregate financing and RMB loans after the holiday effects caused weak February data. Given the strength of last year’s data in the first quarter, YoY growth numbers may be flat or negative. We are still looking to see if the 50bp RRR cut that took effect in early February will have any positive impact on lending.

Inflation to tick higher in India

Indian inflation for March will rise slightly from 5.1% YoY to 5.35% following a 0.5% month-on-month increase, as seasonal vegetable prices have pushed slightly higher after falling in recent months. This remains within the Reserve Bank of India's 2-6% target, but in the upper half of that range, and is one reason that the central bank isn't going to be in any hurry to start easing until the Federal Reserve begins to take US rates lower.

Taiwan inflation to dip

March CPI numbers will be released on Tuesday. We expect inflation to moderate in March to around 2.5% YoY, but this relief will be short-lived, as an electricity price hike in April will raise price pressures again. Trade data will be published on Wednesday, where we are looking for growth to pick up in both exports and imports.

BSP widely expected to extend pause

The Bangko Sentral ng Pilipinas (BSP) rescheduled its policy meeting to the coming week reportedly to wait for inflation data. Inflation has edged closer to the upper end of the BSP's inflation target, which should mean that the central bank will likely retain policy rates at restrictive levels. We expect the BSP to remain sidelined for at least the first half of the year, with any potential easing likely only following a potential Fed rate cut.

Singapore's first quarter GDP and MAS

Singapore reports first quarter GDP in the coming week, with economic output expected to gain a sizeable boost due to the influx of tourists related to a concert series. We expect first quarter GDP growth to hit 2.8% YoY, or roughly 0.15% up from the previous quarter. Meanwhile, the Monetary Authority of Singapore (MAS) will meet to decide on policy, and we expect it to retain all settings given the recent flare up in inflation.

BoK on hold again

The Bank of Korea meets on Friday. With the latest inflation and inflation expectations above 3% and IP and exports holding up fairly well, the BoK is expected to keep the policy rate at 3.5%. The central bank is likely to downplay higher-than-expected inflation, as this was mainly due to a temporary issue on the supply side.

South Korea will hold legislative elections on 10 April. Recent polls suggest that it will be a neck-and-neck race between the two major parties, as there is still a large number of undecided voters. Currently, the progressives (opposition party) hold a large number of seats in parliament, but in the last two elections – presidential and local – the conservatives won.

Japan’s labour cash earnings could bounce back

Labour cash earnings are a key data release for Japan next week and are expected to have grown by 3% in February. We expect a more meaningful rebound in cash earnings from April and May as the newly agreed wage negotiations kick in.

Key events in Asia next week

Download

Download article5 April 2024

Our view on next week’s key events This bundle contains {bundle_entries}{/bundle_entries} articles

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more